How Much is Transocean (RIG) Really Worth

Price is what you pay, value is what you get

“There are five ascending levels of intellect: Smart, Intelligent, Brilliant, Genius, Simple.” - Albert Einstein

According to Einstein, the highest level of intellect is simplicity. And I’ve always felt that simplicity is a huge advantage because we can always have things straight in our head. So I’ve always been naturally attracted to simplicity.

I’ve also felt that when I’m making an investment, if I cannot explain the thesis of that investment in three sentences to a child, there’s something wrong with the investment. It’s probably not going to work. Here’s how I explained my offshore thesis to my child:

Offshore oil supplies a huge share of global production, and it’s produced at a much lower cost than fracking. Drillships are massive, extremely expensive machines and no new ones are being built. When the number of ships is limited but projects keep growing, dayrates usually rise, and that’s when companies like Transocean can make a lot of money.

I like offshore bets because they’re simple. You check how much stuff the company owns, how much money it owes, and how much its rigs can earn in the next years. When you put that together, you get a simple idea of what the company is really worth. That’s exactly what we’re going to do here.

Investment thesis:

Transocean’s downside is heavily anchored by its hard assets at today’s price, while the upside has no practical ceiling if the cycle stays tight.Here’s the structure for the rest of the write-up:

Liquidation value (today)

• Balance-sheet value per share

• Fleet value per share

Intrinsic value (2026–2032)

• Expected free-cash-flow generation over the next cycle

• Capital Allocation

We’ll finish with some key risks and a comparison between Valaris and Transocean.

Liquidation value (today)

Balance-sheet value per share

A quick note: I don’t include Transocean’s backlog in the liquidation value. Valaris has a short, near-term backlog that turns into cash soon, so it makes sense to treat it like cash in liquidation. Transocean’s contracts run much longer, so using backlog the same way wouldn’t be accurate.

In its latest 10-Q, Transocean reports the following non-fleet assets:

Cash and cash equivalents: 833M

Restricted cash: 417M

Accounts receivable: 574M

Materials and supplies: 382M

Assets held for sale: 48M

Other current assets: 163M

Other assets: 974M — in liquidation I take 50% = 487M

Deferred tax assets: 95M — I assume 0 in liquidation

Total non-fleet assets add up to roughly 2.9 billion dollars. With about 1.10 billion shares outstanding, that’s around 2.6 dollars per share in non-fleet value before even considering the rigs.

Fleet value per share

Transocean’s fleet is a completely different animal from Valaris.

Valaris has a strong fleet, but a big part of it consists of jackups for shallow waters. Transocean has none of those. Its entire business is built around the deepest water and the harshest conditions on Earth.

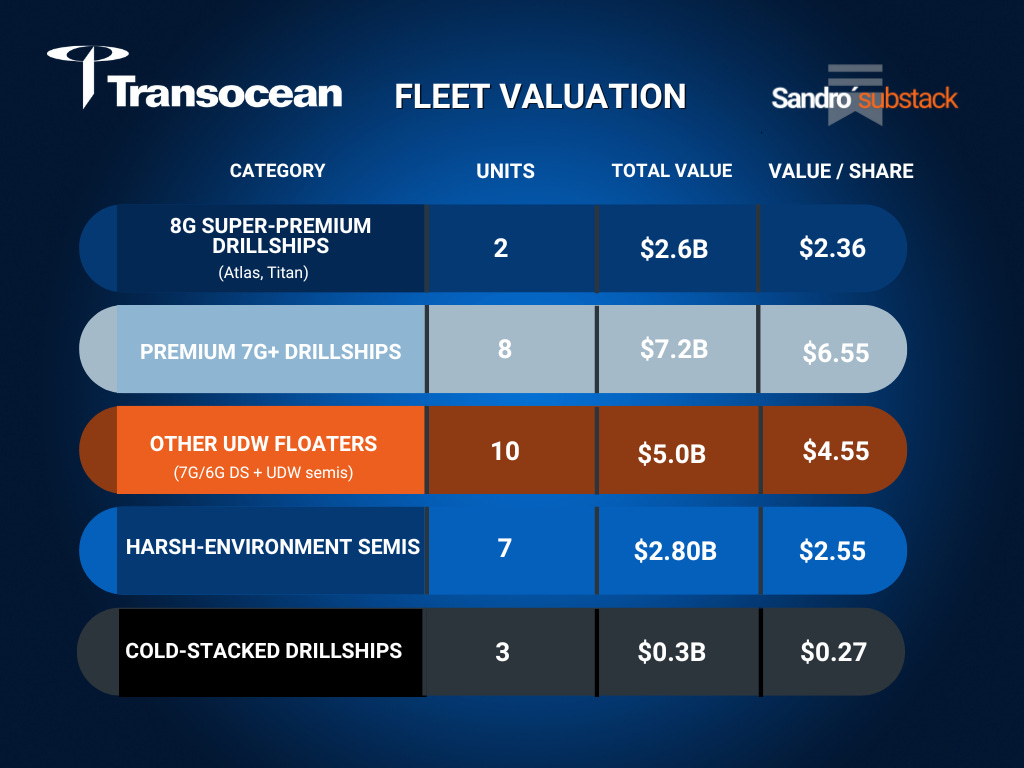

Transocean owns two 8th-generation drillships, the most capable ever built. Right below them are the upgraded 7th-generation units, which now sit so close to 8th-gen specs that in practice they can handle nearly the same ultra-deep, high-pressure, long-duration wells.

Then you have the harsh-environment semis. These are the rigs built for the worst conditions on the planet: freezing temperatures, storms, massive waves and unpredictable seas — the North Sea, the Arctic edges. Only a handful of rigs worldwide can operate safely there, and Transocean owns many of the very best. That is a real moat. When oil companies push into the deepest wells and the harshest environments on Earth, Transocean is almost without competition.

Since the goal here is to estimate liquidation value today, I’m keeping the assumptions intentionally conservative. Some analysts argue that Transocean’s fleet could be worth close to 40 billion dollars in a fully tight market. I don’t think that number is unrealistic long term, just not today. It only becomes plausible if the ultra-deepwater market tightens exactly the way I expect over the next few years.

Sixth-generation harsh-environment rigs like the Enabler and Barents are now earning around 480k per day, a level that until recently belonged only to top-tier seventh-generation units. That means a 6th-generation rig can already generate close to 100 million dollars of free cash flow per year, which is phenomenal. That alone suggests the entire fleet is structurally more valuable than what I’m assuming here.

As for the stacked fleet, Transocean has only a small group of rigs worth considering. In reality, just three have meaningful reactivation potential: Apollo, Athena and Mylos. The rest are impaired or held for sale — outdated units that would require enormous capex and can’t earn real market rates. In practice they’re scrap or spare-parts value, so I exclude them entirely from the fleet valuation.

I estimate that the entire fleet is worth around 18 billion dollars today, or roughly 16.3 dollars per share. Add roughly $2.6 per share in non-fleet assets, and the current liquidation value comes to around $19 per share.

In summary:

Fleet value: $16.3 per share

Non-fleet assets: $2.6 per share

Total assets before debt: $19 per share

On the liability side, Transocean has about 8.1 billion dollars of total liabilities, including roughly 6.2 billion of interest-bearing debt. The remaining non-debt items are broadly matched by the current asset block we already covered.

So in this liquidation lens, I subtract only the net debt from the asset value, around $5.7 per share. After that adjustment, the conservative liquidation value comes out to roughly $13.3 per share.

Transocean stock trades at about $4 per share — before we even touch the intrinsic value.