Alpha Metallurgical Resources (AMR): Deep Analysis

Why This Is My Lifetime Bet

Created with TradingView

Introduction

My lifetime bet is coal. Metallurgical coal. As of August 2025, Alpha Metallurgical Resources makes up around 50% of my portfolio. I don’t think I’d mind if it were 70%—or even 100%. If I had to put all my wealth into a single stock, it would be Alpha.

There are two very different types of coal: thermal and metallurgical. Thermal coal is mainly used to generate electricity and can be partly replaced by natural gas, renewables, or nuclear. Metallurgical coal, on the other hand, has no large-scale substitute today—it’s essential to produce iron and steel. Without it, civilizations don’t get built. Every building, every bridge, every “layer of growth” around us depends on steel, and primary steel still needs met coal.

Metallurgical coal, unlike thermal coal, exists only in a few geographic regions: Australia, Canada, the United States, and to some extent in Mongolia and Russia. That’s more or less where the list ends.

Some kind of competition to metallurgical coal is Electric-arc furnaces EAF. That means recycled steel is used, which doesn’t require coal, to produce new steel. However, if you want a civilization to grow — for example in India, Africa, or rebuilding Ukraine after the war — you cannot rely on recycled steel. You need new steel, and that comes only from metallurgical coal.

Coal is a four-letter word. It is deeply unloved. ESG pressures, capital restrictions, CO₂ debates, and activists fighting against coal have made the sector one of the most avoided in global markets. Yet the most common cause of low prices is pessimism. That is exactly the environment worth investing in. Not because pessimism is attractive, but because the prices it produces are. Optimism is the true enemy of the rational buyer.

