Match Group: Is It a Buy?

The Stock Collapsed 80%. The Cash Didn’t. That’s Why I’m Interested.

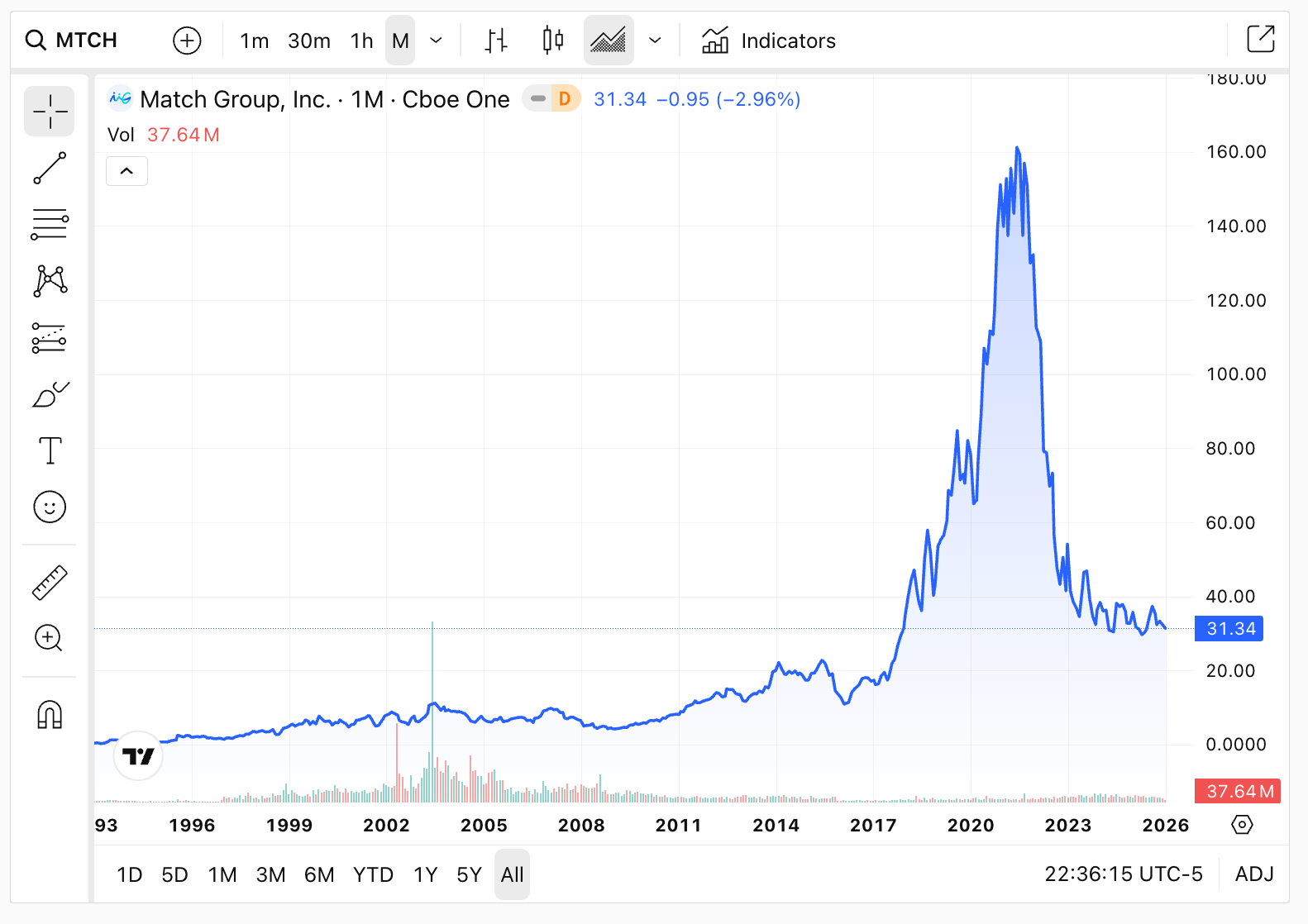

For years, this company grew fast. Then growth slowed. The market treated that as a death sentence. The stock collapsed more than 80% from the peak, because investors were pricing in smooth, perpetual 20% growth.

