Valaris (VAL): Why Offshore Drilling Is One of Energy’s Most Misunderstood Sectors

Until the Cash Flows Arrive

Looking at day-rates and utilization, my base case is that Valaris (VAL) will generate $1B in free cash flow (FCF) in 2026. There’s a strong probability that the following year will bring even more – perhaps significantly more.

If I look at companies capable of consistently generating $1B in FCF annually, the list isn’t very long. Of course, there are several – the world doesn’t revolve around Valaris – but very few trade at a ~$3B market cap while being able to produce ~$1B in FCF, and almost debt-free.

Here’s how Mr. Market values some companies with similar FCF:

Ferrari (RACE) – $1.3B FCF, ~$85B market cap

Created with TradingView Adidas (ADS) – $0.7B FCF, ~$30B market cap

Created with TradingView

Carvana (CVNA) – $0.6B FCF, ~$44B market cap

Created with TradingView

And now, Valaris (VAL):

expected 2026 FCF of $1B, yet trading at just a ~$3.4B market cap.

Sometimes Mr. Market gets overly excited, sometimes overly fearful. The asymmetry works in both directions. Some stocks remain “cheap” forever – but Valaris won’t. Why? Because it will aggressively buy back its own shares.

Other offshore players

Tidewater (TDW) – the leader in the OSV segment. Thanks to its short contract cycle, it reacts quickly to market changes. Drawback: vessels are faster and cheaper to build compared to rigs. Still, an interesting company worth following.

Noble (NE) – a solid company, but somewhat larger and more expensive than peers. Less exposed to jackups compared to Valaris, with a very healthy balance sheet.

Transocean (RIG) – carries a heavy debt load and relies on just a few 8th-generation rigs, making the risk/reward unattractive. Could perform well if those rigs deliver, but the risk remains high. Additionally, its capex must increase, and idle rigs are costly.

Borr (BORR) – heavily exposed to the jackup market and currently under strong pressure. Lost half its value in the last 12 months. A “pure play” on jackups, but not very attractive to me.

For me, Valaris (VAL) is the clearest and simplest play in the offshore sector. It has the largest fleet, a clean balance sheet with no debt, and capex limited to maintenance – meaning all FCF goes back to shareholders. Revenues are growing at double digits, while net income is rising three times faster than the top line. In addition, Valaris still has several 7th-generation rigs scheduled to come online in 2026/27, giving it organic growth potential unlike most of its peers.

Risks

I recently had a discussion with an investor I respect a lot, and he sees the following risks for the offshore sector:

First – new technology. The fear is that something like shale could happen again, for example a breakthrough that allows drilling much deeper or unlocking new reserves offshore. History shows that technological revolutions can change entire industries almost overnight.

Second – gas as an alternative to oil. Natural gas, especially LNG, is cheap and flexible. In some parts of the world, like Thailand and Malaysia, entire taxi fleets already run on LNG. If that trend went global, it could start eating into oil demand, at least in certain transport segments.

Third – the energy transition. Heat pumps replacing oil heating, hybrids and EVs replacing traditional combustion engines – the shift is happening. If electrification accelerates, oil could lose relevance faster than expected.

Fourth, falling oil prices would be a major risk.

My perspective is slightly different.

On new technology, I separate the possible from the probable. Shale was a once-in-a-century revolution. Could something like that happen offshore? In theory, yes. In practice, over the next five years, I see this risk as relatively low.

On gas/LNG, I agree it is cheap and flexible, but it does not truly replace oil except in limited niches. Oil remains the backbone of transport and many industries. That’s exactly why Buffett made his massive bet on OXY – he knows oil demand isn’t going away.

On the energy transition, the trend is undeniable. Heat pumps, hybrids, EVs – they’re growing. But globally we still have more than 1.4 billion combustion engine vehicles on the road. Even with fast EV adoption, this shift takes decades, not years. Oil will remain embedded in daily life far longer than most people expect.

On falling oil prices - this industry is highly misunderstood. Many think the main risk is falling oil prices, but that’s only partly true.

Shale works like this: you drill a well, get quick production, but it declines very fast. To keep output steady, companies must constantly reinvest in new wells. That makes shale very sensitive to oil prices, because if prices drop, new drilling stops and production collapses. Break-even is often $45–60 per barrel.

Offshore is different: yes, it requires much larger upfront investments and long planning, but once a field is developed, the cost per barrel is actually much lower and stable — often in the $30–50 range. Projects then produce steadily for decades.