Demand

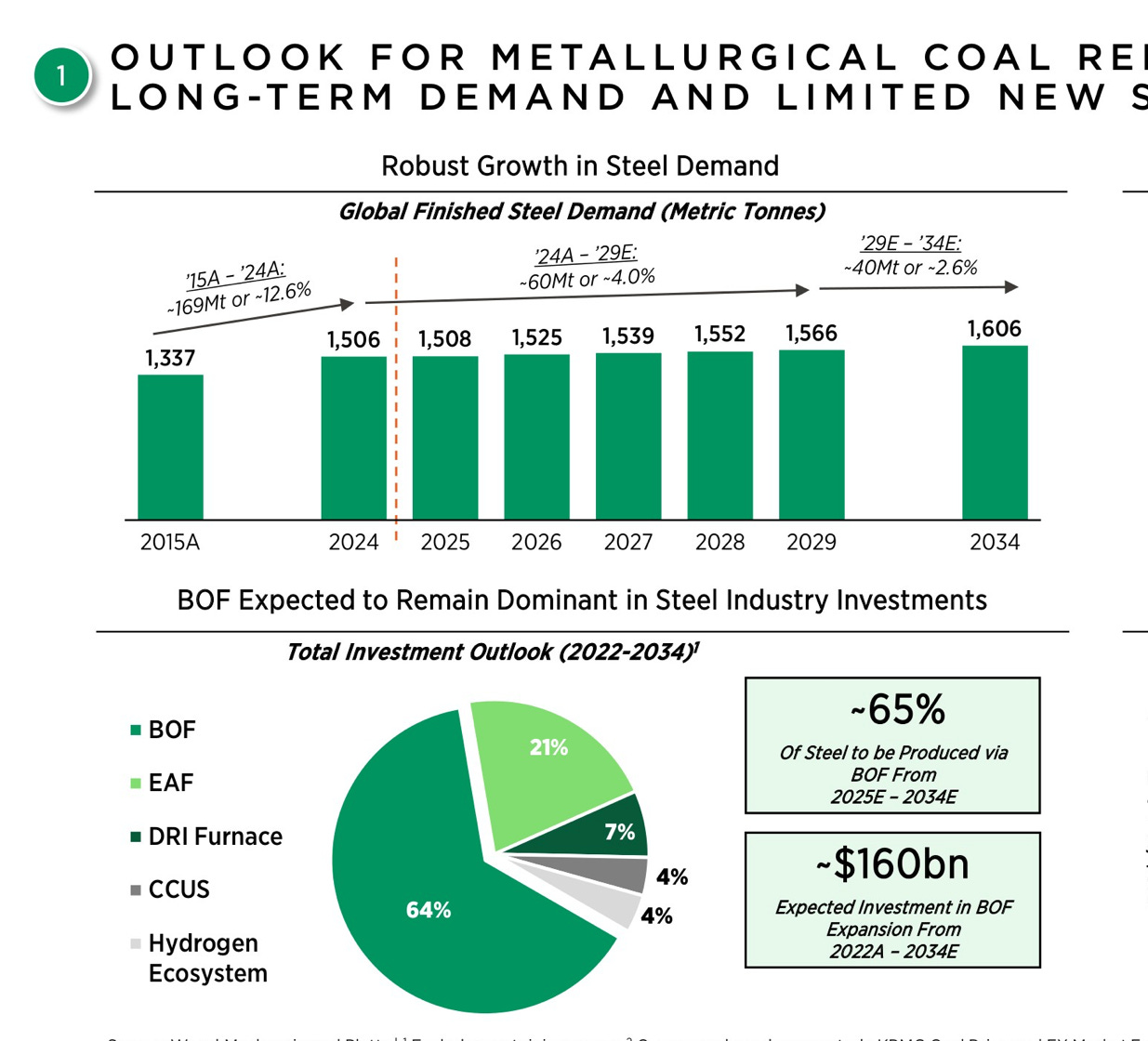

All around the world, new blast furnaces are being built and commissioned – giant industrial plants where iron ore and coking coal are turned into pig iron, the base material for steel. Many more are planned over the next 5–10 years. Each of these furnaces has a lifetime of 40 to 70 years. Building a new blast furnace steel plant costs billions of dollars. No one commits that kind of capital unless they expect the furnace to run for decades. There is still no alternative technology at scale that can replace the blast furnaces route, which means coking coal–based steelmaking could remain dominant well into the 2070s or even 2080s, so coal-based steelmaking remains dominant for now.

Alpha is positioned right in the middle of this reality. Its reserves of premium hard coking coal can last for many decades, matching the lifespan of the blast furnaces now under construction. While Europe and the U.S. are steadily reducing demand by closing old furnaces and shifting toward EAF/DRI, over 300 Mt of new BF capacity is in development globally, mainly in India and Southeast Asia, with Africa just beginning to build integrated steel plants.

This locks in demand:

