October 2025 Portfolio Breakdown: AMR, Valaris and Athabasca Oil

Three companies, almost no debt, and 100% FCF to shareholders

My portfolio updates and plans will be reserved for paid subscribers.

There, I’ll speak openly and transparently — before I buy or sell anything — including what I plan to do next.

Since my Substack is still relatively new, and there have been a few portfolio changes recently, we’ll start tracking performance officially from next year. Although I don’t think that’s particularly important — when a portfolio consists of only a few names, like mine, there can be years where nothing major happens… and then suddenly, in just one year, the big returns happen. Still, for the sake of transparency, we’ll track performance going forward. I manage a private six-figure portfolio (hopefully seven soon), as well as the portfolios of a few clients and my children.

My investing approach is very simple. I ask myself two questions: How much am I paying — and when will I get my money back? If I can get it back in one, two, three, or even four years, I’m usually interested to dig deeper. But if I’m paying for something like Tesla with a P/E of 250, meaning it would take 250 years of current earnings to get my investment back, I’m not interested — and I move on.

Beyond that, I look at debt, because debt can easily destroy an otherwise great investment. And I care deeply about management — I only want to invest in companies where management is willing to return a meaningful part of earnings to shareholders, because that’s the whole point of owning public companies in the first place.

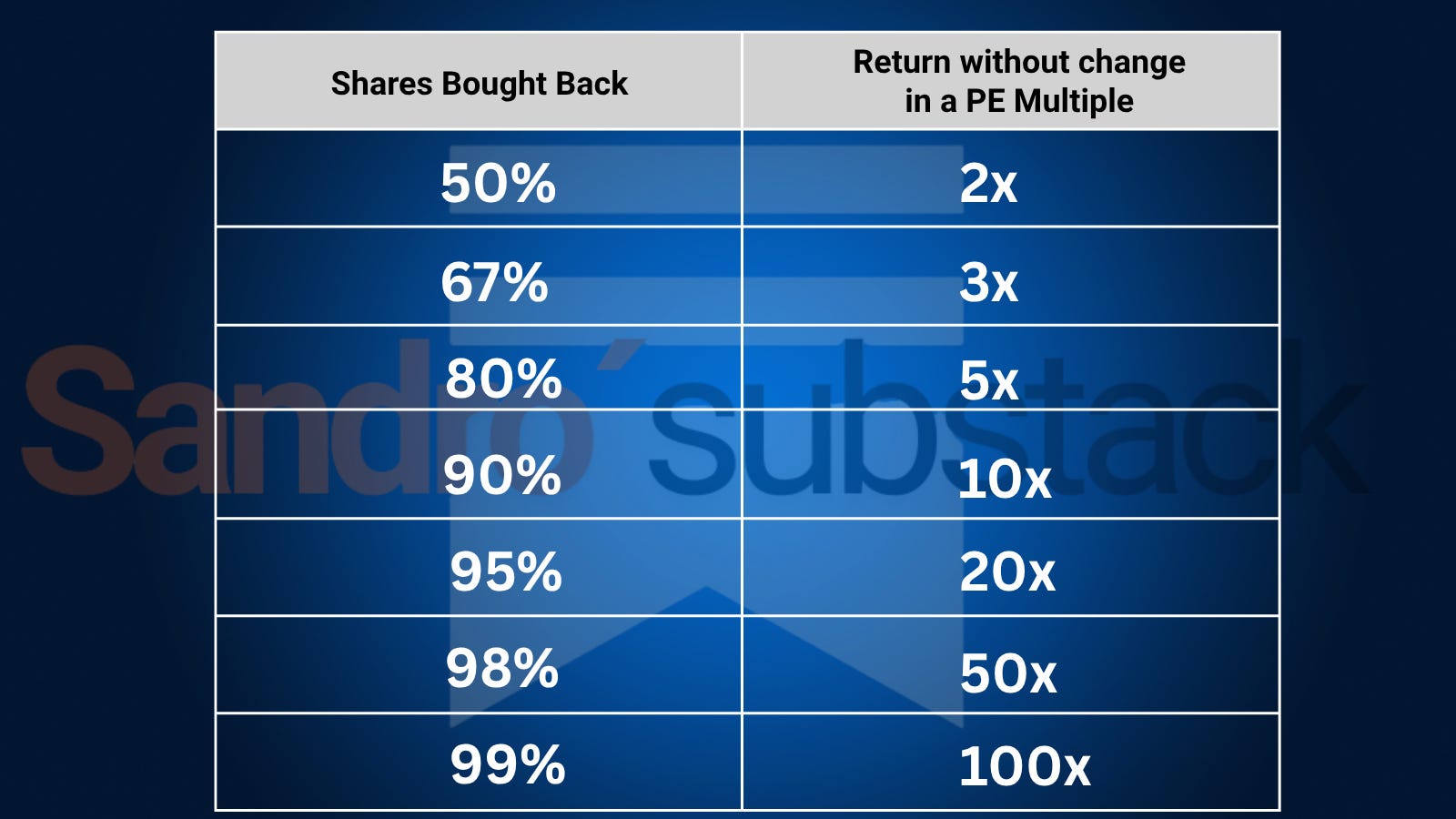

