Sable Offshore (SOC): A $25 Billion Asset Trading for $600 Million

Investing in special situations

“When I first came to Columbia University, I was dirt poor. I did not choose to come here – I just ended up here because I had nowhere else to go, having just escaped from China after Tiananmen. I was in a new country where I didn’t understand the language, didn’t know anybody, and didn’t have a penny to my name. So I was desperate and afraid.”

Born in China, he was forced to flee after the Tiananmen Square crackdown, when the government crushed the 1989 pro-democracy movement with violence. He arrived in the United States with no money, no contacts, and no English. Yet in a completely foreign language, he managed to complete three of the hardest academic programs in America at the same time: an undergraduate degree, an MBA, and a law degree at Columbia.

At Columbia University, he once saw a flyer with the word “buffet” on it and thought it was an event with free food. When he showed up, there was no food — just some man named Buffett giving a lecture.

Warren Buffett.

Only then did he realize he had misread the word. That day, he decided that value investing would become the work of his life.

Since he had no money, the only capital he possessed was his student loan “float.” Instead of spending it, he invested it and by the time he graduated, he had turned it into one million dollars. Back in China, he found companies that went on to become ten-baggers and even hundred-baggers.

Ladies and gentlemen — this is Li Lu, perhaps the greatest investor of our time.

Charlie Munger saw what this guy could do and made a decision almost unheard of in his entire life. He trusted him with his own personal money to manage. In reality, Munger placed his entire fortune into the hands of a young, unknown man who had once fled China with nothing.

“I’m 95 years old. I’ve given Munger money to some outsider to run once in 95 years. That’s Li Lu.” - Charlie Munger