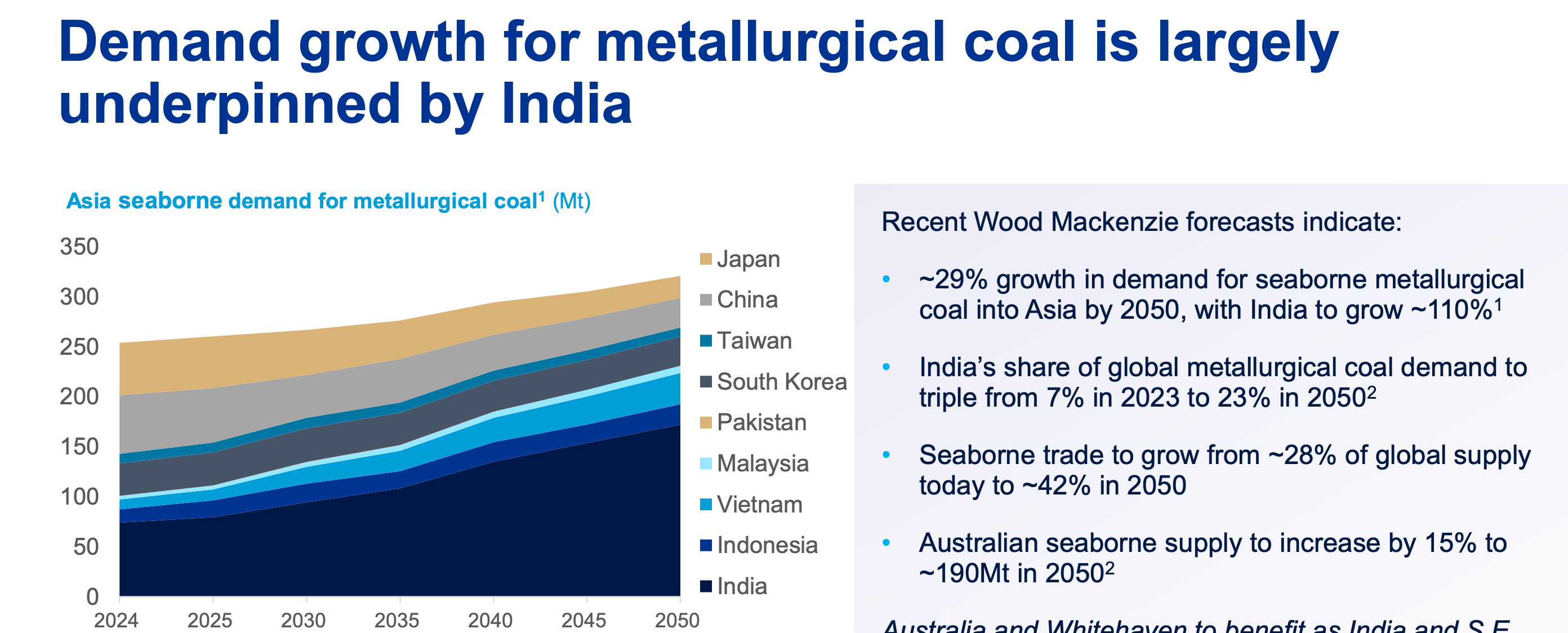

India is set to increase imports from ~90 Mt today to over 200 Mt by 2050.

Southeast Asia adds another 15–20 Mt by 2035.

Africa enters the industry for the first time.

China reduces its demand (from ~70 Mt to ~20 Mt by 2045), but that decline is far outweighed by growth elsewhere.

Europe & U.S. see long-term declines, but they are minor compared to Asia’s expansion.