Because my portfolio is focused on companies that are shareholder-friendly, I want to briefly explain how buybacks actually work. All three companies I own have just started to “eat themselves.” In the early stages, the share price usually does nothing — and that’s perfectly fine. Historically, once a company repurchases around 50% of its own shares, the stock tends to double. And things get truly interesting once 80–90% of the shares are gone.

I believe my portfolio is bulletproof.

And although it may sound counterintuitive, I actually want my stocks to fall as much as possible — because that will get us to the goal faster. So, to be honest, I don’t expect any major performance next year — and I actually hope the prices stay low. Lower prices allow these companies to buy back their own stock even faster.

It’s really that simple.

And I’m comfortable having 100% of my net worth in just three stocks.

Why?

Because every company I own has almost no debt, generates strong free cash flow, and aims to return 100% of that cash to shareholders through buybacks — the best form of capital return there is.

So, let’s begin.

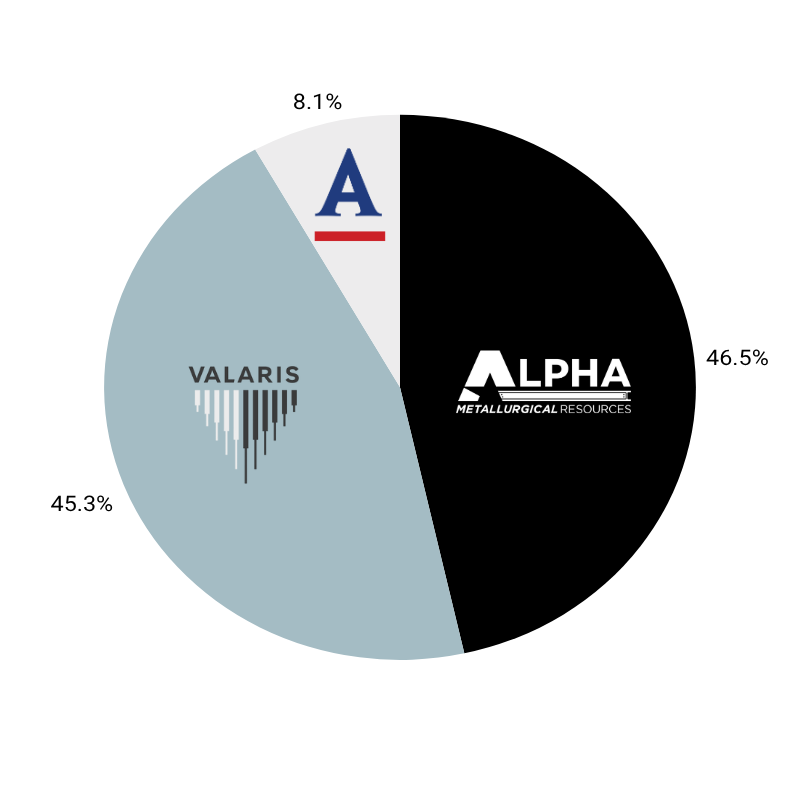

My Current Portfolio (on invested capital basis)

Alpha Metallurgical Resources (AMR) - 46,5%

Average cost: $136,50/share

Valaris (VAL) - 45.3%

Average cost: $49.45/share

Athabasca Oil (ATH.TO)

Average cost: $4.80/share (C$6,70)

Alpha Metallurgical Resources (AMR)

Coal is an industry I’ve been working in for several years, so my position in Alpha comes from first-hand understanding. I see what’s happening on the ground every day. Although I work in Germany for RWE — at a site where coal is still being produced — it gives me a unique angle. I often notice small things others might overlook.

