How Buffett Really Got Rich: Inside His First Investments

Part 1: Marshall-Wells

“He’d find something that was selling for one-fourth of liquidating value. He’d load up. So for a long period of time, he had a happy hunting ground. All he had to do was go through lists of liquid securities and slowly buy them, and he could get these ridiculous bargains.”

Charlie Munger

In 1950, while studying at Columbia, twenty-year-old Warren Buffett discovered that he could buy shares of real businesses for less than what their assets were worth if sold off.

This post is part of a new series where we’ll step inside Warren Buffett’s mind — to see how he invested small sums of money at the very start of his career. We’ll look at his biggest wins, his mistakes, and the lessons that shaped the greatest investor of all time. Honestly, I think dissecting Buffett’s investments and trying to understand how he thinks teaches you far more than any Harvard Business School degree ever could.

Back then, Buffett owned a few stocks, a few books, and a very patient mind. His mental model of investing was simple: he looked for stocks that made absolutely no sense. But he had already understood one of the greatest truths about investing — in the stock market, you’ll occasionally find things that make absolutely no sense.

If you try to buy a house and ask the seller for the price every day, it will barely change — rational buyer, rational seller. But pick any stock and look at its 52-week price range, and you’ll often see swings of 100% or more. That’s the beauty of the stock market.

Sometimes you’ll find a company sitting on massive oil reserves, capable of generating $100 billion in future free cash flow and yet the entire business trades for just $1 billion. And other times, you’ll see a tech stock trading at 600 times annual earnings. Madness on both sides.

Back then, Buffett was buying businesses below their liquidation value — meaning he could shut them down, sell all assets, and still make more than what he paid in the market. It was simple, rational, and brutally effective. He also had one huge advantage that he doesn’t have today — he was investing small sums of money. Today, he can’t buy a company worth only a few million in market cap; it simply wouldn’t move the “needle” for Berkshire.

