Alpha Met Resources vs. Warrior Met Coal

Which company is the better long-term bet ?

In the Indian epic, written several thousand years ago, called Mahabharata, one of the heroes is a great warrior and archer named Arjuna.

When Arjuna was learning how to be an archer, his teacher Dronacharya decided to test all the students. He placed a tall pole, and at the end of the pole he put a fish, a sculpture of a fish with a small blue eye. He put the pole into a pool of water and told the students to look at the reflection of the fish in the water and to hit the eye of the fish.

The first prince stood, and before he released the bow, the teacher asked him: “What do you see?” The prince answered: “I see the water, the pole, the fish.” The teacher told him to sit down, because he was not ready.

The second prince stood and said he saw the pole, the fish, and the eye of the fish. Again the teacher told him to sit down. One by one, the princes said what they saw, but none were ready.

In the end, Arjuna stood and the teacher asked him what he saw. Arjuna answered: “I see only the center of the fish’s eye.” The teacher told him to shoot, and Arjuna hit the eye of the fish.

So let’s aim straight at the eye and see which is the better investment:

Alpha Met Resources or Warrior Met Coal.

Metallurgical coal is my lifetime bet — and so are the companies producing it. I have already written about the industry in this post.:

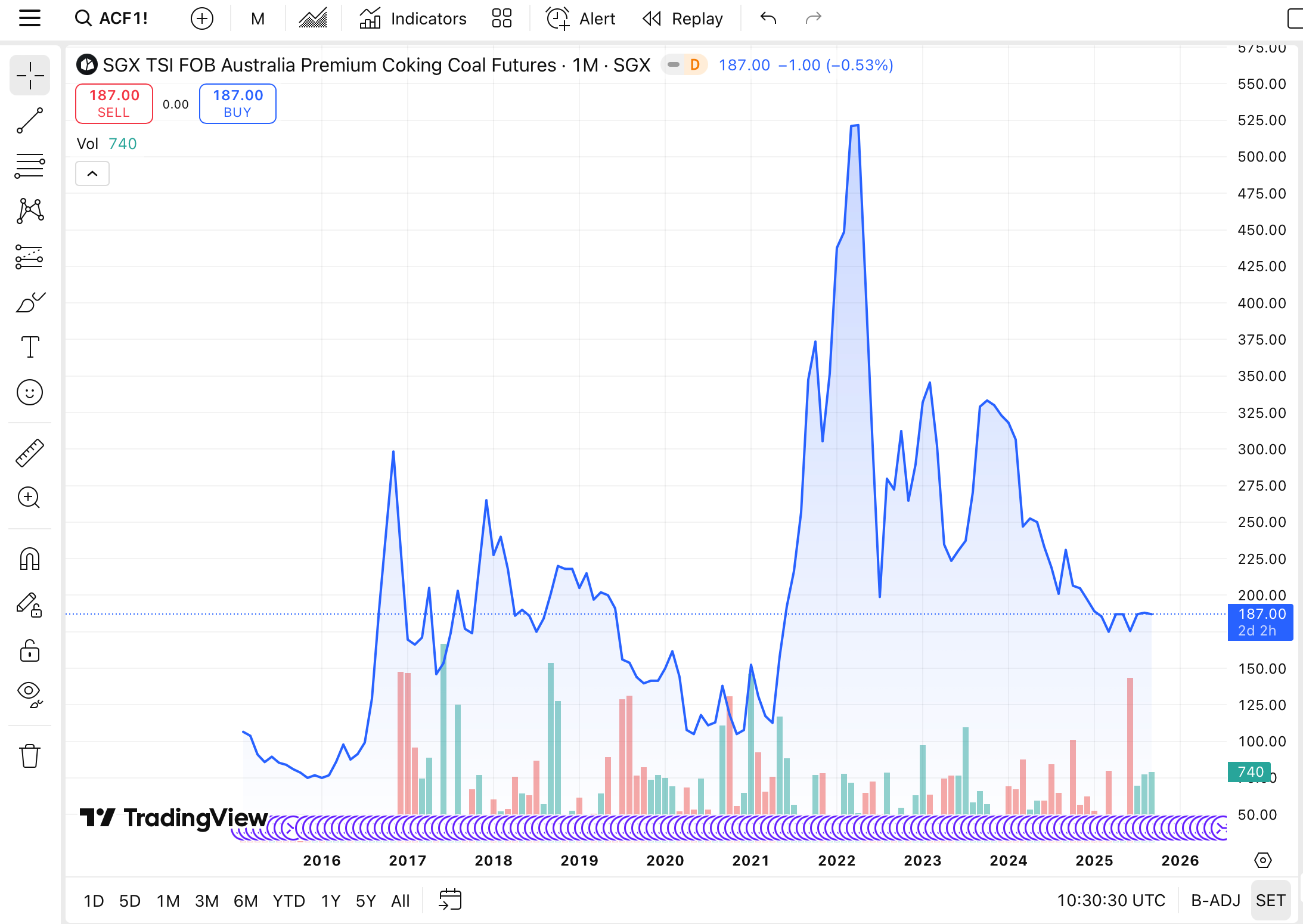

What fascinates me about the coal market is that it’s almost never balanced. It either feels like it’s asleep — like today, with prices depressed and valuations ignored — or it’s in total shock, like in 2022 when prices exploded to unprecedented highs.

After years of working inside the coal industry, I see things that make today’s market valuations look completely irrational. The future of met coal, in my view, is bright: the world has no real substitute, supply is structurally fixed, and even a minor disruption can send prices to extremes — like in 2022, when prices spiked to almost $600/ton and companies like AMR and HCC printed cash at historic levels.