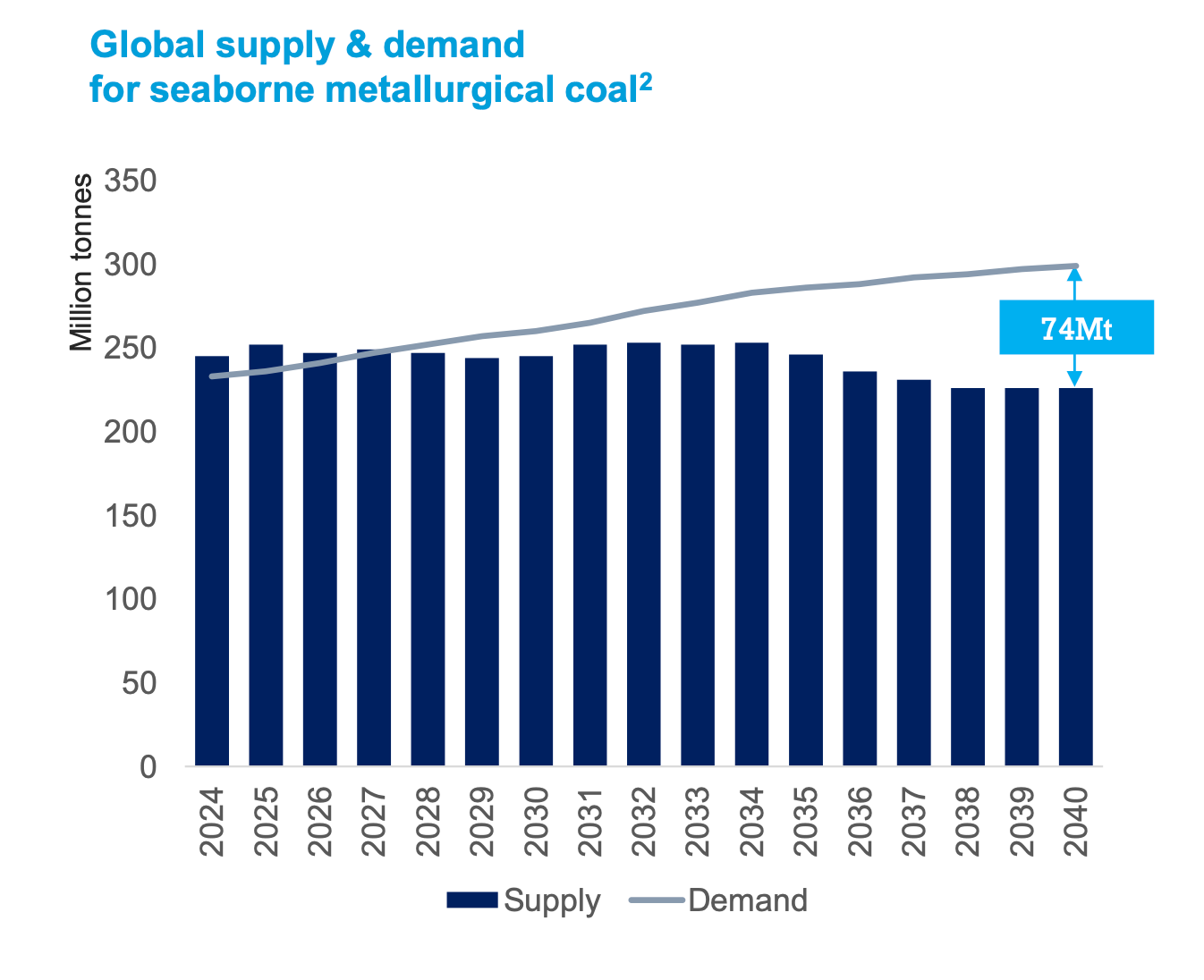

Supply

My bet on met coal is less about demand growth and more about supply.

In short, supply is tight. So if anything happens — for example floods in Australia, regulatory shocks, labor shortages, or mine incidents—that can send prices vertical.

Development of new mines is practically non-existent – the only major project coming online is Warrior’s Blue Creek, and that’s it. ESG pressures, lack of capital, and regulatory barriers mean new mines are not being built, while existing mines in Australia, the U.S., and Canada are gradually depleting and shutting down.

On top of that, low prices are already pushing higher-cost producers into bankruptcy – Corsa Coal and Coking Coal LLC are recent examples. And accidents also take capacity offline: explosions like the one at Anglo American’s Grosvenor mine in Australia have forced closures and cut output.

And what happens when a mine shuts down? Once a mine shuts down, restarting it is extremely complicated. When a mine shuts down, all workers are laid off, all equipment is removed and sold as owners try to recover as much money as possible. The equipment is gone, the workers are gone, and often the mining license expires too, since it requires continuous fees and taxes to be paid.

The first obstacle in restarting is financing. Any restart would have to be funded entirely with equity, which is unusual in mining. Even if capital were raised, there is no certainty about where coal prices will be in six months, a year, or three years. Who would be willing to invest in such uncertainty? A $300 price might last three weeks or three years – nobody knows. That makes raising capital very difficult.

The second problem is the lack of miners. It takes years to develop mining skills; you can’t just post a job ad and immediately find skilled workers. If former miners have moved on to other jobs or industries in the meantime, bringing them back would be very hard – especially if the coal price is already high again.

The third obstacle is equipment. Just like in Korean shipyards, there are delivery delays of 2–4 years. Mining equipment manufacturers now have the upper hand, so acquiring new equipment would be slow and expensive.

