Athabasca Oil (ATH.TO): Trading at 5% of Liquidation Value

Without Debt and Returning 100% of FCF to Shareholders

I don’t often bring a new position into my portfolio, but today I have one that genuinely excited me — the kind of excitement usually reserved for something far more… personal. :)

This company is relatively small, forgotten, and carries zero net debt. It trades around a $2.3 billion market cap, yet it’s reasonably certain (even at today’s depressed product prices) that it will generate roughly $50 billion in free cash flow over time. In other words, it’s trading at about 5% of liquidation value.

Put differently, you’re paying just 5 cents today for every dollar the business is set to produce. And what excites me the most is that the company is effectively returning 100% of FCF to shareholders through buybacks.

Here’s what I’ll cover:

Buffett’s early investments – how he deployed small amounts of capital in the beginning

The business model

The industry

Price vs. intrinsic value

My portfolio update

Buffett’s early investments

“He’d find something that was selling for one-fourth of liquidating value. He’d load up. So for a long period of time, he had a happy hunting ground. All he had to do was go through lists of liquid securities and slowly buy them, and he could get these ridiculous bargains.” — Charlie Munger

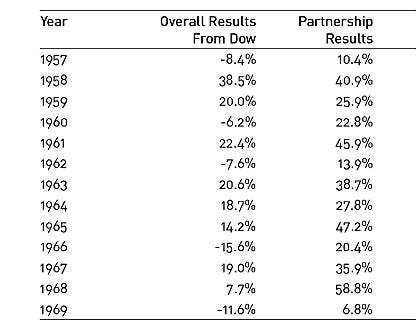

I’ve been digging into how Warren Buffett invested when he had only a few thousand dollars of capital in the early days. What stood out to me is how poor the overall market was between 1957 and 1969. During that stretch, the Dow Jones returned only about 4–5% annually, while Buffett’s partnership compounded at over 30% per year – in a bad market environment. At that pace, his investments were doubling roughly every 2 years.

How did he manage that? Very simply: he bought businesses trading far below their liquidation value. These companies were, so to speak, worth more ”dead than alive” compared to how they traded on the stock market. These were small, forgotten companies, and Buffett never invested with the assumption that the market would later award them a high earnings multiple (as most investors think today).

Fast forward to today: with AI stocks trading at some crazy earnings, I believe it’s far more sensible to focus on simple businesses generating real free cash flow. If you invest in Tesla now with a P/E of 250, good luck with that. It means you’re paying 250 times the company’s annual earnings. Mathematically, if earnings stayed the same and everything was paid out to you, it would take 250 years to get your money back. In other words, the market has already priced in strong future profit growth. And there’s always the possibility that the market will cool off at some point. Nothing against Tesla, but the valuation looks pretty overheated to me.

“Think about a company with a market cap of $500 billion. To justify paying this price, you would have to earn $50 billion every year until perpetuity, assuming a 10% discount rate. And if the business doesn’t begin this payout for a year, the figure rises to $55 billion annually, and if you wait three years, $66.5 billion.” - Warren Buffett

In the 1950s and early 1960s, Buffett invested in a range of “ordinary” companies, for example:

Marshall Wells – shoe retail chain - P/E 5

The Greif Co. – paper packaging and barrels - P/E 4

Cleveland Mills – textile manufacturer - P/E 3

Union Street Railway – local transport operator - I can’t find the exact P/E, but the company had cash on the balance sheet of $48.13 per share while trading around $30 per share.

Philadelphia and Reading – railroad - P/E 7

American Express (AmEx) – financial services and charge cards- P/E 14

Studebaker – automobile manufacturer P/E 6

When I analyzed Buffett’s early investments, I noticed a clear pattern: almost all of these companies traded at 25–50% of liquidation value. The first three ideas (Marshall Wells, The Greif Co., Cleveland Mills) generated “okay” returns, but nearly all the others delivered extraordinary results.

The difference? The more successful ones were shareholder-friendly. They returned part of their free cash flow to investors through dividends, which both supported the stock price and delivered cash directly to Buffett. The market recognized this later, awarded a higher multiple plus dividends, and that led to extremely strong results. It’s that simple.

None of them, however, were returning anywhere near 100% of FCF to shareholders – only a portion. And buybacks didn’t really exist back then.

Today, buybacks are often the more powerful way of returning capital: if a company grows and stays profitable while reducing its share count, returns can become extraordinary. A classic case is NVR, where the stock went from $5.50 to nearly $10,000 as the company repurchased over 80% of its own shares.

Now, when I look at my own portfolio, I see clear parallels.

Valaris: the replacement value of its rig fleet is around $30 billion, while the company trades at just over $3 billion in market cap. On that basis, it’s trading at about 10% of liquidation value. And it’s reasonably certain that over the coming years Valaris will generate about $1 billion of annual FCF.

Alpha Metallurgical Resources: I built my position below a $2 billion market cap, yet the company controls about 800 million tons of premium met coal reserves and resources. Based on reasonable assumptions, those reserves could generate between $50–80 billion in FCF over time. That means AMR is effectively trading at only 2.5–4% of liquidation value, depending on the price of metallurgical coal.

Both companies have no debt and will effectively return all free cash flow to shareholders – which, in my view, might be even better setups than Buffett’s earliest investments.

So Warren, if by any chance this ever lands on your desk, I hope I’ve done you proud. I get it — you can’t touch small-cap companies like these anymore. Too much capital, too few opportunities, and a universe that shrinks as your size grows.

Me? I’ve got the opposite problem: too little money, too many ideas. The playing field is wide open, but the stakes feel small.

Still, maybe one day I’ll have the privilege of facing your kind of “problem” — too much cash to deploy, not enough places to put it. Until then, I’ll keep fishing in the ponds you no longer can.

My new idea is trading at roughly 5% of liquidation value. All of its free cash flow is going straight into buybacks, and the debt? Just paid off. A forgotten business, a clean balance sheet, and capital returns at full throttle – beautiful.

Let’s dive in.