Lumine Group (LMN.V): The Stock Mark Leonard Wants His Grandkids to Hold for 50 Years

Inside the Constellation spin-off that trades at half its all time high

Go read Part One first. I am serious. If you do not know who Mark Leonard is or what Constellation Software does this post will not make sense. Come back when you are ready.

For those who are caught up. At the end of that post I said I was not buying Constellation. Too big. The 140x is behind us. I said I was looking for the next Constellation.

I found it.

Its name is Lumine Group. It trades in Canada under the ticker LMN.V.

Let me show you what I found.

One Billion Devices

Before I tell you about Lumine I need to tell you about two phone calls.

The first call happened in 2018. Someone at Nokia picked up the phone and called Lumine. Nokia had a problem. They owned a video streaming software business called Velocix that they had inherited through the Alcatel-Lucent merger. It was a good business. Content delivery. Caching. Streaming personalization. Customers in 14 countries. But Nokia did not want it. It did not fit their strategy. They needed someone to take it off their hands.

Private equity would buy it. Gut it. Flip it in five years. Nokia did not want that. They wanted a permanent home for the engineers and the customers.

Lumine said yes. They bought Velocix. Restored the original brand name that Nokia had buried. Let the team run independently. Gave them capital and a playbook of 250 best practices.

By 2024 Velocix won the NAB Product of the Year Award. A business Nokia considered dead weight became an award winner.

Then came the second call. December 2023. Nokia picked up the phone again. This time the business was much bigger. Their Device Management and Service Management Platform. Software with roots in two prior Nokia acquisitions called Motive and mFormation.

This platform manages over one billion devices across 150 deployments worldwide. Broadband routers. IoT sensors. Multi-vendor device fleets. The software that telecom operators use to remotely manage every piece of hardware connected to their networks.

One billion devices.

Nokia wanted 202 million US dollars. Five hundred employees would transfer to Lumine.

Why did Nokia call Lumine a second time? Because the first deal worked. Velocix thrived. The engineers were happy. The customers were retained. The brand was restored. Nokia trusted Lumine.

Reputation compounds just like capital. I wrote that in Part One. This is what it looks like in practice.

The 90% Monopoly

Now let me tell you how Lumine was born.

In 2014 a man named David Nyland walked into Constellation’s Volaris Operating Group with a mandate. Build a communications and media software vertical from scratch. Nyland had the resume for it. Software developer at Accenture. Two CEO roles. Acquisitions across North America and Europe. He knew how to buy and build.

For nine years he did exactly that. Quietly. Deal by deal. Small telecom software companies. Billing platforms. Fraud management systems. Mobile optimization tools. By 2022 he had assembled a portfolio generating 228 million in revenue.

Then Constellation did something it had only done once before. They spun Lumine off as an independent public company. But the spin-off came with a gift. An acquisition so good it justified the entire separation.

WideOrbit.

WideOrbit is the system of record for over 5,000 broadcast stations and cable networks in the United States. It processes more than 35 billion dollars in advertising revenue every year. It commands 90% market share among US local TV stations for ad trafficking and sales.

Ninety percent. In an industry where the software is so embedded in daily operations that switching would shut down the station.

94% of revenue is recurring. Renewal rates are nearly 100%. Gross margins 70%. And here is the number that matters most. Before the acquisition WideOrbit’s estimated return on invested capital was 53%.

Constellation paid 490 million. Three times revenue. Eleven times EBITDA. Expensive by Constellation standards. But when you are buying a 90% monopoly with a 53% return on capital you are not overpaying. You are stealing.

The structure was genius. Lumine stock was used as partial payment. The founder Eric Mathewson joined the board and kept running WideOrbit as CEO. His wealth is now tied to Lumine’s success. Everyone has skin in the game.

One deal. Lumine nearly doubled in size overnight.

The CEO Who Came Back Twice

I have saved the best story for last.

In November 2023 Lumine bought two small business units from a Nasdaq-listed company called Synchronoss Technologies. Standard carve-out. 41.8 million dollars. Nothing remarkable.

Lumine did what it always does. Restored the heritage brand names. Openwave. RazorFlow. SpatialNetworX. Names that had been buried inside Synchronoss through years of corporate acquisitions. Lumine resurrected them. Gave the teams autonomy. Applied the playbook.

Jeff Miller the CEO of Synchronoss watched this happen from the outside. He watched his former divisions come back to life under new ownership. Two years later in December 2025 Miller called Lumine and said take everything.

All cash. Nine dollars per share. 258 million dollar enterprise value. Lumine took Synchronoss private. Delisted it from Nasdaq. Absorbed the entire company into the portfolio.

Miller himself said the former businesses “have flourished under Lumine Group’s stewardship.”