But this business is brutally profitable and spits out cash. Historically, roughly 85% to 90% of EBITDA has converted into free cash flow. It is capital light in the purest sense.

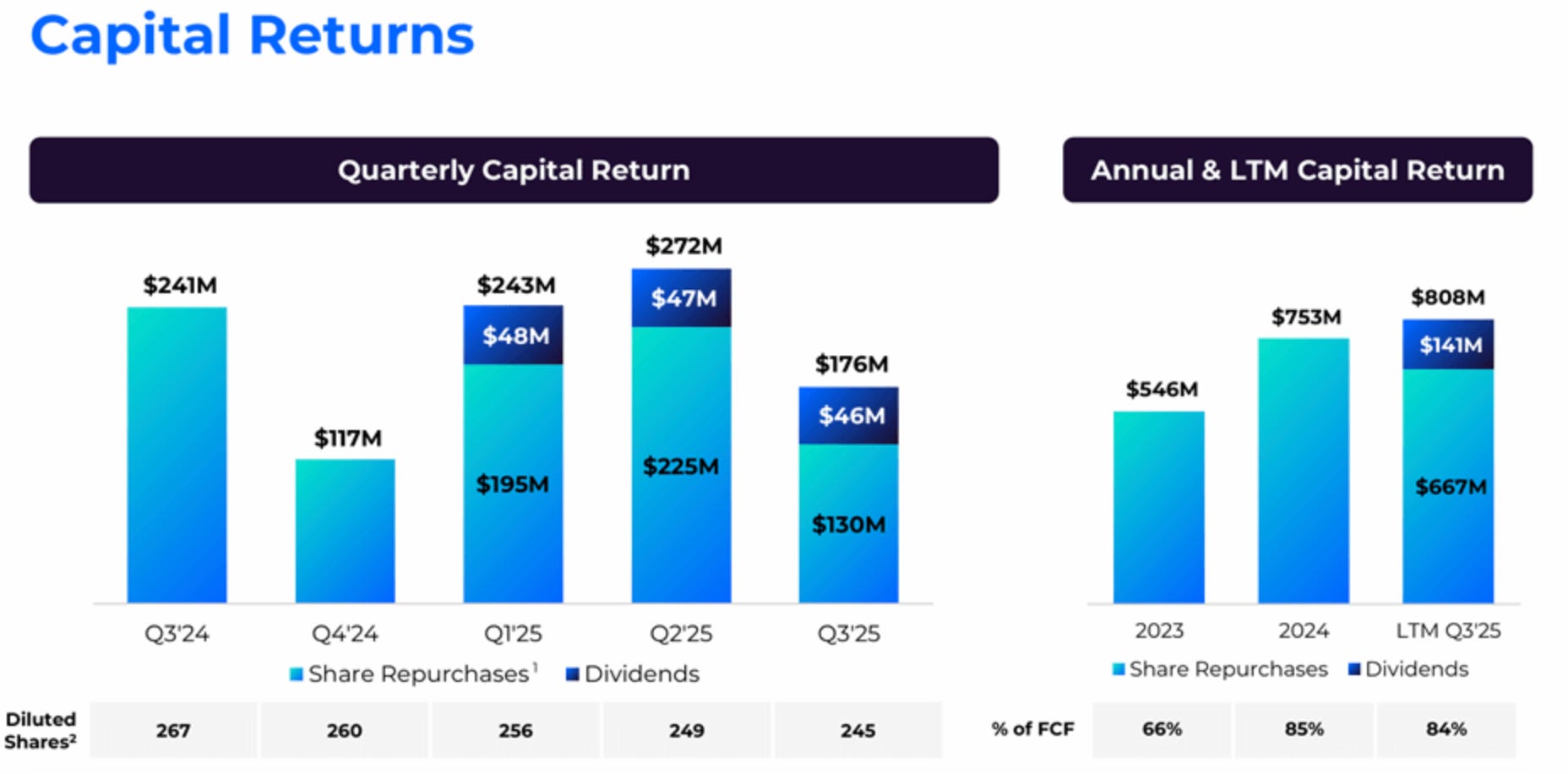

That is exactly where my interest starts. An 80% drawdown can be a gift when the underlying machine is still throwing off cash and sending it back to owners. Last quarter, they deployed 97% of free cash flow into share repurchases and dividends.

