Cardlytics (CDLX): The Silence of the Lambs

"In particular, if you have a corporation where a man has risen to be CEO, and he now has hundreds of millions of dollars in the stock of the company... And then he has his directors vote him a great stock option grant annually to preserve his loyalty and his enthusiasm to the company, I think that's demented. And I also think it's immoral."

- Charlie Munger

I made a mistake.

Cardlytics was my investment before Cannibal Stocks existed. The ticker is CDLX. Most people reading this have never heard of it, and that is the first interesting thing about this company. You have probably used it. You just did not know.

Here is the business in four sentences. You open your banking app and see an offer, twenty percent back at a restaurant you already visit. You tap it, you pay with your card, the cashback lands automatically. Behind that tap sits Cardlytics, the wire connecting the advertiser to your bank, and the bank already knows what you buy. They do not advertise themselves. They have no logo you would recognize. They are already built into the payment systems of some of the largest banks in America, which means millions of people use this company every week and have no idea it exists.

When I bought it, here was my logic, and I want to be honest about every piece of it.

I thought the moat was enormous. Banks will not hand customer transaction data to anyone. Google tried. Facebook tried. Both got told no. Cardlytics got in because the data never leaves the bank. A competitor starting today would have to go bank by bank, contract by contract, for years. That felt unbreakable to me.

The stock was cheap. All-time low cheap. I was buying the whole company for under one times revenue. The math in my head was simple and seductive. The cost base is fixed, somewhere around 250 to 300 million a year, whether revenue is 250 million or a billion. So the moment they become meaningfully profitable, and they are already around breakeven, the market hands a small-cap a high multiple overnight, and you are sitting on a brutal return. That was the entire thesis. And I was buying while everyone else was running for the exits. I cloned the idea from Cliff Sosin, and I was paying less than he did. What could go wrong.

Here is what I got wrong.

It turns out the banks can do this themselves. I do not regret that part. If you do your homework, you think hard, you read everything, and you still get the moat wrong, that happens. It happens to the best investors alive. I am young. I will misjudge a moat again. That is the cost of doing this work, and I am at peace with it.

While I was sitting in this position, watching the stock grind lower, I noticed something else. Something that had nothing to do with banks or moats or competition. Every single quarter, no matter how badly the company performed, no matter how far the stock fell, management got rewarded. More shares. More grants. Again. And again. And again.

So I asked people. Smarter people than me, more experienced people, people who have been doing this longer. I asked them, is this normal? Is this how it is supposed to work? Every one of them told me the same thing. Yes. That is standard. That is just how the industry does it. Stock-based compensation, equity grants, it is normal, do not worry about it.

Bullshit.

What I Found Underneath

Quick thing first, because the whole post rests on it. A company is a pie. Your shares are your slices. When the company prints new shares for someone else, your slices do not disappear, but the pie now has more slices in it. Your piece got smaller. That is dilution. Nobody reaches into your pocket. You just own less of the same company than you did yesterday.