RWE originally planned to shut down coal-fired plants by 2029 (the same year my current contract runs), but now they’re already talking about extending operations to 2032, and some even say 2038. And the irony is: the more mines shut down, the better it gets for Alpha.

The supply side of coal is structurally tightening — mines are closing due to political and ESG pressures — while demand keeps rising organically, especially in Asia. Even just the end of the war in Ukraine and its reconstruction could create a 10–15 million ton annual supply gap. And I honestly don’t know where that coal would come from. That’s why I expect sustained — and at times extreme — coal prices in the years ahead.

From an investment perspective, Alpha’s case is simple:

It’s a debt-free company with arguably the strongest balance sheet in the entire sector, exceptional management and capital allocation fully aligned with shareholders. If I had to, I’d be perfectly comfortable having 100% of my net worth in this company alone. I think it’s very important with Alpha to be extremely patient — and to be among the last ones still holding the stock.

For the full details of my thesis, you can read my Deep Dive here:

I also analyzed this industry more deeply in my book “How to Invest in Stocks.”, which is currently available in 6 languages.

Valaris (VAL)

The investment thesis for Valaris is also straightforward. Valaris went bankrupt in 2020 and later re-listed, with all of its former debt converted into equity. That event is crucial — because on the company’s balance sheet, you won’t see the rigs they actually own. (just like Alpha’s coal).

Today, Valaris has a market cap of around $3.5 billion, while the replacement value of its rigs is over $25 billion. No one is building new rigs anymore — they’re too expensive, and banks refuse to finance them due to ESG restrictions. After the 2020 bankruptcies, rig construction practically stopped. Building a new rig takes around five years, and as of today, not a single company has filed a request to build one. By 2030, the world is expected to need around 115 active offshore rigs, while today there are roughly 80 — and the odds are high that there will be even fewer by then.

Another important tailwind for Valaris is the oil price itself. Unlike shale, which needs around $60 per barrel to break even, offshore production remains profitable even at $30–40. That means lower oil prices actually benefit Valaris, as they make offshore projects relatively more attractive compared to shale.

This imbalance will inevitably lead to much higher day-rates, which means massive free cash flow for Valaris — a debt-free company returning 100% of FCF to shareholders through buybacks. Both Alpha and Valaris could soon be in a position to generate in a single year as much free cash flow as their entire market cap.

Here I wrote more about Valaris and the offshore industry:

Athabasca Oil (ATH.TO)

Athabasca is also a simple business — but unlike Valaris, it’s directly tied to the oil price. Charlie Munger once said that we’ll see extremely high oil prices in the future, and I tend to agree. Most oil producers remain concerned about uncertain demand, but in the long run, I believe demand is far more predictable than supply — and that’s precisely the core of the oil investment thesis.

Athabasca is a low-cost producer, with a breakeven around $40 WTI. Even with relatively low oil prices in recent years, the company generates about $500 million in net income on $1.5 billion in revenue. That’s the moat.

By 2030, Athabasca plans to almost double production, and it holds reserves for roughly 90 years. It has zero net debt, and returns 100% of free cash flow to shareholders through buybacks. We’ll see the upcoming results soon, but so far in 2025, I assume they’ve already repurchased about 10% of the entire company.

In essence, all three companies I own share one thing in common — they’re hated.

Because of ESG restrictions, most funds and institutions aren’t allowed to invest in them, which keeps them deeply undervalued. But that’s exactly the perfect setup for buybacks to do their magic. In the ideal scenario, this situation doesn’t change — and the share prices stay low.

From here on, this section is for paid subscribers only.

I’ll briefly go over what I’ve sold recently and what I’m planning to buy next in the near future — including the reasoning behind each move.