Noble (NE) vs Valaris (VAL)

Which offshore driller is the better long-term bet?

Offshore drilling is slowly entering a new supercycle — and almost no one is paying attention. After a decade of bankruptcies and oversupply, the rig market has completely reset. The fleet is smaller, the balance sheets are clean, and the probability of massive free cash flow ahead is enormous.

The offshore industry has a few solid players — but I think two companies are going to truly dominate this space: Valaris (VAL) and Noble (NE). Both trade far below what their fleets are actually worth. Both are going to generate serious free cash flow. And both could be early winners of the next offshore cycle.

So the question is: which one would I rather own?

Here’s what we’ll look at:

Fleet value

Backlog

Growth

Capital allocation

Valuation

Let’s dive in.

Fleet worth

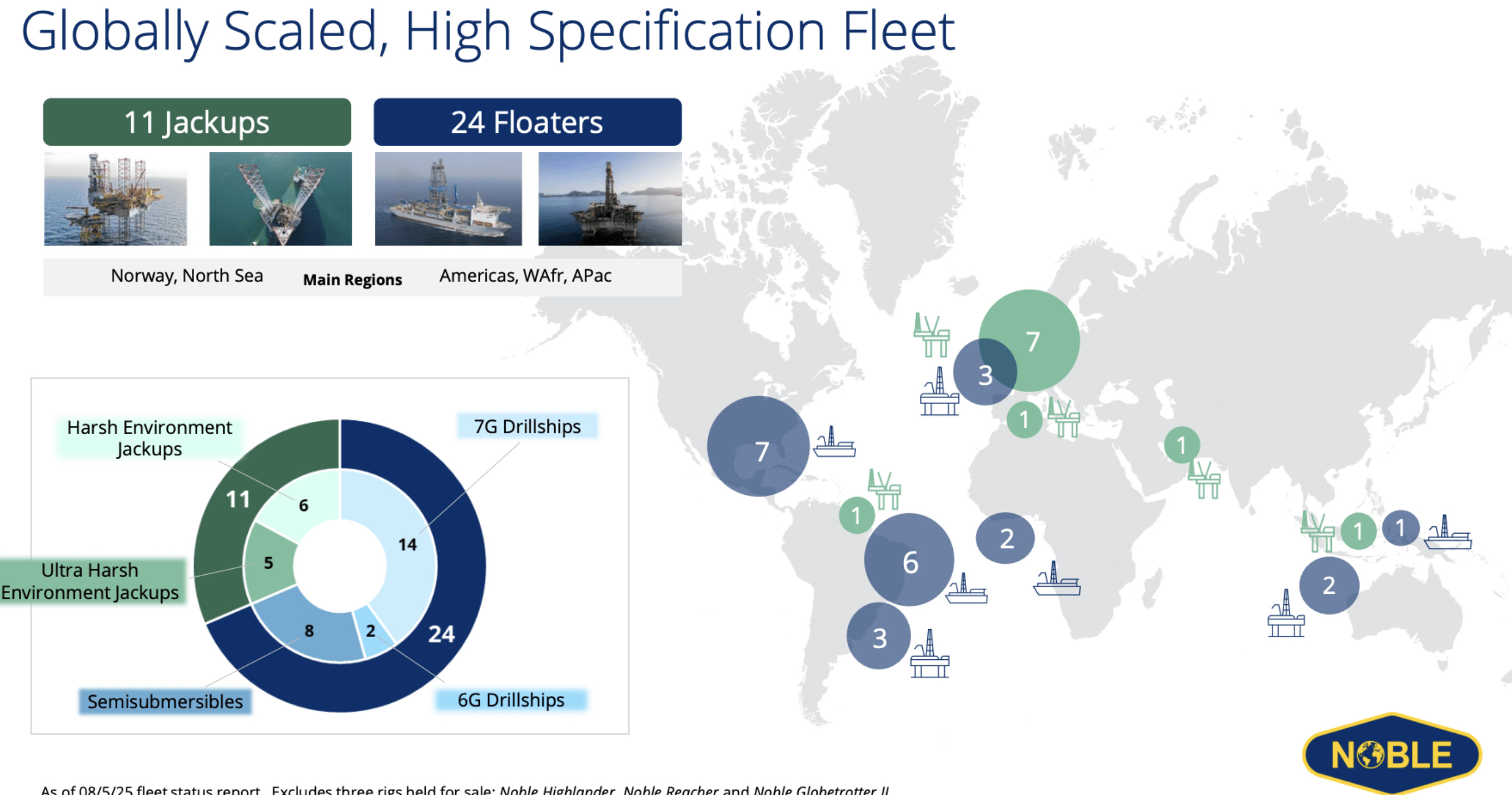

Noble

Today, Noble operates one of the youngest and most advanced fleets in the entire offshore drilling industry. Its portfolio includes both floating deepwater rigs (drillships and semisubmersibles) and self-elevating jackups for shallow-water operations.

After a bankruptcy restructuring in 2020, Noble completely transformed itself. In 2022, it merged with Maersk Drilling, and in 2024, it acquired Diamond Offshore. These two deals turned the company into a global player with a fleet scale comparable to the largest competitors and operations across all key offshore basins — the North Sea, Gulf of Mexico, West Africa, and Asia-Pacific.