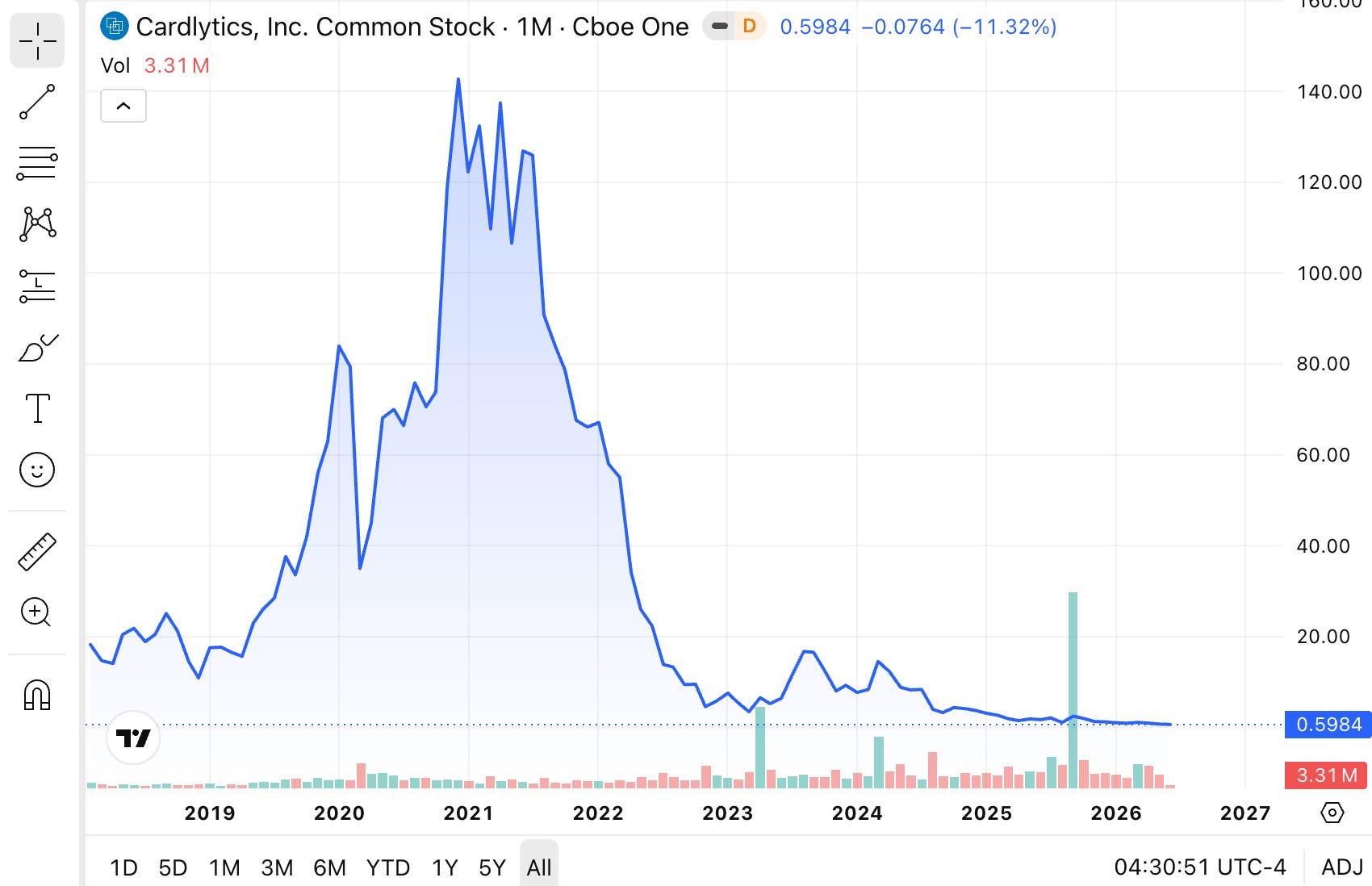

Now look. In 2018 Cardlytics had about 22 million shares. Today it has about 58 million. They more than doubled the slices. And while they kept printing, the stock fell from about 150 dollars to under one. Price down 99 percent. Slices up 156 percent.

What does that do to you? If you owned one percent in 2018, you own about 0.39 percent today. You sold nothing. Your piece got cut by more than half while you watched.

So where did all these shares go?

A big chunk went to pay the people running the company. From 2018 to 2024, Cardlytics handed out about 251 million dollars worth of stock as pay. The entire company today is worth about 50 million. They paid out five times the value of the whole business in stock. Not with money they earned. With your ownership.

Then the deals. In 2021 they bought two companies for about 856 million combined. Within three years they admitted those companies were nearly worthless and wrote off more than 655 million of it. Hundreds of millions gone, and more shares printed to pay for it.

But the part that got under my skin was the accounting.

Cardlytics reports a number called Adjusted EBITDA. In 2024 the real result was a 189 million dollar loss. Their homemade number was a 2.5 million profit.

