Inside Buffett’s First Investments: Greif Bros. Cooperage Corporation (1951)

Buffett’s $3,650 bet

This post is part of a new series that steps inside Warren Buffett’s mind — exploring how he invested small sums of money at the very start of his career. We’ll look at his biggest wins, his missteps, and the timeless lessons that shaped the greatest investor of all time. To be honest, studying Buffett’s early moves and the way he thought teaches us far more about real investing than any Harvard Business School degree ever could. In those early years, Buffett was buying businesses below their liquidation value — meaning he could close them, sell the assets, and still walk away with a profit.

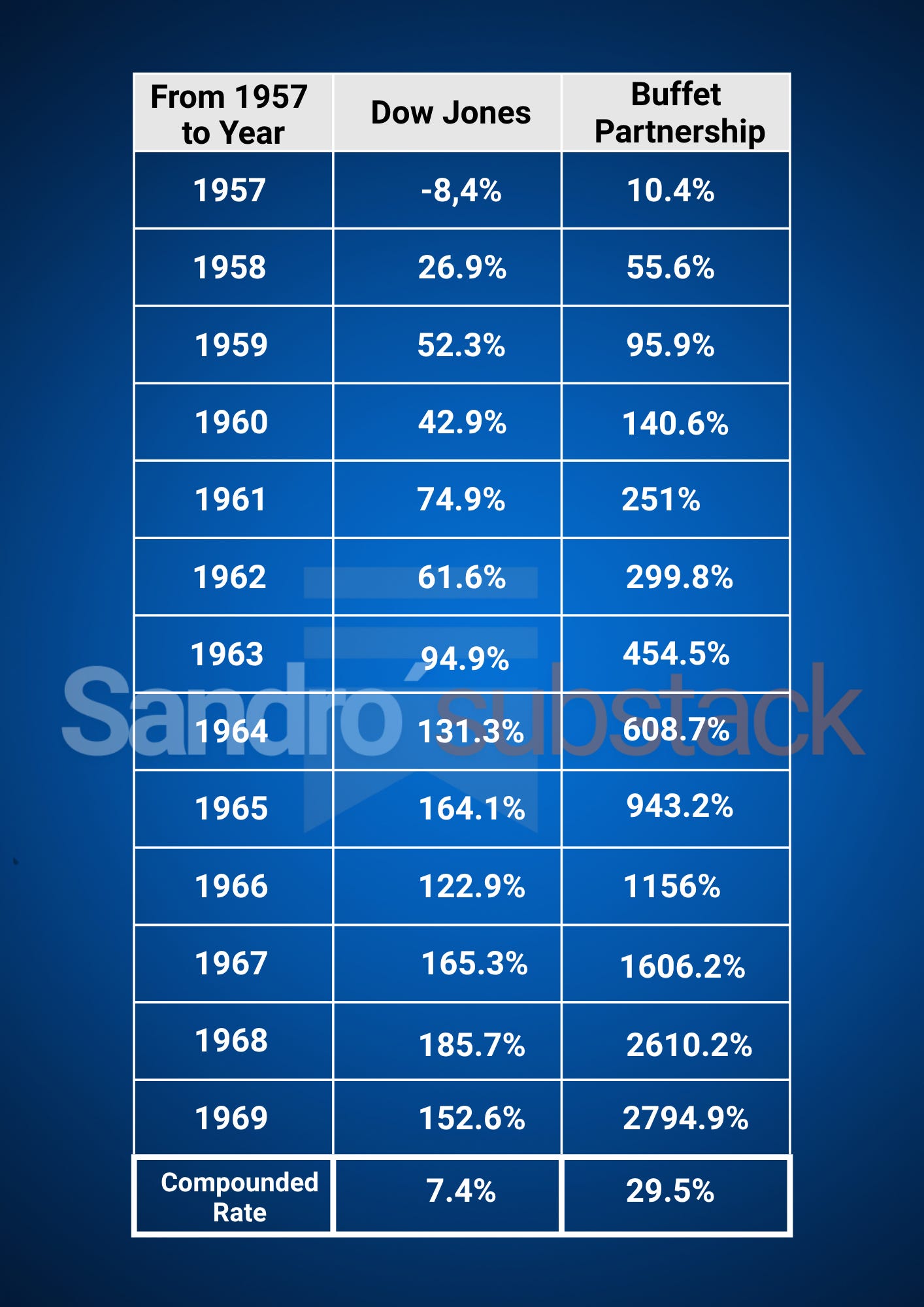

From 1957 to 1969, Buffett’s partnerships compounded at 29.5% per year, turning $1,000 into nearly $26,000, while the Dow Jones barely moved.