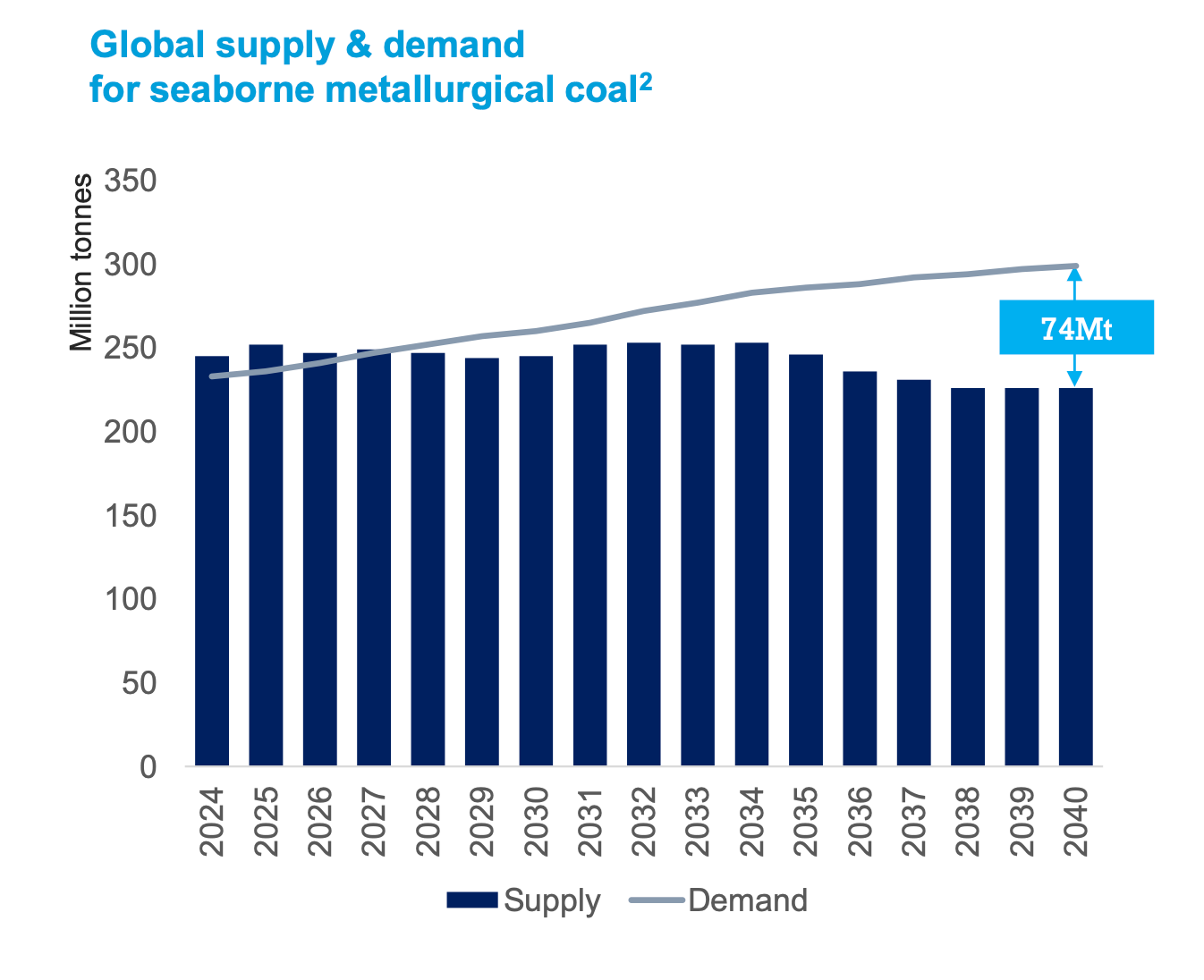

From 2028 onward, I believe we are entering a new era: structural deficits, consistently high prices, and occasional super-spikes. At that point, met coal may stop being “cyclical” in the old sense and instead become a scarce, strategically indispensable resource.

But why not just wait until 2028 to invest in these companies?

The problem with that approach is timing. 2028 may mark the start of the organic deficit, but prices don’t move on calendars — they move on shocks. A war, a flood in Australia, a bankruptcy, or an accident can send prices soaring overnight, long before the “official” deficit begins. I can’t predict when such an event will happen, which is why I prefer to build my position now. I’m paying little today, happy to add if prices dip, and treat those shocks as free upside options.

One scenario already on the horizon is Ukraine. I believe it’s realistic to expect the war to end within the next one to three years, followed by reconstruction. If Ukraine were to rebuild, demand would rise by around 15 million tons per year – and I have no idea where that supply would come from. That single event alone could make coal prices explode, not for just a single year but spread over five or six. And if further disruptions occur, the shortage only deepens. Mines that shut down rarely reopen — when capacity disappears, it is often gone for good.

