AutoNation vs AutoZone: The Buyback Deathmatch

Same game. Which buyback cannibal is deadlier?

"It’s a very simple decision, in my view, as to whether you repurchase your shares. You do it if you’re taking care of the needs of the business and if your stock is selling for less than it’s intrinsically worth." - Warren Buffett, 2015 Annual Meeting

AutoNation and AutoZone are not rivals in the usual sense. They sell different things. They show up at different moments. But they are built around the same obsession. Fewer shares.

AutoNation is a dealer. It earns money when cars are sold, when financing is arranged, and again later through service and parts tied to its network.

AutoZone lives in urgency. It earns money the moment something breaks and the fix cannot wait. Speed matters more than price. Certainty matters more than choice. That moment is its moat.

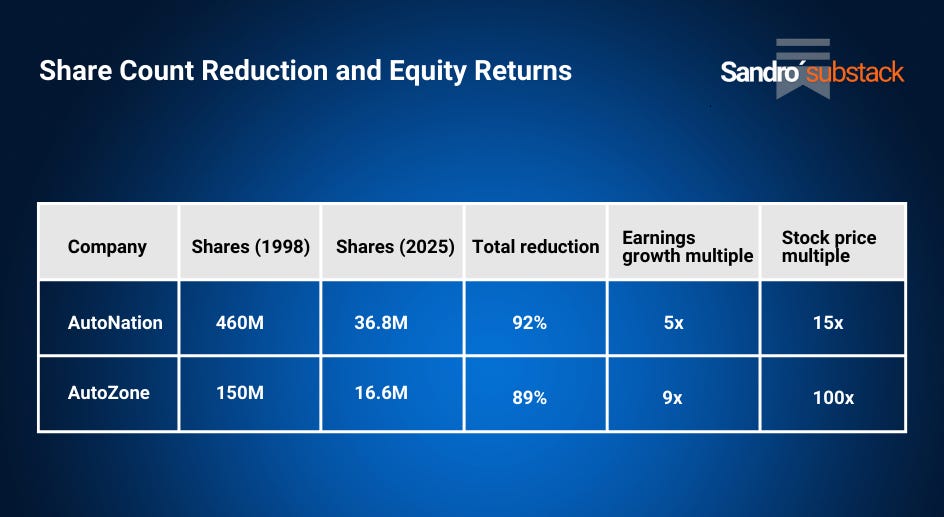

Both have already retired close to ninety percent of their share counts. The only question left is who can chew through the final ten percent faster.

I am grading this matchup on:

Capital allocation

Cash flow quality

Moats

Balance sheet risk

Valuation and buyback torque

Endgame catalysts

Capital allocation

The table tells you everything you need to know about how both management teams think. No dividends. Both companies picked one lever and kept pulling it. Shrink the share count.

AutoNation plays offense. When the cycle is friendly, it pushes hard. When conditions tighten, it slows down. You get volatility, but you also get torque.

AutoZone plays discipline. Earnings rise while the share count keeps shrinking. The business stays boring. The math does not.

There is one extra layer that makes this uncomfortable. AutoZone is willing to borrow to buy back stock. In 2024 it generated about 1.9 billion in free cash flow and spent about 3.2 billion on repurchases. The difference came from debt. That is why equity is negative. For most companies that signals stress. For AutoZone it is the receipt. Capital returned. Profits returned. Then borrowed to return more. With ROIC around fifty percent, the math stays brutal as long as returns stay above the cost of debt.

This is not a story about a good company versus a bad one. Both are dangerous to underestimate. In capital allocation, this fight ends in a draw. Both are brutal cannibals. Just killing shares in different ways.

The only thing left that matters is the endgame. Who can retire the final ten percent faster. And what has to stay true for that to actually happen.