That’s why long periods of low oil prices can actually benefit offshore. If shale becomes uneconomic, big oil companies may shift even more capital toward offshore, where production is cheaper and more reliable in the long run.

I honestly have no idea where prices will be in the future. If I had to assume, I’d say short term they remain volatile because of Ukraine, OPEC and geopolitics. But in the medium term, I see them more likely to rise. Demand is not falling fast enough, no new offshore rigs are being built, and the U.S. Strategic Petroleum Reserve has already been drawn down to about 400M barrels — the lowest level in 40 years.

And why did this happen? After Russia’s invasion of Ukraine, the Biden administration released 180M barrels — the largest drawdown in history — with the goal of pushing oil and gasoline prices lower to fight inflation. The result: the SPR has fallen to nearly half of its peak (~727M).

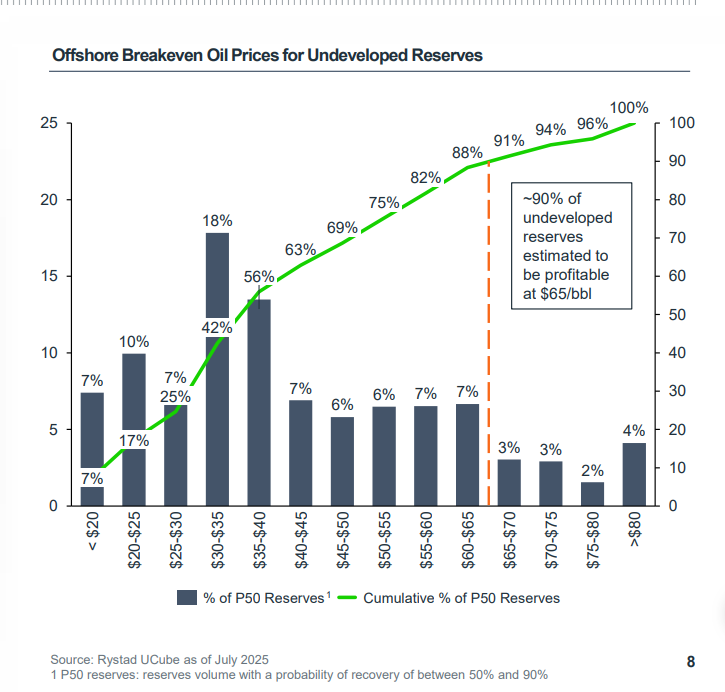

If another crisis hits, such a massive release simply cannot be repeated — the barrels aren’t there anymore. That’s why I believe the downside risk for oil is limited. And importantly, ~90% of offshore reserves remain profitable at around $65/bbl (see chart).