So the real question for investors: which company is the better long-term bet — Alpha Met Resources or Warrior Met Coal? In this post I break down in detail the risks, profitability, cost structures, capital allocation, valuation, reserves and resources of both companies.

Risks

Coal mining carries an inherent danger: underground explosions. They are usually triggered by an accumulation of methane gas or coal dust, ignited by a spark or electrical equipment. While rare, these events are catastrophic — they kill workers, halt operations for months, and can even lead to permanent closure of a mine.

Recent and historical examples show the scale of this risk:

Tabas, Iran (2024): Methane explosion killed at least 51 miners and injured 20; mine shut down pending investigation.

Bulla Loca, Venezuela (2024): Illegal gold mine collapse and methane-related blast killed at least 15 miners.

Çöpler, Turkey (2024): Landslide at a gold mine buried 9 miners alive; operations suspended.

Yanaquihua, Peru (2023): Fire caused by electrical short circuit killed 27 miners in a gold mine tunnel.

Welkom, South Africa (2023): Methane explosion in an abandoned gold mine killed at least 31 illegal miners.

Pniówek, Poland (2022): Series of methane explosions nearly a kilometer underground killed at least 5 miners, >20 injured.

ČSM Karviná, Czech Republic (2018): Methane explosion killed 13 miners and injured 10.

Halemba, Poland (2006): Methane/coal-dust explosion killed 23 miners.

Sago Mine, USA (2006): Methane built up in a sealed section; 12 miners died, 1 survived. Mine permanently closed.