Even licenses can be problematic depending on the location, since coal today is seen as a “dirty word” in environmental and regulatory discussions. Unlike office buildings, where financing and tenants are somewhat predictable, mining is far more uncertain.

In short: once a mine shuts down, it stays shut. No new supply is coming while most existing mines are depleting. Demand keeps rising. Long term, I expect high met coal prices—and if a new war or black swan event occurs, I expect extremely high prices.

The coal sector today is going through an even more intense boom-and-bust cycle than before. From an investment perspective, understanding this model can provide huge advantages. If you enter the industry at the right time in the cycle, the results on the other side can exceed all expectations. Growth can be spectacular. That’s why investing in companies that are debt-free, with low production costs and strong market positions, is extremely rewarding. They may suffer small losses in bad times, but in good times they deliver exceptional profits.

In a Highly Cyclical Business, You Need a Low-Cost Producer

I’m saying this because I want to maximize downside protection. My view is that next year, with Blue Creek coming online, supply will slightly exceed demand. But from 2028 onward, the situation changes — I don’t think this will even be a cyclical business anymore, at least not in the way it used to be.

Coal mining is an unusual branch of the mining industry. The first reason is the war in Ukraine and the extremely high coal prices in 2022. All of these companies today are debt-free (Alpha, Warrior) – they paid back every cent, something that had never happened before. Mining and coal companies had always carried debt, and that was usually the reason they got into trouble – prices dropped, the cycle turned down, they couldn’t service their debt, went bankrupt, and the cycle repeated. But in 2022 and 2023, we saw a situation where many coal companies had net cash – something that had never been seen before.

Take a downturn in the metallurgical coal market, when prices are too low and everyone is losing money or just barely surviving. What happens is that high-cost mines eventually have to shut down, because they can only run at a loss for so long while hoping for a recovery. If the downturn lasts long enough, they are forced to close. Right now, prices for metallurgical coal are indeed low, and many mines in Appalachia and around the world have already closed.

But if you look at companies like Alpha and Warrior, you’ll see they produce premium met coal, hold large reserves and resources, and operate at the low end of the global cost curve. This means that this companies will likely be the last ones standing in any downturn, and the hardest of all to go bankrupt.

Price Is What You Pay, Value Is What You Get

So, what’s the price? The market cap is about $1.8 billion, or around $150 per share.

What do I get? A debt-free company, with the best balance sheet I’ve ever seen – absolutely fantastic. A very strong management team (I believe the best in the industry), with outstanding capital allocation skills and a business that, over a full cycle, can generate substantial free cash flow. Capital returns have been aggressive: the board authorized up to $1.5B for buybacks, and the company has already executed over $1B, retiring a large chunk of shares. And I am getting a lot of coal. A lot. You know, they hold a ~300 million short tons of reserves and ~500 million short tons of resources for a combined total of about 800 Mt – equal to roughly ~46 years of mine life.

It’s also notable that U.S. policy recently classified metallurgical coal as a critical mineral, formally recognizing its strategic importance for steel and supply chains..

And let’s not forget – over the last three years the company has generated around $2.5 billion in pure free cash flow, yet today it trades at only $1.8 billion market cap. Whaat?!

Similarity of a potential 100-bagger

There’s a fascinating study that tracked 100-bagger stocks over a 10-year period and looked for their common characteristics. To keep it short, the majority of these companies were profitable (82%), relatively small in size, and trading at attractive valuations — typically EV/EBITDA below 10x and EV/Revenue below 1x. Most of them came from cyclical industries or were classic turnarounds. The highest share of 100-bagger stocks shared exactly these traits.

So does Alpha share some of these 100-bagger characteristics?

Profitability: Alpha is a cash cow. Yes, in a cyclical business there will be weaker years, but over the cycle the company generates massive amounts of cash.

Small size: With a market cap of about $1.8 billion, Alpha technically falls into the small-cap category (generally defined as $300M–$2B). It’s small enough to fly under the radar of most institutions.

