Everyone’s Buying AI Stocks. I Remember 1999.

Beware the next big trend

“What we learn from history is that people don’t learn from history.” — Warren Buffett

I’m not against AI. On the contrary — I’m fascinated by what’s happening right now. This revolution is real, and I feel privileged to live in a time when the entire world is changing before our eyes. I truly believe artificial intelligence will make the world a better place.

AI will eliminate many jobs that people were never meant to do — truck drivers who sleep and live in their cabins, shower at gas stations, spend months away from their families, and eat on the highways. Warehouse workers who stand for 12 hours counting other people’s packages. Call-center agents who repeat the same sentences all day long. People who copy data from one spreadsheet to another, without meaning or purpose.

AI will change all of that. And that’s a wonderful thing.

But my job as an investor, managing both my own and other people’s money, is to assess risk. And I see many risks along the way. Don’t get me wrong, of course it’s possible to make money on AI stocks. But my small brain simply can’t figure out who the ultimate winner will be, or whether this will turn out to be a “winner-takes-all” game. These companies are capital-intensive and highly risky.

And I don’t like either capital-intensive or risky businesses. It’s that simple.

So let’s look back at what history teaches us about big trends.

Beware the next big trend

“There is no better teacher than history in determining the future.” — Charlie Munger

Rising stock prices are far more common than they might appear at first glance. These explosions in value don’t just happen on Wall Street, they happen everywhere, across different industries and parts of the world, both in history and today.

If you look closely, there’s always some “new big thing” growing somewhere, a startup, an industry, or even an entire nation on the rise. Former CNBC journalist Ron Insana wrote about this in his book “Trend Watching.” A quick look at it reveals one clear truth: these sudden booms are a permanent feature of markets. Something is always rising, it’s either just beginning, at full speed, or on its way to collapse.

These market swings are usually driven by human nature, as fear and greed are the two main engines. As long as there are people investing, there will be these ups and downs. One day, everyone’s buying because they don’t want to miss “the big opportunity”; the next, they’re all selling because they’re terrified of losing money. That will never change, it’s simply part of the game.

To illustrate why this matters, let’s take a quick look back.

The Automobile Boom: The First Big Trend

In the early 1920s, the American automobile industry was booming. If you were an investor at that time, you probably thought cars were the future and you would’ve been right. In just one year, between 1921 and 1922, car sales jumped an incredible 50%. America was in the middle of an industrial revolution, roads were being built, cars were becoming affordable, everything pointed to an unstoppable trend.

It all looked perfect.

But soon after, the market collapsed, and most of those car companies vanished. If you were an investor then, you would have lost nearly everything, even though you were absolutely right that cars would change the world. Only the biggest players survived; everyone else disappeared. Between 1895 and 1930, around 1,900 automobile companies were founded in the United States. By the mid-20th century, more than 99% of them were gone. The few that survived were Ford, General Motors, and Chrysler, along with a handful of smaller names like Hudson, Nash, Packard, and Studebaker — most of which eventually disappeared too.

The Electronics Craze: The Second Wave

If you were an investor in the 1950s, you probably thought electronics were the future — and you would’ve been right. Semiconductors, transistors, and solid-state circuits were revolutionary technologies that changed everything. Radios, televisions, and early computers all depended on them. It felt like a once-in-a-century opportunity.

But just like the automobile boom decades earlier, the story ended the same way. Investors piled into hundreds of companies with futuristic names ending in -tron or -onics, expecting limitless growth. Between 1950 and 1965, over 140 U.S. electronics firms went public — and within two decades, more than 90% of them had disappeared or been absorbed.

Only a handful survived and became true industry foundations — names like Fairchild Semiconductor, Texas Instruments, and Sperry Corporation. The rest vanished almost as quickly as they appeared.

The technology was right. The investments weren’t.