Think about what just happened. A CEO sold two small pieces of his company to Lumine. Watched them thrive. Then sold the entire rest of the company because he was so impressed. That is a referral. The most expensive referral in corporate history.

And it reveals something about Lumine that no financial metric can capture. When you are the buyer that makes businesses better instead of worse, sellers come to you. You do not have to chase deals. Deals chase you.

The Number That Changes Everything

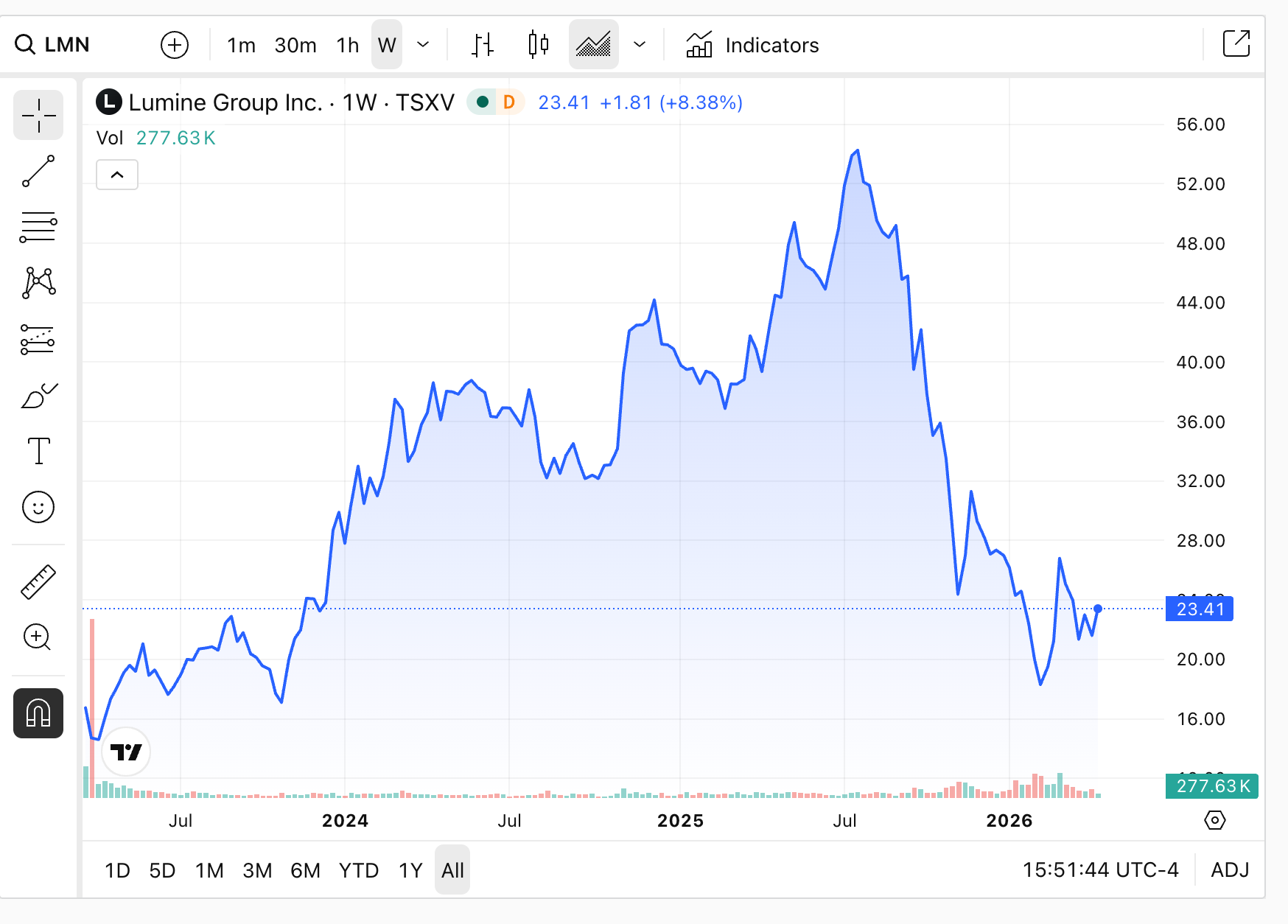

The stock is down 58% from its all time high.

I spent days going through Lumine’s filings, Constellation’s shareholder letters, RBC equity research, and every deep dive I could find. What I found does not make sense.

There is a single metric that Constellation’s entire empire was built on. The metric Warren Buffett called the difference between a great business and a mediocre one at the 1995 Berkshire Annual Meeting. The metric that determines how fast intrinsic value compounds per share.

Lumine scores higher than Constellation itself.

What follows is the full breakdown. The number. The formula Mark Leonard buried in his shareholder letters. A free cash flow model through 2035.

And my position.