EV/Revenue: At 0.39x, Alpha trades well below the 1x threshold seen in many past 100-baggers.

EV/EBITDA: At just 5.0x, it’s comfortably under the 10x mark.

In other words, Alpha ticks many of the same boxes that historically defined early-stage 100-baggers: profitable, small, cheap, cyclical.

But that’s not all. Alpha’s management has made it clear they intend to return almost 100% of free cash flow to shareholders via buybacks. Combine that with the company’s already cheap valuation and strong fundamentals, and you don’t just have the profile of a potential 100-bagger — you have the profile of a 100-bagger on steroids.

There Are Only Three Scenarios

Scenario 1 (re-rating) : Alpha trades at some kind of “real” or “fair” valuation, in line with other companies generating around $1 billion in annual FCF. In fact, Alpha should arguably deserve a premium since it is debt free, unlike most peers.

For comparison: Ferrari (RACE) makes about $1.3 billion in FCF and trades at an $85 billion valuation. Carvana generates about $0.6 billion in FCF, carries $7 billion of debt, yet trades at a $44 billion valuation.

But coal is not a fancy business. Alpha will never get Ferrari or Carvana multiples. With CO₂, coal stigma, and ESG headwinds, the market simply doesn’t like it. So the chance of this scenario happening is almost zero, but that doesn’t bother me.

Scenario 2 (base case): This is the most likely outcome. When the company continues its buyback program, the market cap itself will grow. If Alpha’s market cap rises from today’s $2 billion to $10 billion, that’s already a clean 5x return. But at that point, buybacks will take longer to “eat themselves,” so to speak.

My base assumption is that the company generates around $1 billion in free cash flow annually. What happens in 15–20 years from now ? Alpha currently has 13 million shares outstanding. They have already bought back a third of the company.

If 75–80% of those are retired through buybacks, only about 3 million shares could remain. If Alpha is still producing $1.5 billion in annual cash flow, that equals roughly $500 per share in earnings every single year.

So what does a business like that trade at? With a P/E multiple of 20, Alpha would be worth around $30 billion market cap, or $10,000 per share. That’s a 66x return from today’s levels. Not bad.

And that’s not the end of the story — because along the way, shareholders still collect 20 years of $1B+ free cash flow, most of which will be returned directly via buybacks. Or dividends.