Management stated that over the next three years they intend to return at least 100% of free cash flow to shareholders through a combination of buybacks and dividends. That is enough for me to do the work. Now I am paying attention.

Dating Is No Longer Local

I used to think dating apps were bad businesses. Too much churn. Not enough alignment. People leave the moment the product works. Then I stepped back and it clicked. The best apps are starting to look less like entertainment and more like infrastructure. They are not selling romance. They are selling access to a matching engine. Taste changes. Trends fade. But a useful matching mechanism tends to stick.

I’m not saying dating apps are the best businesses in the world. I’m saying they’re not nearly as bad as most people assume.

To understand why, we need one step back. Before the internet, dating was bound by physical proximity. It was hyperlocal. A famous study from the 1930s looked at 5,000 marriage licenses in Philadelphia and found that a large share of couples lived within a few blocks of each other.

Then in 1995, Match.com shows up and deletes the proximity constraint. For the first time, people could search for a partner from home. And the candidate pool exploded, because the internet scales.

Today it goes further. You can filter for the exact person you want to see. Distance, lifestyle, values, even narrow preferences. That is a completely different world than hoping for a lucky encounter on a random night out. And it is better.

Winner Takes Most

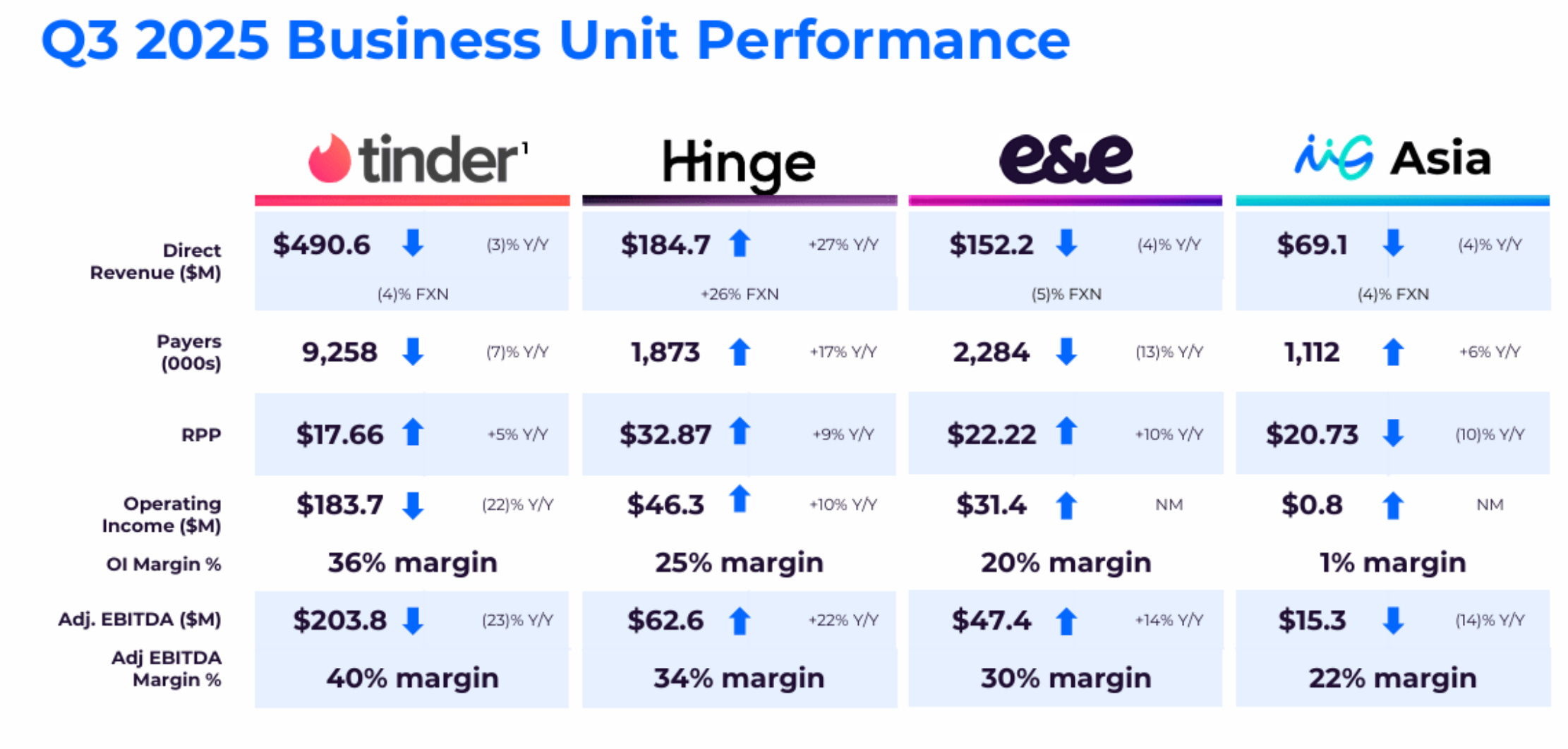

Match Group is the dominant player in the category. It is a holding company with more than 45 dating brands, including Tinder, Hinge, Match.com, Plenty of Fish, OkCupid, Meetic, OurTime, The League, and a range of smaller niche apps.

It sits around a $7B market cap and roughly $3.5B in annual revenue. Bumble is meaningfully smaller, roughly $1.0B of revenue. Grindr is the other listed peer, around a $2B market cap and roughly $0.4B of revenue.

After that, the market turns into a long tail. There are well over a thousand smaller dating apps. Most never become real businesses because without scale they never get enough user liquidity to monetize.

Match Group is estimated at roughly 250 million monthly active users. They have previously framed their addressable market outside China at about 700 million connected singles aged 18 to 65. Connected singles is the broader pool, while active singles and dating is the narrower slice. That alone suggests the market is far from saturated. Match has roughly 15 million paying users across its portfolio. Big number. Still small versus the pool of people who could eventually pay.