The early portfolio

Marshall-Wells (1950)

Greif Bros. Cooperage Corporation (1951)

Cleveland Worsted Mills (1952)

Union Street Railway (1954)

Philadelphia and Reading (1954)

British Columbia Power (1962)

American Express (1964)

Studebaker (1965)

Hochschild, Kohn & Co. (1966)

Walt Disney Productions (1966)

My previous post on Marshall-Wells (1950) can be found here:

This post focuses on Greif Bros. Cooperage Corporation (1951) — a company that manufactured wooden barrels, kegs, and staves used to store and transport dry goods like sugar, flour, fruit, and nails. In the early 1900s, it was the largest cooperage company in the world, supplying packaging for industries from food to petroleum.

Greif Bros. Cooperage Corporation

Something new began with this one.

In 1951, Warren Buffett was a 21-year-old student driving across the country, personally visiting companies he was considering investing in. No assistants, no prior meetings — he’d simply walk in and talk to whoever was willing to talk with him.

During that trip, he stopped in Ohio, to investigate Greif Bros. Cooperage Corporation, the world’s largest barrel manufacturer. What began as a quick visit turned into hours of conversation with employees about how the business actually worked, from timber sourcing to barrel production and shipping. It was the first time Buffett stepped beyond financial statements to understand a company from the inside out — a research habit that would define his career.

Buffett quickly saw that Greif’s business was in mild decline, but not necessarily doomed. The market, however, had already written off the entire industry. Wooden barrels were being replaced by steel and fiber drums, and investors assumed the end was inevitable. That excessive pessimism pushed Greif’s stock to absurdly cheap levels — exactly the kind of market mispricing Buffett was just beginning to recognize.

“Declining businesses are not worth nearly as much as growing businesses, but they can still be quite valuable if a lot cash is going to come out of them.”

Charlie Munger

But Buffett found a company trading far below the value of its assets, with a strong balance sheet, rational capital allocation, and a management team actively adapting to change. In short, Greif was a business in mild decline, but one that was deeply undervalued. In partnership with his father, he invested $3,650, his second-largest position at the time (15% of his total assets).

At the time of Buffett’s purchase in 1951, Greif Bros. Cooperage was trading at an very low valuation:

EV/EBIT 1–2×,

P/E 3–6×

When Buffett dug deeper, he found something remarkable. Despite operating in a declining industry, Greif’s underlying assets were worth far more than the market realized. Its net current asset value, the cash, receivables, and inventory minus all liabilities, actually exceeded the entire market capitalization. In other words, even if the company shut down and sold everything tomorrow, shareholders would walk away with more than the stock was trading for.

Here’s what he found on the balance sheet:

64% of assets were liquid — cash, receivables, and inventory.

30% were tangible assets — 239 factories, 11 offices, and valuable timberland.

The company had repurchased 30% of its outstanding shares, lifting book value by $12.40 per share.

Because the company used “LIFO” accounting, the value of its inventory on paper looked lower than it really was — since prices for wood and steel had risen sharply after the war.

As Buffett ran the numbers, he quickly saw that the company’s book value was $39.60 per share while its stock traded for only $18.25. The gap was too large to ignore as he was effectively buying a dollar for less than fifty cents, with all future earnings coming as a free bonus and getting all future earnings for free.

“He’d find something that was selling for one-fourth of liquidating value. He’d load up. So for a long period of time, he had a happy hunting ground. All he had to do was go through lists of liquid securities and slowly buy them, and he could get these ridiculous bargains.”

Charlie Munger

Buffett held his stake in Greif Bros. Cooperage for several years and likely sold it around 1956. By that time, the company had already begun a successful transition from wooden barrels to steel and fiber containers, a turnaround few thought possible. His estimated annual return was around 20 percent including dividends, not a home run but an outstanding result for a business in decline. Even though the business was indeed in gradual decline, management ultimately managed to turn it around, and the stock multiplied several times after Buffett sold. His mistake wasn’t in the analysis, it was in selling too soon.

Next, we move to Cleveland Worsted Mills (1952) — another classic “net-net” that looked cheap on paper but turned into one of Buffett’s early disappointments. Full story coming soon.

Getting Paid to Do Nothing

After meeting Charlie Munger, Buffett gradually shifted his investing style — moving away from “cigar butt” companies that were simply too cheap, toward wonderful businesses at fair prices. Yet ironically, that old approach produced some of his best results, helped by the fact that he was managing small amounts of capital at the time.

Personally, I believe the ideal investing approach is finding good businesses that can eventually become wonderful investments. A great business isn’t always a great investment. But I think I’ve found a few that are high-quality companies trading deep below their liquidation value.

Just like Buffett with Greif Bros., the market sees them as relics of dying industries. But the “sunset” could turn out to be long and beautiful. Pessimism has driven valuations absurdly low, while the balance sheets remain strong and robust.

So yeah… my grand investment strategy? Do nothing. Get paid. Repeat. Meanwhile, I’ll be here sharing cool ideas and the occasional bad joke. 😎

Cheers,

Sandro