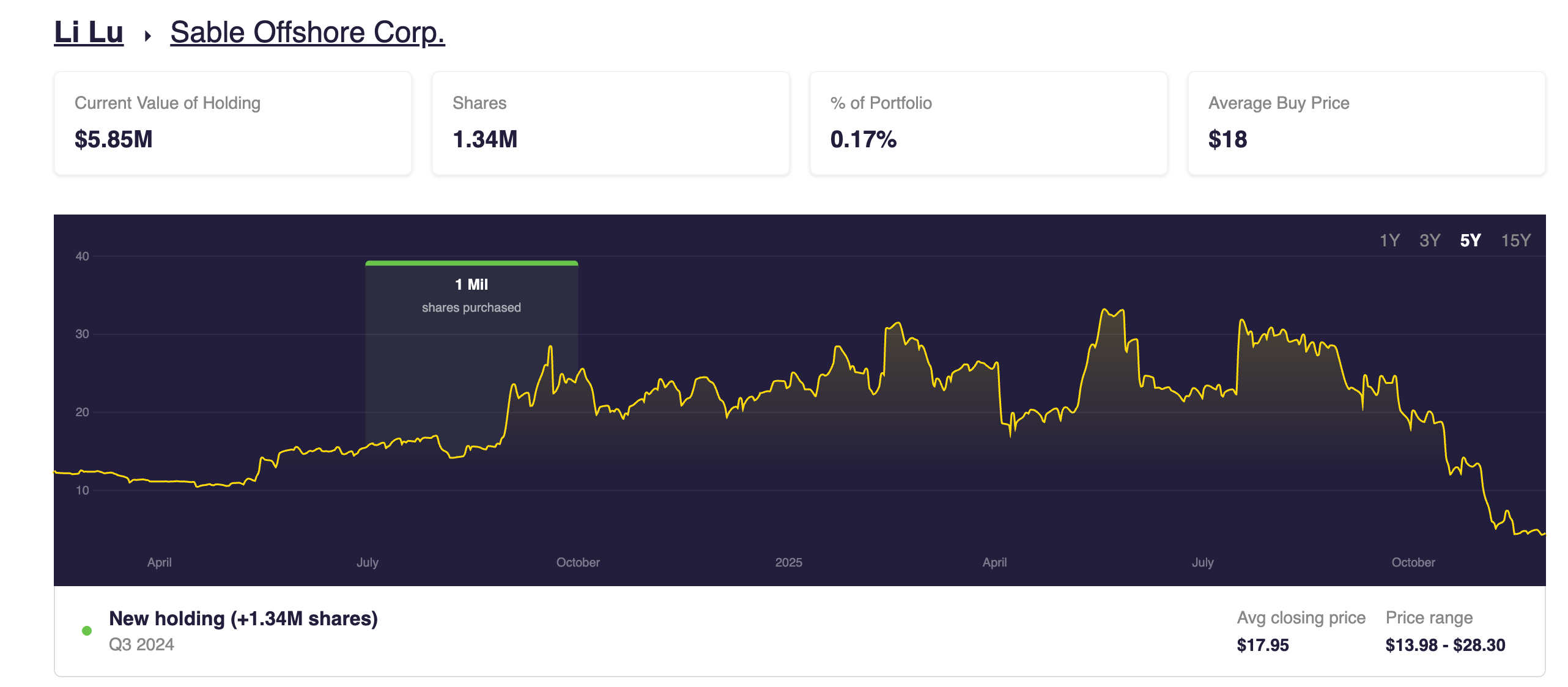

And here’s the detail that truly grabbed my attention. In the summer of 2024, Li Lu bought 1.34 million shares of Sable Offshore Corp. at an average price of about $18 per share.

When I saw that he bought Sable and when the stock dropped significantly, it forced me to stop and look deeper. And maybe it comes down to my investing nature, that I only become interested when things go wrong. Only then can you find something that makes no sense at all. In the stock market we sometimes see anomalies on both ends, either absurdly cheap or absurdly expensive. And yes, I openly admit it, I love free lunches, and I love free movie tickets when everyone else is running out of the theater. I like the idea that this company was analyzed by an investor like him long before I ever looked at it. I like the idea that I can buy the stock at about one fourth of the price he paid. And I like the idea that the worst is probably behind us.

These are special situations.

All of this is more than enough reason to go deep. In this write-up we go as far as possible into the key questions behind Sable Offshore.

What exactly is Sable Offshore

Valuation

Why the Stock Dropped

Key Risks

Upside Scenarios

What Management Is Telling Us

How I expect this to play out

What exactly is Sable Offshore?

Note: This is a high-risk, high-reward special situation with significant uncertainty. Only appropriate for investors who can tolerate substantial volatility and potential permanent loss. Not investment advice.Sable Offshore is a small energy company that bought a very large old offshore oil field from Exxon, called the Santa Ynez Unit. It sits in federal waters off the coast of California. The field may be old, but it still contains hundreds of millions of barrels of oil and could keep producing for decades if it ever restarts.

Why is nothing happening there today? In 2015 the pipeline that carried oil from the offshore platforms to the shore ruptured and caused a spill. After that, California shut the project down. Since then the platforms have been idle, the pipeline has stayed shut, no permits have been approved and the whole project has turned into a political minefield.

When Sable bought the field from Exxon, the plan was simple. Fix the pipeline, reconnect the platforms to the onshore system, restart oil sales and earn billions over the next 20–30 years. On paper it looked like the perfect asset play. In practice, every step has faced resistance.

Regulators in California have blocked almost every move. The Coastal Commission says Sable does not have the right permits. Santa Barbara County may refuse to transfer Exxon’s old permits. The State Fire Marshal says important safety rules are still not met. A California court has said that the Commission has full power to punish Sable.

Meanwhile the company keeps burning cash without earning a single dollar in revenue. With no oil sales, income is zero while costs for labor, engineering, repairs, compliance and legal fights climb month after month.

Valuation

Sable controls a massive, already-drilled offshore field with very attractive economics. This is the largest remaining offshore oil resource in the United States, and one of the cheapest to operate. All the infrastructure is already there. The wells exist. The field works below the surface. The pipeline has been repaired, tested, certified, insured, and is technically ready.

Now let’s make the valuation simple, without DCF models and spreadsheets.

If you wanted to buy the entire company today, the price is roughly $600 million

(about $4 per share). But how much cash can the field generate?