Assume a conservative $20 to $25 of monthly revenue per user and you get an annual market size of roughly $35 to $50 billion. Match generates about $3.5 billion today, which means the company is capturing less than 10% of the market it could realistically monetize.

This market is winner takes most. Liquidity is the moat. Scale is the moat. Starting a new app is easy. Scaling it to meaningful liquidity is brutally hard. Consumer tastes can change, sure. But building enough density to threaten Tinder is rare. And Hinge is a very good app. You need a clear, differentiated value proposition and even then the odds are against you.

The Economics Behind the Swipes

Most of these businesses run a freemium model. The free tier exists to create liquidity and pressure. The paid tier exists to monetize urgency and outcomes. Users can enter for free, but the experience is throttled. Limits. Friction. Waiting. The upgrade is the escape hatch.

Revenue comes in two buckets. Subscriptions and à la carte purchases. For Match, subscriptions are roughly 70 percent of revenue, with the rest coming from add-ons like boosts and super likes. Tinder adds another layer with multiple subscription tiers. And the apps are addictive. In an age when people go out less, it’s easiest to pay a few dollars and look for a partner from the comfort of home.

There is a paradox at the heart of this business. When two people meet and enter a relationship, the platform loses two users. In Hinge’s case, that is literally the product goal. From a pure shareholder perspective, that looks misaligned.

Casual users are economically more valuable. They stay longer. They churn less predictably. Their lifetime value is higher. Yet there is an indirect payoff most investors miss. Couples who meet through these apps become lifelong evangelists. They don’t just leave. They advertise the product for free.

I used Hinge for testing.

The app is brutally addictive and extremely clean. Everything is fast, intuitive, and clearly designed to keep you engaged. What’s interesting is the philosophy. Hinge is built to be deleted. That means users are willing to pay a lot, but supply is also deep. In the right location, the odds of actually finding a partner are high. Photos are optimized hard. Profiles look like Instagram. People almost always look better than in real life, likely due to filters and careful curation. Visually, it pulls you in.

The price is the other side of the coin. In Europe, it’s around €72 per month. That’s expensive for a dating app. But it is a lot of cash flowing to Match shareholders, without the need for heavy reinvestment or large ongoing costs.

