Whitehaven Could 10x. Here's Why I'm Not Buying It.

Whitehaven Coal is sitting on a $17 billion cash machine. One decision separates a 10-bagger from a dead-money dividend trap.

The Department of Energy recommended the addition of metallurgical coal and uranium, citing the use of these minerals in domestic steel production and projections for steel production to grow.

The United States government has officially recognized that metallurgical coal has no substitute. There is no green alternative. No synthetic replacement. No workaround. You cannot make steel without it. And by classifying it as a critical mineral, the US has given itself the legal and strategic framework to restrict or ban met coal exports in the event of a supply disruption. Think about what that means. The same way politicians today talk about banning oil exports to protect domestic energy security, the US can now do the exact same thing with met coal. And if that ever happens, if the world’s second largest met coal exporter pulls supply from the seaborne market, prices would explode. Every tonne of met coal shipped from Australia, Canada or Russia would instantly reprice. It is now an official policy option. And it changes the entire calculus for anyone investing in seaborne met coal.

The met coal macro no one is talking about

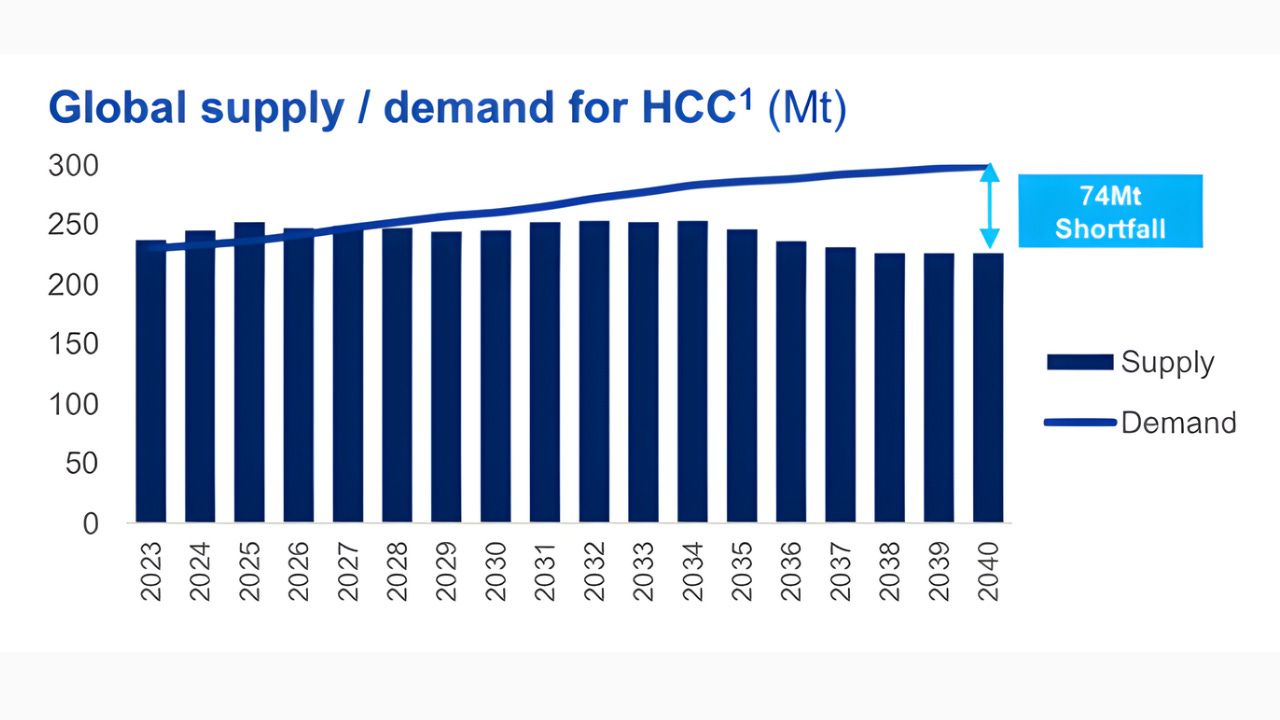

For the past decade, China dictated met coal prices. It had Russia and Mongolia next door. Whenever it needed more coking coal, it simply stepped onto the seaborne market. That single buyer was enough to keep premium hard coking coal averaging around $250 per tonne for five years straight.

Now forget China. Look at India.

India’s steel production surged 10 percent year on year to over 150 million tonnes in 2025. The government is targeting 300 million tonnes by 2030. And 500 million by 2047. But here is what matters: India has no Mongolia next door. No Russia. Every single extra tonne of steel requires coking coal that must arrive by ship. India is about to overtake China as the world’s largest seaborne buyer of met coal. By 2028 at the latest, the seaborne met coal market will be structurally short. And there are no meaningful new supply sources coming. Australia is the anchor supplier. The US, Canada, and Russia fill the gaps. That is it.

I wrote about the met coal industry in this post.

That is the macro backdrop. Now let me show you what Whitehaven Coal looks like through that lens.

A monster hiding in plain sight

Whitehaven Coal is a textbook Cannibal Stocks setup. Unknown to most investors. Deeply undervalued. Operating in an industry everyone loves to hate. Exactly the kind of stock I look for.

Let me walk you through what this company has already proven it can do.

On a USD EBITDA basis, Whitehaven generated roughly $2.6 billion in 2023, $2.0 billion in 2022, $0.6 billion in 2024, and $1.4 billion in 2025. Read those numbers again. This is a company with a market cap that barely reflects a single good year of cash flow.

But that was the old Whitehaven. Smaller. Primarily a thermal coal producer. Narrower asset base, less diversification.

Then everything changed. Whitehaven acquired two major metallurgical coal mines from BHP. Blackwater is a large-scale, long-life mine with massive reserves and strong infrastructure. Daunia adds high-quality met coal exposure with established production and export capacity. Together, these acquisitions transformed Whitehaven from a mid-tier thermal coal miner into one of the most powerful diversified coal producers on the planet.

The one thing management must get right

Share repurchases can be the smartest thing a company ever does — or the dumbest.

Warren Buffett, 1999 Meeting

I get it. Some investors love the dopamine hit of a dividend landing in their account. But here is the truth: dividends are the last resort of capital allocation. You pay a dividend when your stock is trading at nosebleed valuations and buybacks no longer make sense. That is the only time.

Here is the simple math. Whitehaven could realistically generate $1 billion, $2 billion, or even $3 billion of free cash flow in a single year depending on coal prices. Management plans to return around 50 percent to shareholders. They have already launched an A$72 million buyback program.

That is a start. But it is small. Far too small.

What Whitehaven should be doing is killing the dividend entirely. Every single dollar should go into buybacks while the stock trades at these levels. This is a once-in-a-decade window.

So I built the model myself. And the difference between the two paths is not small. It is staggering.