How do you flip a 189 million dollar loss into a profit? You take the bad stuff out. Mostly the 40 million in stock they paid themselves. They erase the cost of their own pay, then call the business profitable. Their excuse? Stock is “non-cash.” No money left the building, so it does not count.

That is the trick. If you would feel richer getting salary plus stock than salary alone, then the stock is pay. And pay is a cost. You do not get to call it free just because no cash moved. Somebody paid. You paid, through dilution. Munger had a word for this kind of accounting. Corrupt.

Then the detail that ended my doubt. On January 12, 2026, with the stock around 90 cents, after the collapse, after everything, the company handed a new executive one million fresh shares. They printed more.

Why would anyone be comfortable doing that? Buffett answered it in 1995.

“We have had conversations with managers where they tell us how fortunate they feel because the stock is down and they can issue options cheaper. If they were issuing those to the third parties, I’m not sure whether they’d have exactly the same attitude.”

There it is. A low price is a disaster for you. For a manager paying himself in shares, it is just a cheaper way in. The lower it falls, the more shares it takes to hit the same payday, and the more of your company quietly changes hands. Munger said it plainer, about a manager who thinks printing shares costs nothing:

“Imagine hiring a manager who thinks that way and paying them money to behave like Judas in your very midst.”

I got the moat wrong. I can live with that. But the moat could never have taught me this. The price tells you what the market thinks of the company.

The share count tells you what management thinks of you.

The Silence of the Lambs

There is a reason for the title.

The shareholders of Cardlytics did what shareholders are trained to do. They held. They trusted. They waited for the next quarter. And every quarter, more shares were printed and handed to the people at the top. They did not scream. They stood quietly in line while their piece got smaller, and smaller, and smaller.

That is what most of us are. Lambs. And the silence is mistaken for consent.

I was one of them.

Not anymore.

Today I put on the mask.

Cheers, Sandro

Note: After years of dilution, the final act was a reverse split. On June 3, 2026, Cardlytics announced a 1-for-10 reverse split, which will begin trading on a split-adjusted basis on June 8. The main reason is to push the share price higher and remain compliant with Nasdaq listing requirements. It improves the stock's appearance, but it does not improve the underlying business. It simply buys more time.

A reverse split is financial cosmetics. It makes the stock price look higher, which can attract buyers who focus on the price rather than the business itself.

Decades ago, Stock-Based Compensation (SBC) was kept entirely off the Income Statement until Warren Buffett famously called out the absurdity, forcing regulators to mandate its inclusion on the P&L. Having lost that battle under GAAP, Big Tech management adapted by shifting the narrative to a non-GAAP metric: Free Cash Flow (FCF). By relying on standard definitions that automatically add SBC back to Operating Cash Flow, they have effectively resurrected the old illusion.

Given the staggering magnitude of equity grants handed to Big Tech insiders today, ignoring SBC in FCF calculations is not a benign accounting quirk—it is a structural distortion. Excluding a massive, recurring operational cost from cash flow metrics represents a deliberate attempt by management to obfuscate economic reality from the true owners of the business. It is a fundamental governance red flag. At Berkshire Hathaway, where cash compensation is the standard, such accounting games are non-existent; if Berkshire ever utilized equity incentives, management would display the candor to account for them transparently.

The structural hypocrisy deepens when evaluating capital allocation. Management frequently deploys billions in hard cash to repurchase shares—often at or above intrinsic value—for the sole purpose of neutralizing the dilution caused by these very same equity grants. Masking an escalating share count by burning cash on non-accretive buybacks is a egregious transfer of value from external shareholders to insiders.

In a buoyant market driven by promotional narratives and momentum-driven participants, these structural flaws are easily ignored. The prevailing consensus treats both SBC and structural CapEx as flexible variables that can be adjusted away to justify higher valuations. Investors who accept these inflated, management-adjusted figures without haircutting the cash flows or modeling the inevitable dilution are simply deluding themselves.

Rant ends.