If Sable eventually sells all of its oil and gas over the coming decades at roughly 80 dollars per barrel (the price assumption used in the company’s investor presentation), and still pays every operating cost, every tax and all development capital, the project would generate about 25 billion dollars in cumulative free cash flow over its life. In other words, at today’s valuation you are paying only around two to three cents for every dollar of cash this field could produce.

And it doesn’t stop there.

Last year, management publicly stated that they planned to pay around $4 per share in annual dividends once production resumes and the stock today trades at $4. In their latest presentation, they also emphasized that free cash flow will be returned to shareholders through dividends, and share buybacks. That is what makes Sable a true special situation.

My ideal stock screener: Offshore? Yes. Huge reserves? Yes. Buybacks? Yes. Down 90%? Hell yes, now I’m interested and slightly too excited. 🙂

Why the Stock Dropped

The stock did not fall because the field changed. It fell because the financing picture suddenly worsened.

On 3 November 2025, Sable announced that Exxon had pushed the loan maturity to March 2027 on harsher terms. The rate went from 10 percent to 15 percent, and Sable now had to raise at least 225 million dollars of new equity. The stock dropped about 25 percent that day.

On 10 November, Sable raised 250 million dollars at 5.50 per share, issuing about 45.5 million new shares and taking the total share count to roughly 145 million. Existing holders were heavily diluted and the stock was down roughly 40 percent in total. If you owned 1 percent of Sable before November 10, you owned only about 0.4 percent after the raise. Analysts now think that getting to first oil will require about 2 billion dollars in total capital.

But this does not matter much if you are a new shareholder. It only hurts if you bought earlier. For a new investor, the damage is already priced in. The question is what happens from here.

The 250 million dollars raised covers only a fraction of what is needed. The debt load is still heavy, and on 4 November 2025 Santa Barbara County rejected Sable’s request to transfer Exxon’s old pipeline permits, another setback.

Because the 2015 pipeline is still offline and unlikely to restart, Sable is pushing an alternative plan called offshore storage and treating, using a converted tanker for storage and processing. This would bypass the blocked pipeline but requires about 450 million dollars of extra funding and several new federal permits.

In total, Sable has raised about 475 million dollars but still needs billions more. If it cannot secure that money and clear the legal issues, the contract with Exxon forces the assets to be returned. Regulators have already imposed an 18 million dollar fine and filed dozens of lawsuits over unauthorized work.

Key Risks

Sable Offshore today is a very high risk situation. The odds of successfully restarting production currently look low because the company needs enormous capital and key permits that it does not yet have.

The biggest problem is politics in California. This is probably the toughest anti-fossil regulatory environment in the U.S., and the whole project depends on a long chain of state-level permits and environmental approvals. Every delay directly threatens the company’s survival. Geographically, the field sits right off the coast of California, a state whose political identity is built around climate policy and anti-fossil symbolism. For the environmental lobby, Santa Barbara activists, local politicians, climate NGOs and even celebrities along the coastline, this project is a symbolic battlefield and their flagship fight against offshore oil.

On top of that, the finances are tight. In its own filings, Sable has already disclosed “substantial doubt” about its ability to keep operating without a restart. If delays continue, the company can simply run out of cash and end up insolvent.

There are also serious operational risks. The platforms, pipeline and processing system have been idle for more than ten years. Corrosion, equipment failures, weaker-than-expected flow rates and extra repair costs are all realistic outcomes.

Upside Scenarios

The upside comes from several independent paths that can unlock value, even if California keeps resisting.

First, the pipeline could still get approved by the California State Fire Marshal. But the chances are low, because California regulators have consistently tightened requirements, added new conditions, and shown no political appetite to let this pipeline restart.

Second, if Newsom blocks or delays approval, the Trump administration has every reason to step in, fully aware of how strategically important domestic oil supply is. Any federal move could trigger another sharp re-rating. I think this is the most realistic outcome.

Third, even in the worst case, Sable can bypass California by using a tanker solution. Oil would flow from the platforms into a converted tanker offshore, where it would be stored and then shipped directly to Asia. Operating costs are higher, but the price difference works in Sable’s favor. In this setup, California oil ends up in Asia instead of the U.S.