If my wife finds out I paid €72 and scrolled Hinge all night, I will calmly explain this was deep research for Substack. No new posts for a few days means I lost everything and became a full time bridge resident. 🙂

An 80% Collapse That Changed Nothing

Growth was strong for years. Tinder compounded at roughly 40% annually over a five-year stretch. Then growth slowed to about 9% last year and the stock collapsed.

What didn’t break was the business.

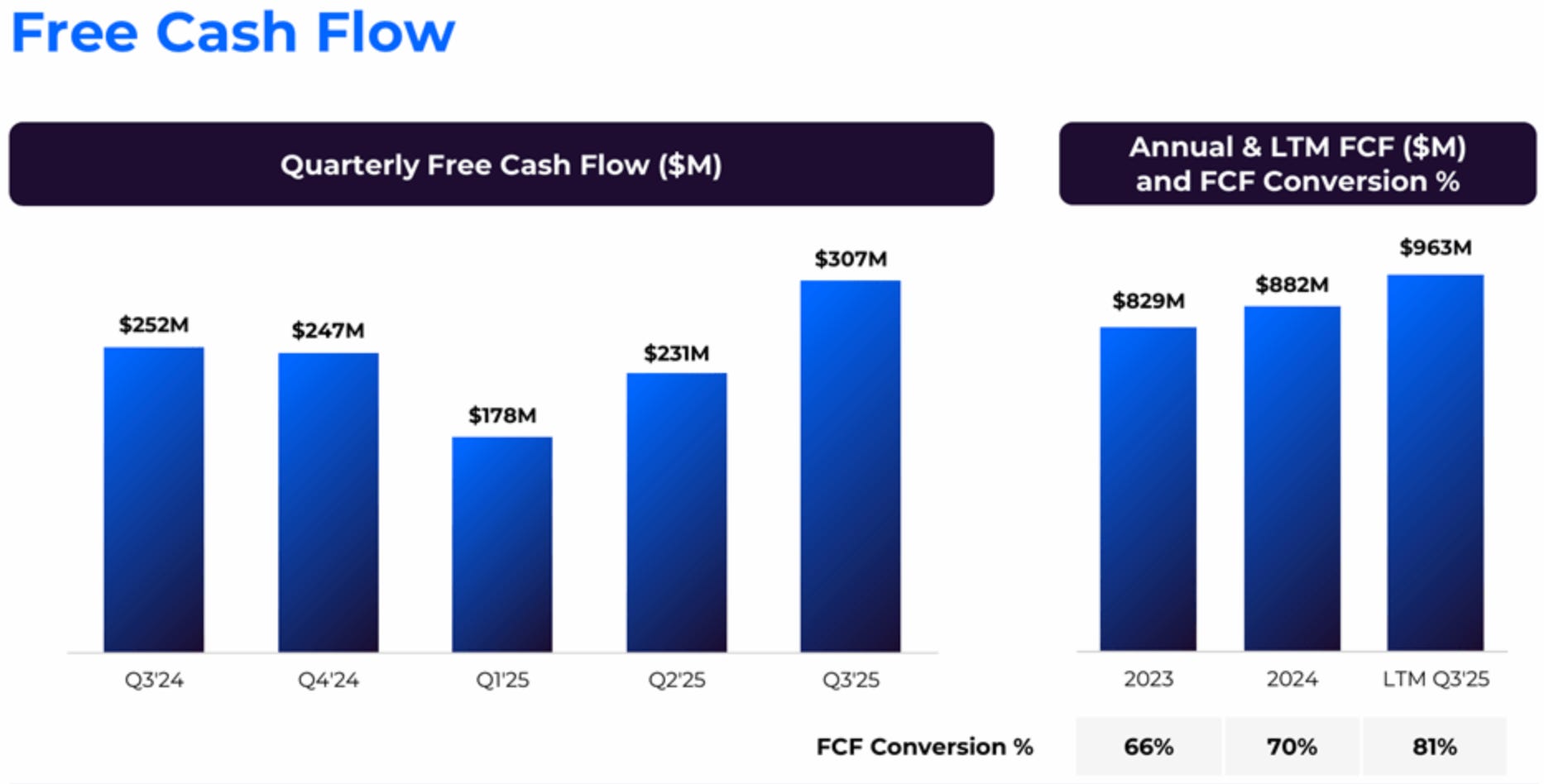

Through the first nine months of 2025, Match generated $963 million of operating cash flow and approximately $716 million of free cash flow. Management later raised full year 2025 free cash flow guidance to about $1.11 to $1.14 billion. Match is best described as a pure cash cow.

