AutoZone Deep Dive: The Cannibal Endgame

The last 10% is where the fireworks start

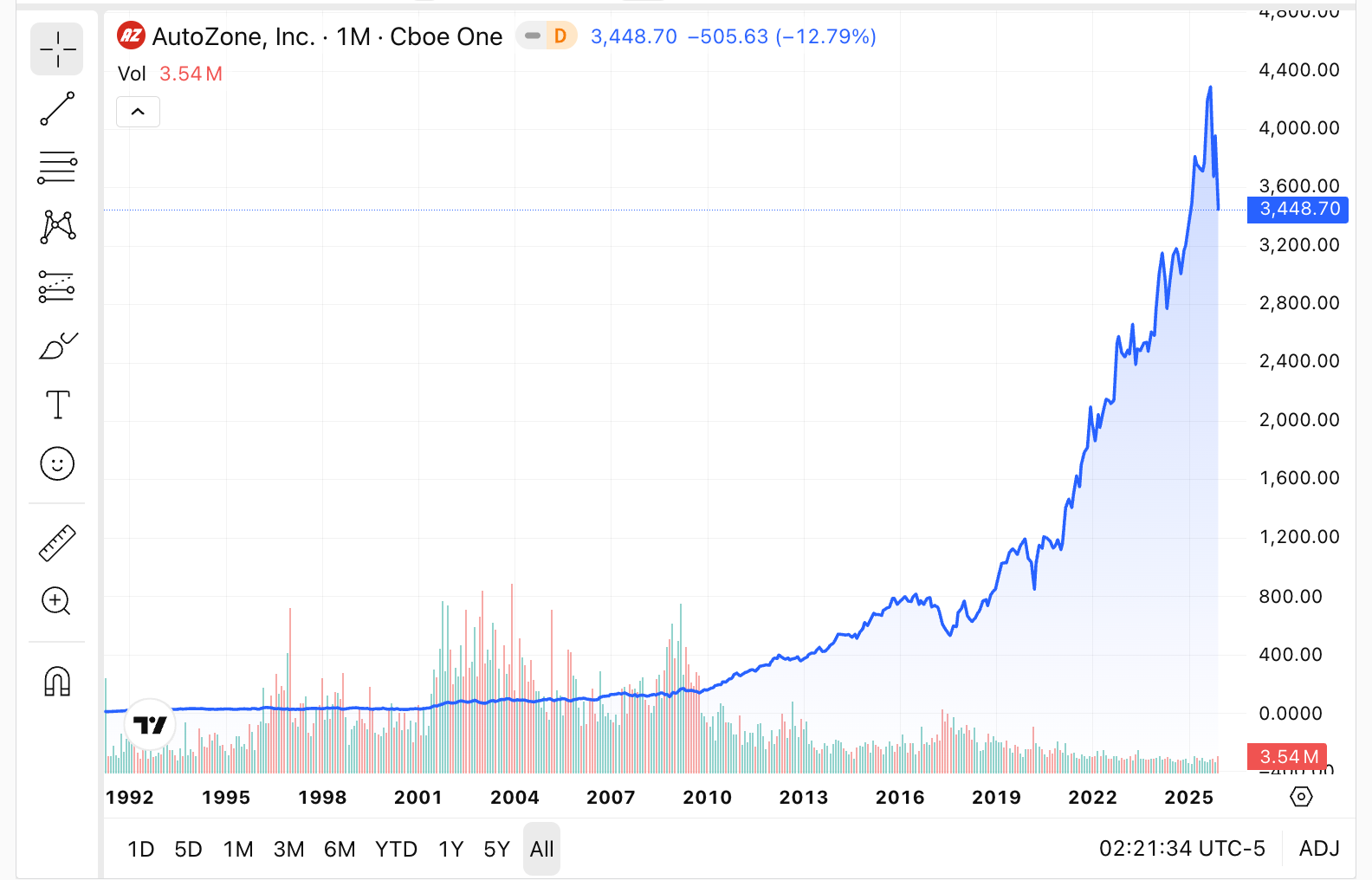

AutoZone reduced its share count by nearly 90%. Net income went up about 10x. EPS went up about 90x. Still think this is a boring company?AutoZone sells car parts and looks boring. That’s the point.

Inventory turns are low by design. Gross margins are high because service is baked into the sale. Working capital is negative because suppliers fund the model. And every excess dollar gets turned into buybacks.

AutoZone is a buyback machine disguised as a parts store. That mix is rare. And it is deadly.