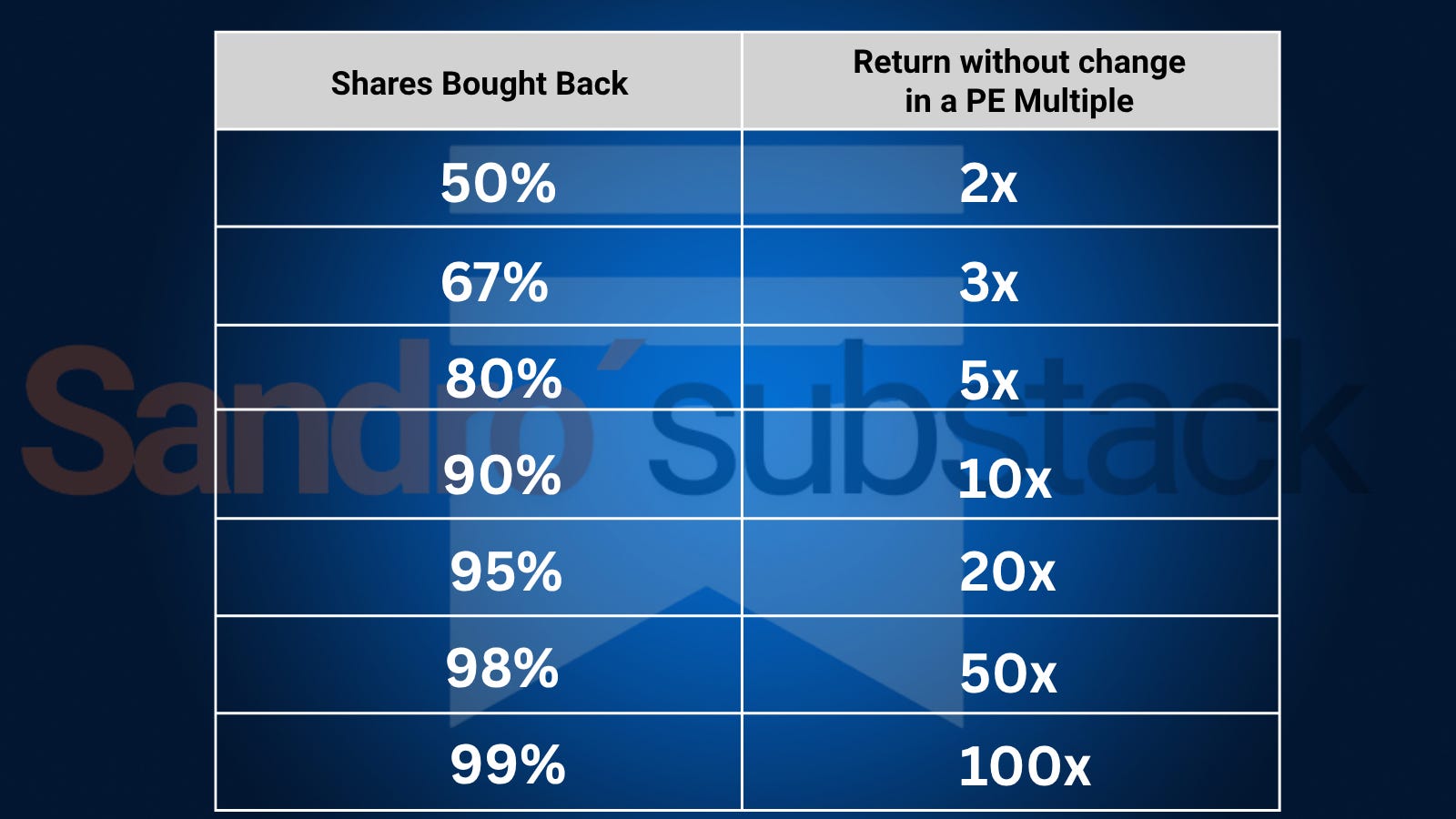

Scenario 3 (Orgasm case) : Many investors simply don’t understand buybacks — and that’s why this scenario is often ignored. Take Alpha as an example: they launched a $1.5 billion buyback program, of which more than $1 billion has already been used. That means the company literally took $1 billion of cash, retired about 30% of itself — and yet nothing happened. The stock price actually went down. Investors want growth, they want dividends. A CEO spends $1 billion on buybacks, and the market yawns. This is deeply misunderstood.

Here’s how buybacks actually work. Up to around 50% of shares retired, nothing really moves. The market doesn’t care. But once you pass that threshold, the math starts to accelerate — the stock effectively doubles. And the real party begins once 90%+ of the company is retired.

Take NVR as the best example: shares outstanding went from 16 million to 3 million — an 81% reduction. The stock price went from $5.50 to nearly $10,000, a return of about 1,800x. It took 30 years, but the compounding was extraordinary.

The third scenario it’s less likely than Scenario 2, but I still think the odds are decent — maybe 30% or more.

In this case, ESG only reinforces the trend: the stock remains unloved, hated, and avoided — exactly what we see today. That would allow buybacks to eventually retire almost the entire company within just a few years. All that needs to happen is for them to keep generating around $1 billion in annual cash flow while the stock trades at a P/E of 3 or 4. No investors, no institutions, only ESG pressures — and that alone could bring us to the promised land in just a few years. For context, let me remind you: after NVR repurchased 80% of its shares, it delivered returns of 1,800x.

The trick with Alpha is simple: never sell, and be the last one holding the stock. That’s why I’m writing this piece. And don’t tell anyone about this post :)

Cheers,

Sandro

Love the math. Easy to understand. Boring is beautiful. 🙏