This is a capital-light machine. Over the past decade, cumulative capex was under $400 million. That’s barely 12% of last year’s revenue. The business requires minimal reinvestment through either the P&L or the cash flow statement to sustain itself. The consequence is unavoidable. There aren’t enough reinvestment opportunities to absorb the cash it generates. Capital has to flow back to shareholders. Great.

One structural drag has been the Apple App Store fee. The shift from web to mobile brought a toll booth. Over the past eight years, Match more than tripled revenue, yet gross margins fell from roughly 87% to about 70%. Last year alone, Match paid roughly $650 million in app store fees, about 20% of revenue. That is real money leaving the ecosystem.

The Risk Reward Setup

There are potential catalysts. EU regulation through the Digital Markets Act. Ongoing antitrust pressure on Google. If the App Store take rate were cut from 30% to 15%, EBITDA margins would expand by roughly nine percentage points.

On conservative assumptions, Match could approach $5 billion of revenue by 2027, with roughly $1.7 billion of EBITDA and over $1.5 billion of free cash flow. After buybacks, that points to around $6 of free cash flow per share. At a 12x multiple, that implies roughly a mid-teens IRR. With modest upside assumptions and potential fee relief, returns push into the high twenties.

The primary risk is higher marketing spend. A less discussed risk is technological change. AI could reshape user behavior. AI chatbots already blur authenticity. More extreme scenarios, like AI companions, sound absurd but cannot be fully dismissed.

As for Meta, despite its scale and data advantage, Facebook Dating has so far been a non-event. Trust issues remain. Monetization is unclear. And dating is not a strategic priority for Meta.

Here is what the CEO said.

We’ve always had competitors. I’m sure we’ll always continue to have competitors, whether they be big tech companies or startups.

So to the extent that Meta and Facebook or any competitor educates people that they can use a dating app, they can use the power of technology to safely meet people and get up off the couch and go out on dates and form human connections that benefits Match Group as the category leader, especially because this is a category with multi-app usage.