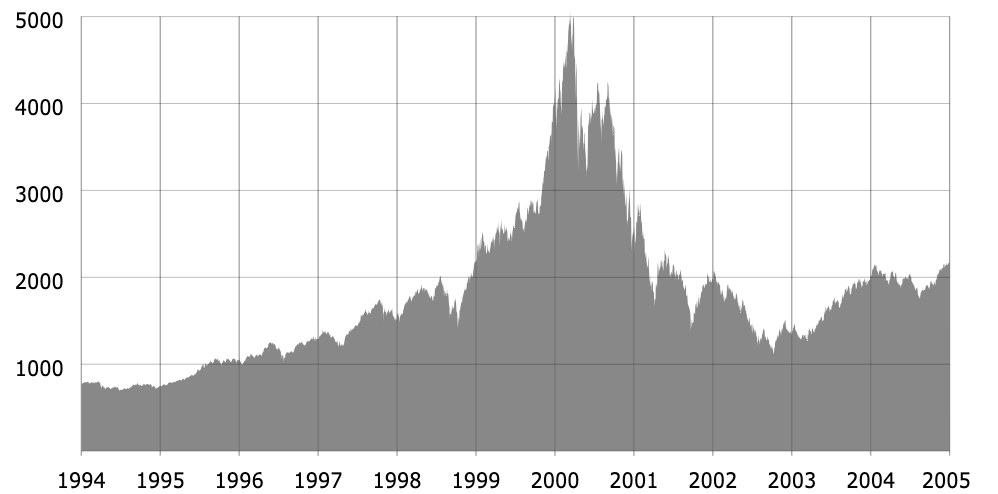

The Dot-Com Mania: The Internet Revolution

If you were investing in the late 1990s, you were sure the internet would change everything — and you were right. But the market went berserk. From 1999–2001, hundreds of “.com” IPOs hit the tape and by 2000–2001 alone, at least 762 internet firms shut down (225 in 2000, 537 in 2001).

By 2002, the Nasdaq had fallen nearly 80%, erasing trillions in market value. Most of those once-hyped startups vanished — names like Boo.com, Pets.com, and Webvan became symbols of the crash.

History Repeats in Cycles

So, what do all these stories have in common? Each of these wild market cycles happens roughly every 30 to 50 years. Why that long? Because it takes about that much time for a new generation of investors to forget the lessons of the last crash. Those who lived through the pain usually step aside before the next “big wave,” and the newcomers convince themselves that this time will be different.

But history always reminds us that things never turn out the way everyone expects.

There’s something else these eras share: during every boom, hundreds or thousands of companies emerge from nothing. First it was car manufacturers, then semiconductor and electronics firms, and later, tech startups in the 2000s.

The problem? Many had little to no revenue, no profits, and rising debt. Stock prices soared without any foundation. Everyone thought the growth would last forever. People even sold quality stocks like Berkshire Hathaway just to join the party. Why? Because no one could stand watching their neighbor get rich faster.

“Someone will always be getting richer faster than you, this is not a tragedy“ - Charlie Munger

Is Today’s AI Boom the New Dot-Com Bubble?

We’re witnessing a new wave and that wave is artificial intelligence.

But serious investors should ask one simple question: are AI stocks overvalued?

The short answer — partly, yes.

Valuations are undeniably high, though this isn’t exactly 1999. The S&P 500 trades at a P/E of around 27-28 — well above its historical average of roughly 16 and the CAPE ratio is near 40 — the third-highest level in history. That tells us prices, especially in tech, are far above long-term averages.

Large institutional managers are increasingly cautious, not because the companies are bad, but because expectations are already extreme. Still, market behavior doesn’t yet resemble the chaos of the dot-com era. The IPO market is active, but we don’t see millions of new retail traders rushing in “because everyone else is.” The excitement is real, but not manic.

I personally don’t invest directly in AI stocks. The reason is simple: the first phase of any technological revolution is the most dangerous one. Vanguard’s Joe Davis explains that every major innovation goes through two phases. The first is marked by hype, heavy investment, and often a bubble. The second comes later, when the real winners emerge, not the companies building the technology, but those using it most effectively. Think of Ford and GM during electrification, or Amazon during the internet era.

That’s why I believe most of today’s “AI pure plays” won’t be the final winners. Most of the growth story is already priced in. AI is fully embedded in the valuations of Nvidia, Meta, and Microsoft. Even if the most optimistic forecasts turn out true, the market has already priced in much of that success. Limited upside — high downside if expectations disappoint.

When I invest, I always ask two simple questions: how much am I paying, and when do I get my money back? If that timeline is two, three, or five years — I’m interested.

But if Nvidia trades at a $4.5 trillion valuation, I have to ask: can Nvidia generate $1 trillion in free cash flow next year?

If the answer is no, I move on. It’s that simple — I’m just not interested.

The real winners, in my view, will come from elsewhere — the so-called “boring” sectors: manufacturing, logistics, healthcare, finance. Those are the places where AI can cut costs, boost productivity, and quietly transform margins. Over time, value stocks might outperform the flashy tech names once the excitement fades.

For now, AI stocks are more story than math. Most valuations depend on distant revenue projections that are little more than educated guesses. It’s the same mistake investors made in the dot-com era, being right about the technology, but wrong about the price.

AI is the future, no doubt about it.

But not every AI stock is a good investment. The smart money waits for the second phase, when the hype fades, and the real value emerges.

Stay rational, stay patient — history rewards those who do.

Cheers,

Sandro,