Upper Big Branch, USA (2010): Coal-dust explosion killed 29 miners, the deadliest U.S. mine disaster in decades.

Moura No. 2, Australia (1994): Methane/coal-dust explosion killed 11 miners; after a second blast, the mine was permanently sealed.

This is where company structure matters.

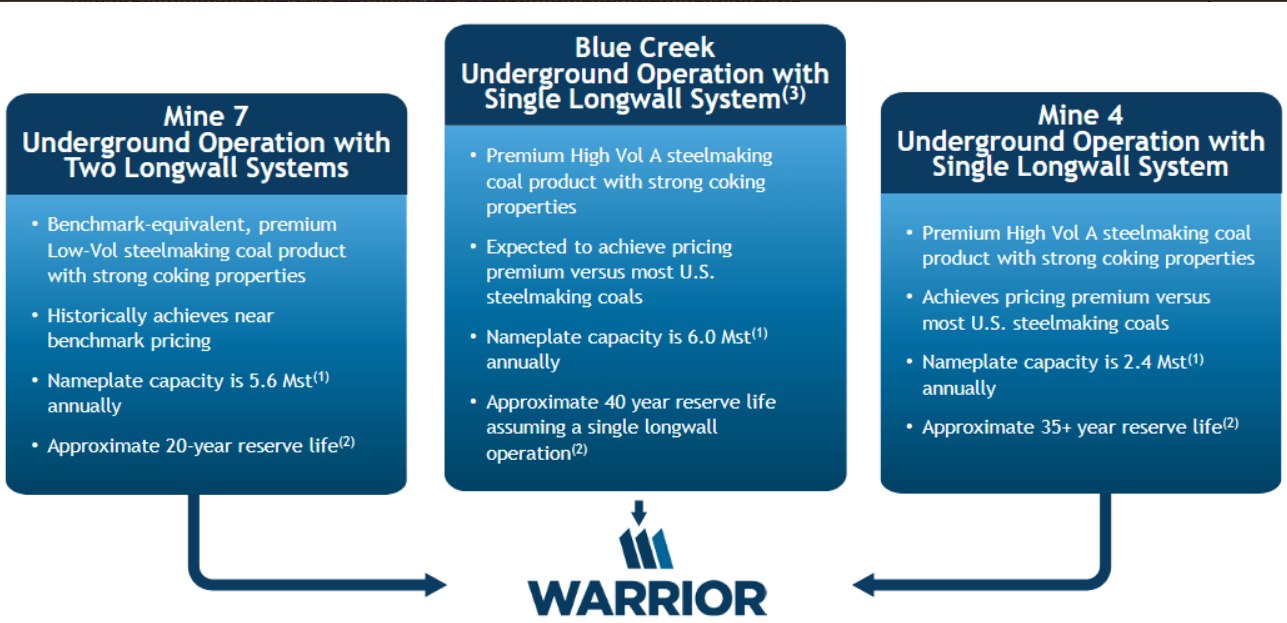

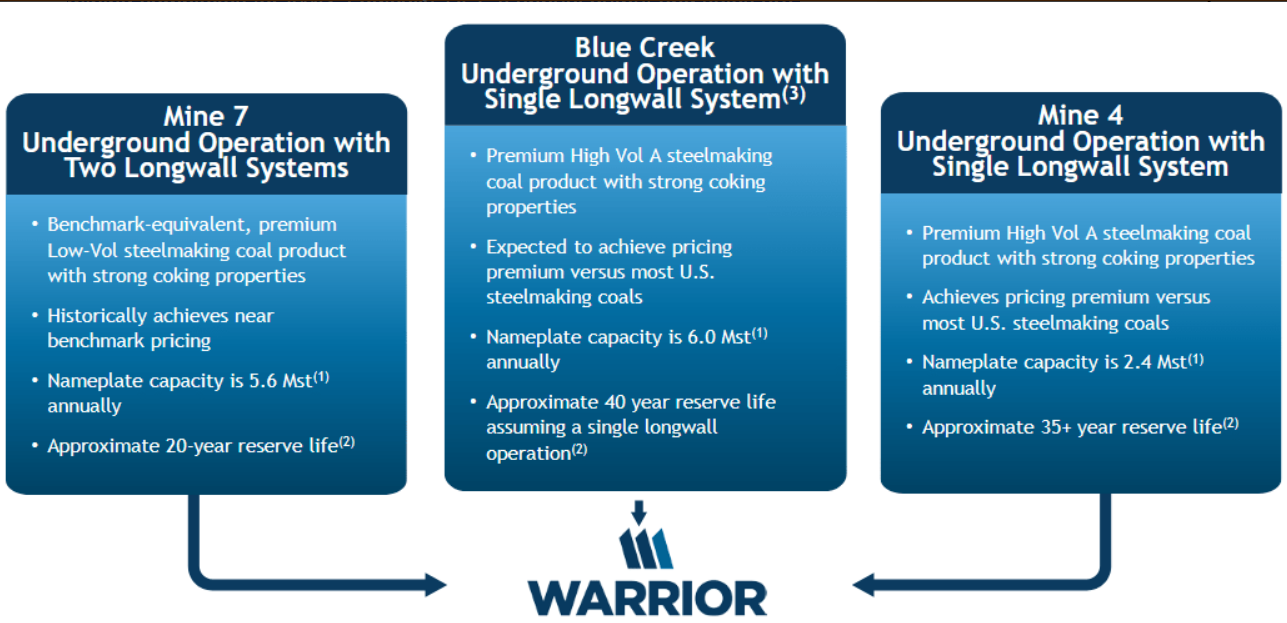

HCC operates only three mines — Mine 7 and Mine 4, both dating back to 1974, plus the new Blue Creek mine that began operations in 2024. All three are underground, concentrated in a single region southwest of Birmingham, Alabama.

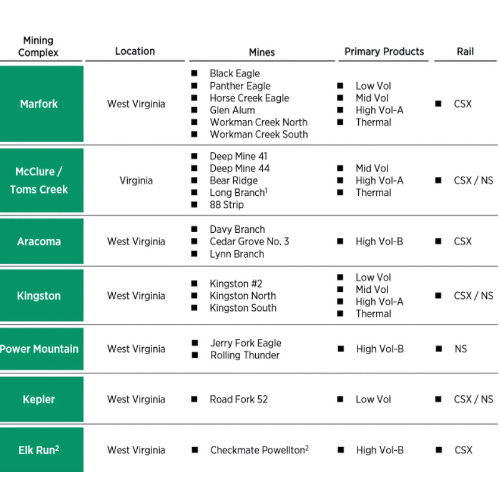