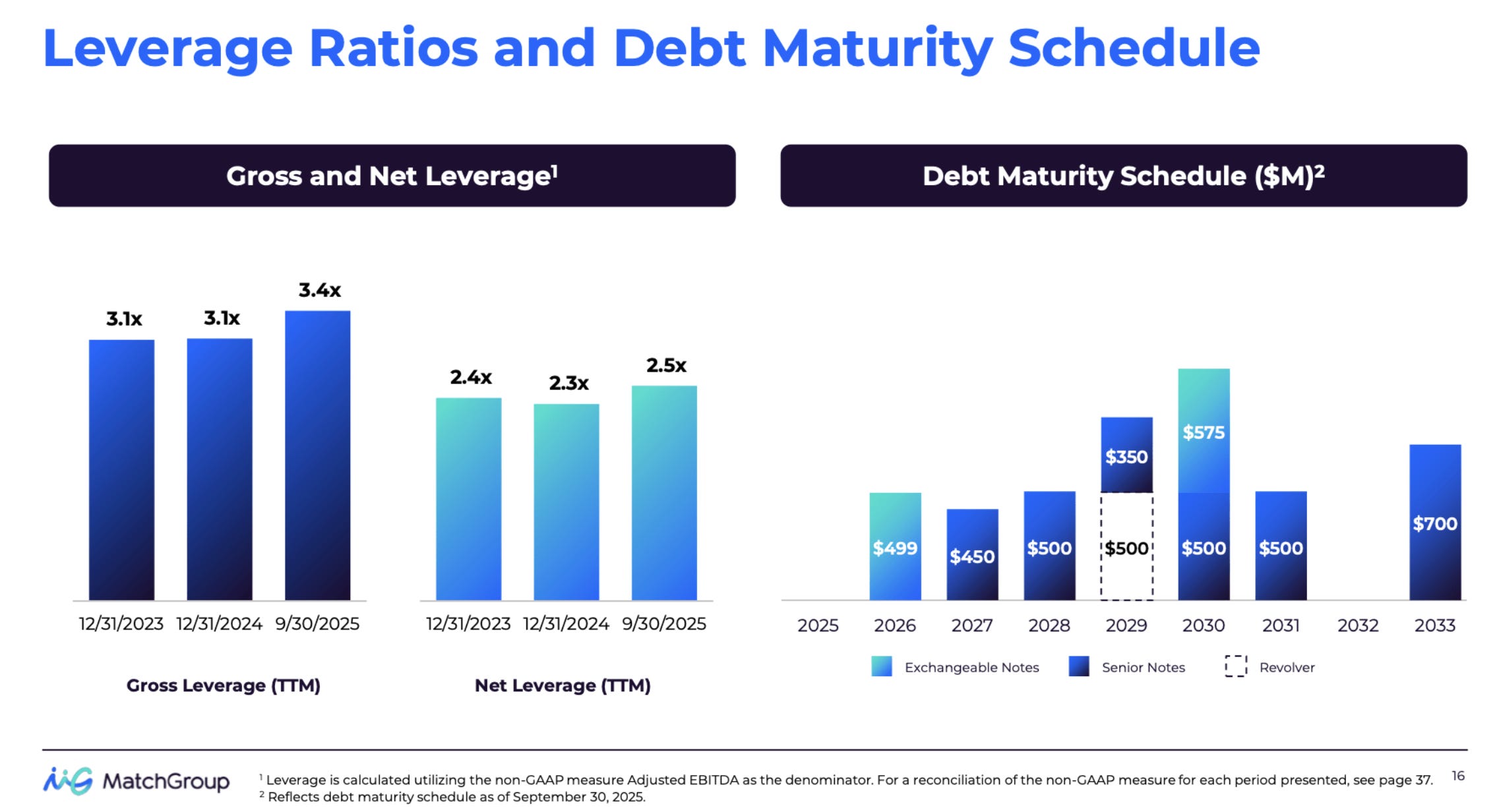

Debt is also a risk, but it’s a mild one here. Match carries leverage, yet it looks controlled. Net debt is roughly $3 billion. Annual free cash flow is close to $1 billion. That’s about 3x FCF. Not aggressive.

Maturities are spread out. There is no single-year wall. Interest expense runs around $140 million per year, which is easily covered by free cash flow.

Capital Allocation as Strategy

Capital allocation is the core of the story now.

Buybacks are the main tool. Dividends are secondary, but steady, running around $140 million per year.

Capex is low. This business does not need heavy investment in physical assets to operate or grow. And there is no aggressive M&A push. The focus is on improving the existing portfolio, pricing, conversion, and product execution.

This is a free cash flow machine that behaves like a cannibal. Capital is not being wasted. It is being returned.

The Reasons To Say No

Match Group trades at a very low valuation for a tech company. Roughly $7 billion for a business that can realistically generate $1 to $2 billion of free cash flow per year, with almost all of it going into buybacks. If you believe the business can grow or at least remain stable over the next few years, why say no?

If this business goes into decline, buybacks can destroy value. But if the business remains stable or grows while aggressively reducing the share count, returns can be brutal. The post below is very important.

I keep asking myself a simple question. Will people still use Tinder to meet in ten years? The honest answer is I do not know. And if I have to lean one way, my instinct says probably not.

Please watch the video below and focus on what Elon says about where apps may go over the next five to six years. If that shift hits dating, the current model can get disrupted faster than a discounted multiple can compensate for.

Buf if this business just stays stable for the next five to seven years while putting $1 billion a year into buybacks, the math gets violent. And this is still a tech company. If sentiment ever turns, you don't just get earnings growth, you get a multiple expansion on top. But I cannot get past the uncertainty around what dating looks like in five years. So for now, Match stays on my watchlist only.

Cheers, Sandro.