The real risk

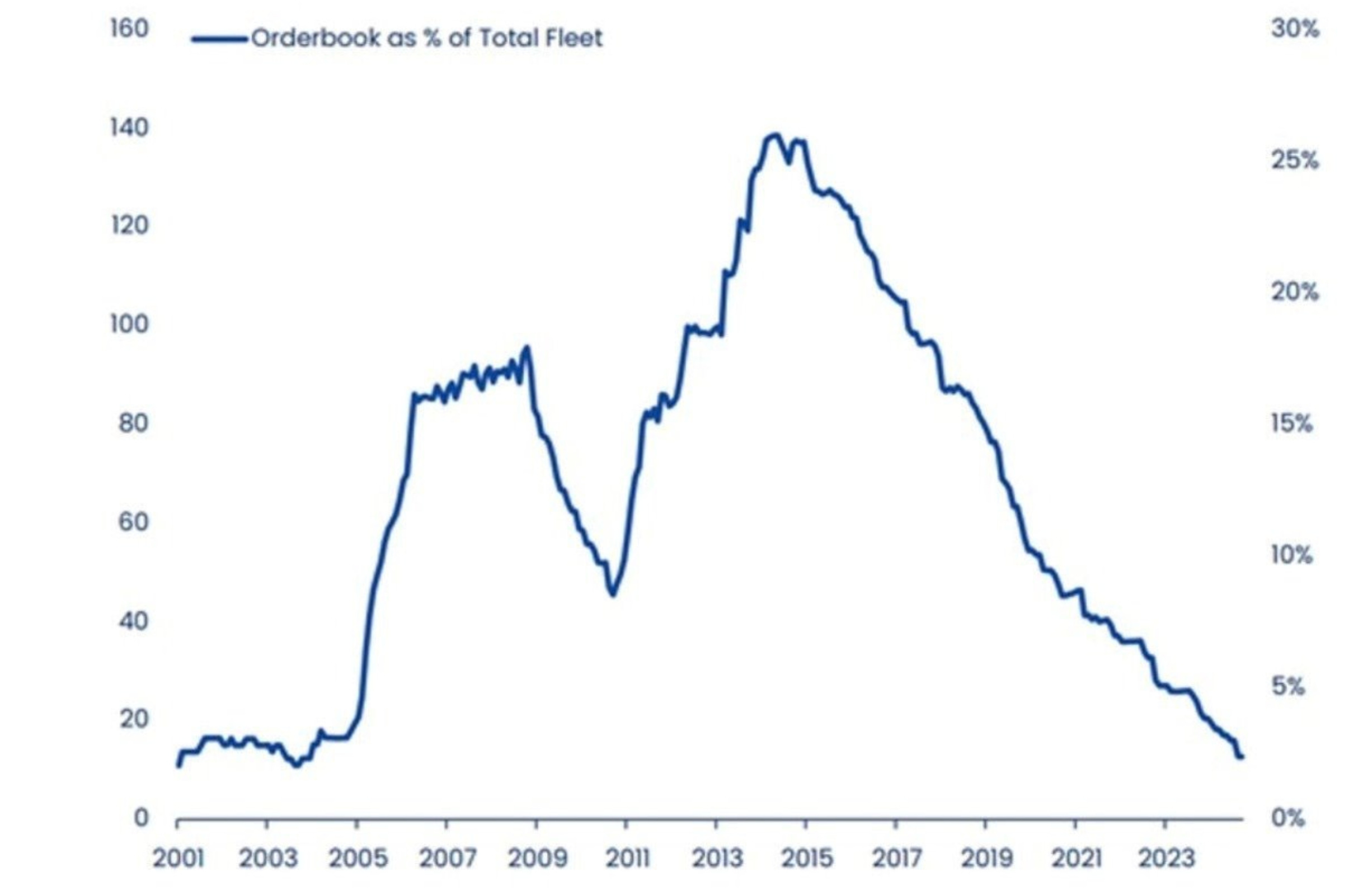

I can observe that offshore stocks have sold off this year, yet the fundamentals look stronger than ever. Balance sheets are cleaned up, debt has been reduced, and the sector now looks more stable than at any point in its history — while day-rates continue to rise. This isn’t about an explosion in demand, but about supply. There are no new rigs on the horizon, which is one of the most important signals in cyclical businesses.

A few years ago, these companies went bankrupt – a combination of rising onshore drilling and the pandemic crushed their balance sheets. Back then, they were overleveraged and extremely capital intensive. But that is the past. After debt was converted into equity, we are now entering a new phase: a capital-intensive business that has stopped being capital intensive.

The market hasn’t recognized this yet. Fear from the past still weighs heavily. The chart attached shows how a historic collapse in offshore demand destroyed the sector. That’s why these stocks are still trading at depressed levels. But the situation today is completely different.

Oil service companies are now in a unique position. After surviving a decade-long downturn, they’ve learned to operate at the lowest break-even levels. While most industries struggle in recessions, these firms are already used to depressed conditions—so any recovery in demand translates into significant upside. Day-rates, in fact, have been steadily rising since 2020.

I see only one real risk here.

Of course, a “black swan” event can always happen, but on the horizon there is only one threat: day-rates spiking above $800-900k. Whaat?!

Yes. Paradoxically, that sounds like a good thing, since Valaris could then generate $2–3B in FCF annually. But that’s exactly what would attract competitors: with such cash flows, they could easily finance newbuilds of the latest generation.

Yes, it takes 3–5 years to build, but if the market were flooded with new rigs, supply would rise and day-rates could collapse again. For me, that would likely be the signal to exit. And that’s what I’ll keep tracking together with you and openly share what I’m doing in my portfolio.

According to offshore company projections, offshore demand will require around 115+ modern rigs by 2030, while the market can only supply about 100.

So the only thing to monitor closely is if and when newbuild orders actually appear.

For now – there are none on the horizon, nor are there companies willing to build them.

Robert W. Eifler (CEO Noble), on the risk of new rigs entering the market:

— The risk of true new builds is practically zero. A new drillship would cost around one billion dollars and take four years to build, and it would require a 10-year contract with dayrates above $600,000. At the moment, nobody will do that.”

Cheers,

Sandro