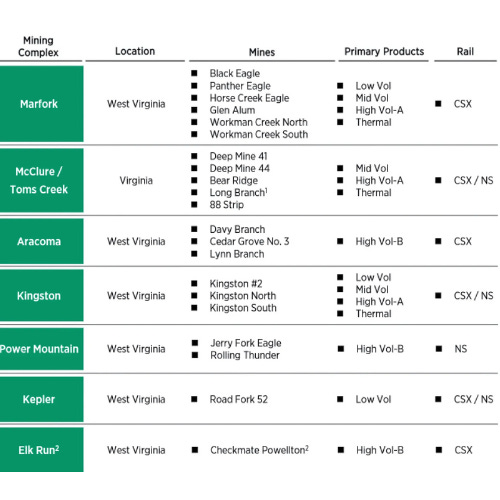

Alpha Met Resources, on the other hand, operates 21 mines across seven different complexes, with a mix of underground and surface operations. Its output is more than double that of HCC.

The implication is clear: if an explosion shuts down one of HCC’s mines, a third of the company’s production disappears overnight. If AMR faces the same event, production continues at twenty other sites. Blue Creek is modern and built with the latest safety measures, but the concentration of risk remains.

This structural difference makes Alpha Met Resources far more resilient to operational shocks.

1–0 for Alpha Met Resources. Let’s move on.