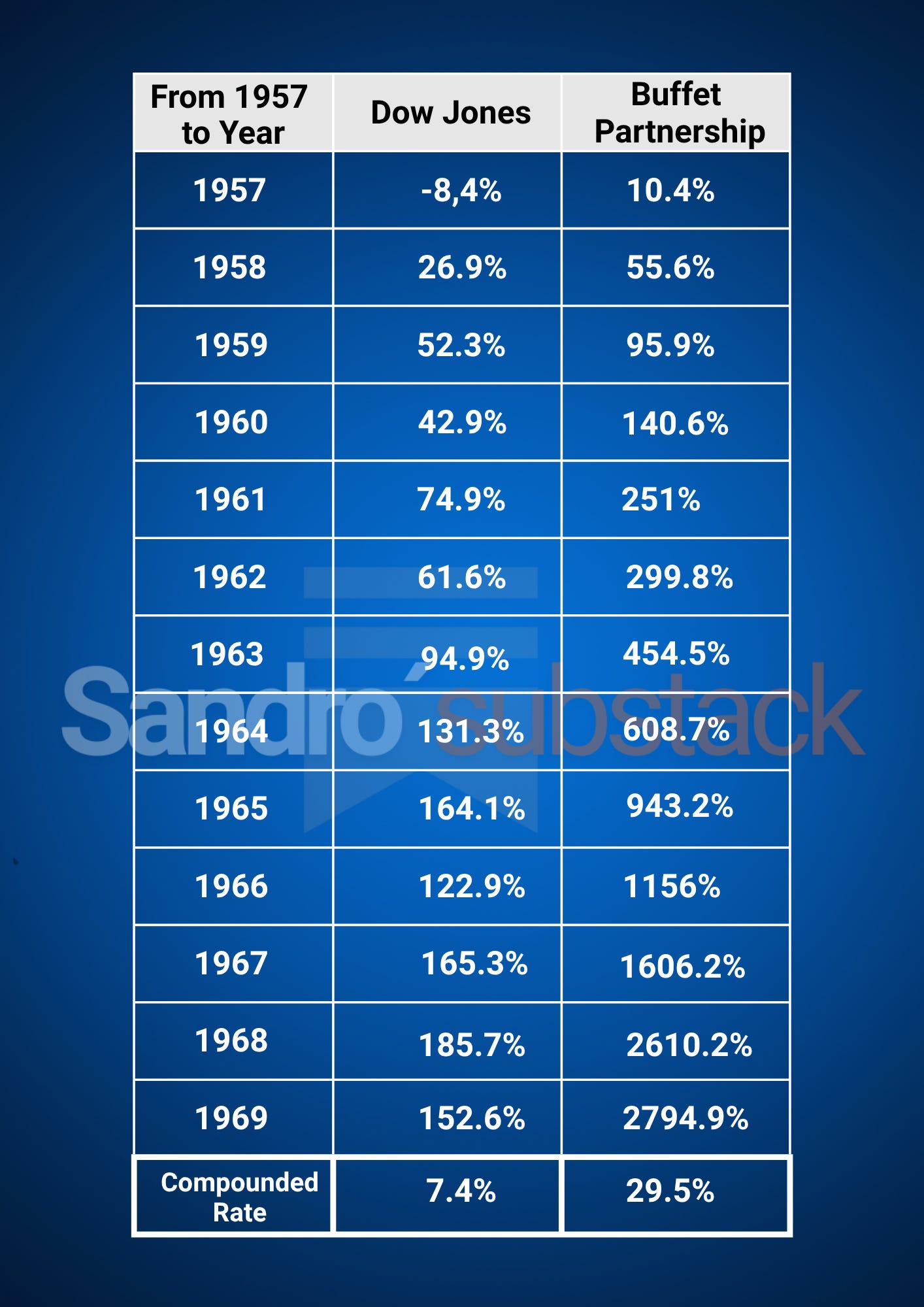

Between 1957 and 1969, his partnerships compounded at 29.5% per year, turning $1,000 into nearly $26,000, while the Dow Jones barely moved. Buffett wasn’t just beating the market — he was obliterating it.

So how did he do it? He wasn’t diversified. When he found a great idea, he went almost all in. He pushed management to unlock value by returning capital to shareholders, travelled to factories, met owners, and studied businesses up close. Even though he made mistakes, it was already clear this was a rare talent worth watching. He wasn’t born a genius — he became one through relentless work, failure, and an obsession with learning.

The early portfolio

In this series, we’ll go step by step through Buffett’s early investments:

Marshall-Wells (1950)

Greif Bros. Cooperage Corporation (1951)

Cleveland Worsted Mills (1952)

Union Street Railway (1954)

Philadelphia and Reading (1954)

British Columbia Power (1962)

American Express (1964)

Studebaker (1965)

Hochschild, Kohn & Co. (1966)

Walt Disney Productions (1966)

This post focuses on the very first one — Marshall-Wells, a company Buffett invested in before his partnership years began. So what did Buffett see in Marshall-Wells?

Marshall-Wells: Buffett’s first investment

In 1950, a twenty-year-old Warren Buffett, a student at Columbia under Ben Graham and David Dodd, bought 25 shares of Marshall-Wells, then the largest hardware wholesaler in North America. The stock was extremely cheap, trading below its net current asset value — a textbook deep-value case straight from Graham’s playbook. At the time, Marshall-Wells sold tools, electrical appliances, paints, and sporting goods across the northwestern United States, Alaska, and the western provinces of Canada. Revenues were evenly split: 50% U.S. and 50% Canada.

Buffett purchased the shares at $200 each, a total of $5,000, of which his personal contribution was $2,500 — roughly a quarter of his net worth at the time. The company had a market capitalization of $11.4 million, and after subtracting cash and government securities, an enterprise value of only $7 million.

It ticked every box in Graham’s playbook — cheap, boring, and slightly dusty. The kind of company that would never trend on X. 😅

Key figures:

traded 40% below net current asset value (NCAV)

EV/EBIT = 1.9x

P/E = 5.5x

cash and bonds = 20% of total assets

current assets = 82%

inventories = 43%

The net current asset value per share was $331, while Buffett paid only $200 — about 66% below intrinsic value. It was a classic “cigar-butt” investment — a stock so cheap that the downside appeared minimal compared to the potential upside. However, the industry was entering a post-war saturation phase as growth was slowing, and profitability was falling. Buffett became disillusioned with the management, which he viewed as passive and indifferent toward shareholders, and soon sold his shares.

Despite the solid numbers, Buffett exited the position later that same year with a minor 1% loss — likely balanced out by the $12-per-share dividend. In short, it was basically a wash.

In the following years, Marshall-Wells struggled as post-war demand faded and competition intensified. Profit margins declined, the company lost relevance, and by the late 1950s it was liquidated and sold off in pieces.

The Marshall-Wells investment didn’t work out as he expected, but he didn’t lose any money on it either. His main takeaway here was the importance of management — specifically, whether they’re willing to allocate capital for the benefit of shareholders.

Today, if you look at his portfolio — Apple, Coca-Cola, American Express — they all share one thing in common: they’re excellent businesses that allocate a portion of their capital for the benefit of shareholders.

Similarly, the three companies that make up 100% of my portfolio are also excellent businesses — and they have something that’s become quite rare today: they plan to return 100% of their free cash flow to shareholders, mostly through buybacks and we might see some nice returns from them in the future.

…at this point, I’m not even an investor — I’m just getting paid to do nothing 😎

Next up: Greif Bros. Cooperage Corporation (1951) — where Buffett’s evolution truly began.

Cheers, Sandro