And to emphasize — Exxon does not want this field back. They left California to escape the liability and have zero interest in returning to this regulatory mess — something their own seller note makes obvious. Forcing a bankruptcy just to reclaim an asset they deliberately exited makes no sense, and if the field becomes more valuable, it only becomes easier for Sable to refinance the note with private credit.

What Management Is Telling Us

After listening to Jim Flores talk about Sable Offshore, it is clear that management sounds extremely confident and optimistic. But it’s worth remembering that every CEO on the planet sounds optimistic, because if they didn’t, they wouldn’t remain CEOs for long. Their tone has to be taken with caution.

Still, there are still a few genuinely positive elements in what they’re saying. The permits they need are valid, which removes a huge part of the uncertainty. It also seems clear that the federal level is far more supportive now than it was just a few months ago. On top of that, they claim to have access to financing options that could make the whole project much cheaper to fund than investors previously assumed. And perhaps most importantly, their new plan for moving the oil no longer depends on California, which has been blocking them for years.

But I need to separate the story they’re telling from the actual numbers behind it. Here is what the numbers say. To move from today to first oil and stable production, Sable needs roughly $2.2 billion.

$900M to take out Exxon

$500M for the OS&T vessel + capex

$300M for LOE and G&A through early 2027

$500M for abandonment bonding obligations

They do not have this money — not even close. Flores openly admits they will need a $100–200M “patch” soon, just to stay alive until the larger federal-backed financing package arrives. That patch is the single biggest near-term risk for shareholders. Behind all the optimism sits a very real liquidity problem.

How I expect this to play out

I think Trump is very smart on these issues, and my base case is that his administration steps in, pushes this out of California’s hands, and moves the whole process to the federal level. Support for green policies is fading rapidly, just as we’re seeing now in Canada.

The second scenario is the tanker route. California blocks everything, so Sable bypasses the state entirely by storing and loading oil offshore and sending it directly to Asia. This keeps the project alive even without the pipeline.

Let’s summarize this as simply as possible.

On one side, you have a company sitting on a huge, already-drilled, low-cost offshore field with massive reserves. The current share price has nothing to do with the real value of this asset and after a 90% drop, the actual risk is much lower than before. You also have a Trump administration that supports offshore production, and a country that does not want structurally expensive gasoline. Then there’s Li Lu, who was buying the stock at $18. And over the last two years, insiders have bought around 8.2 million shares, putting about $95 million of their own money into the stock — an extremely high insider ownership level for a company of this type.

On the other side, we have aggressive green politics pushing to kill the project through bans, delays, lawsuits and constant public pressure. All of this can theoretically drag the process out long enough that Sable simply runs out of time, fails to raise the remaining capital, and ends up in bankruptcy.

This is a true special situation with both high risk and high potential reward, but my own preference has always been for setups where the downside is small and the upside is meaningful. When you look at the whole picture, the most realistic outcome is that the project survives in some form, but existing shareholders are likely to face heavy dilution, far more than management currently suggests. They can now issue new shares potentially at around 3 dollars, which means we could still see another 50 percent downside from today’s price. I don’t like dilution, I prefer buybacks, not issuing more shares. I believe investing should focus almost entirely on the downside. And here, the downside isn’t well protected. So I’ll probably pass on this opportunity.

But I haven’t made a final decision yet and need more time to think this through, so please share your thoughts in the comments — every perspective helps and I’ll be reading everything.

Below is a 2006 masterclass talk by Li Lu, where he walks through his Timberland investment in detail, which is one of the cleanest examples of pure value investing you will ever see.

Quick note:

I want to thank everyone who reads and supports this project, so I’m giving away one full year of paid membership. To enter, just restack any of my posts (or this one), then come back to the chat and write “Shared” or “Restacked.” I want one of you to experience the full premium access for an entire year. The winner will be selected at random on December 7, 2025.

Cheers, Sandro

Shared

Never happen. It’s California, ie, BANANAS: Build Absolutely Nothing Anywhere Near Anybody.

They couldn’t even permit an offshore LNG regas terminal, and that was under Schwarzeneggar.

Remember, Li Lu can afford to lose money: most of us cannot.