Over the past year, Noble has continued to strengthen its position through fleet optimization. It is actively selling older, less efficient assets and focusing on modern, high-margin rigs. In June–July 2025, Noble sold two cold-stacked drillships for $41 million and agreed to sell the idle jackup Noble Highlander for $65 million. Two more rigs Noble Globetrotter II and Noble Reacher — are currently held for sale.

As a result, the share of modern rigs in the fleet continues to increase. Key assets such as the Noble BlackHawk, Noble Tom Madden, and Noble Venturer are central to the company’s competitiveness and cash generation.

Fleet overview (mid-2025)

Total rigs: 35

24 floaters (14 drillships, 8 semisubmersibles, 2 management/service units)

11 jackups (6 harsh-environment, 5 ultra-harsh-environment)

Generations: mostly 6th- and 7th-generation rigs

Estimated replacement cost: over $35 billion

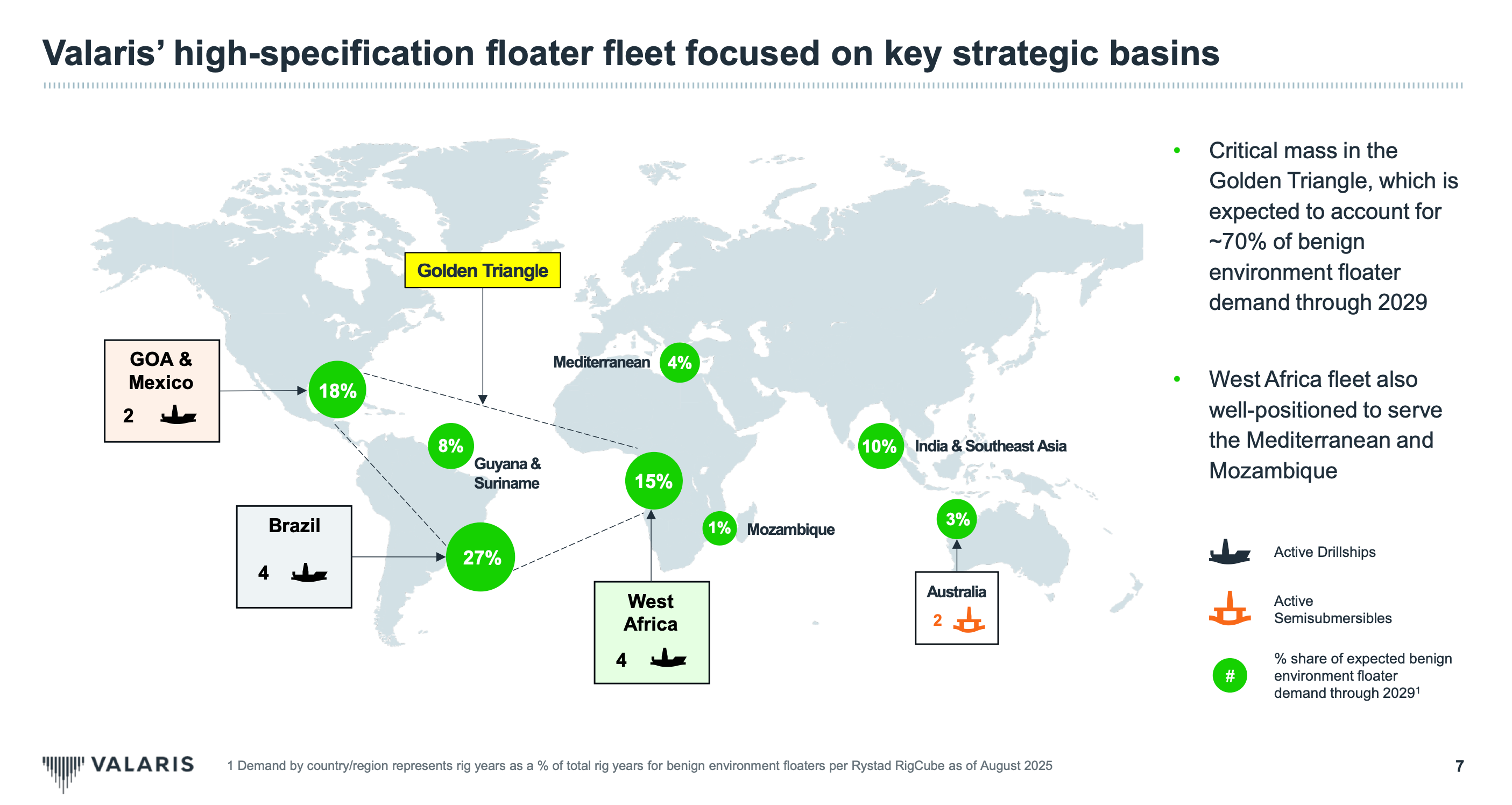

Valaris

Valaris represents a more conservative, less levered way to play the offshore cycle. Its 7th-generation drillships are among the most advanced in the world — more efficient, safer, and capable of handling the most complex deepwater projects. These rigs command premium day-rates and are the core driver of Valaris’s value creation.

Fleet overview (mid-2025)

13 seventh-generation drillships

2 harsh-environment semisubmersibles

22.5 jackups (8 harsh-environment, 14.5 benign, including 4.5 through a 50% JV with ARO Drilling)

Estimated replacement cost (Westwood, Offshore Journal, S&P Global):

Drillships: about $1B each

Semis: $700M–$900M

Jackups: $175M–$250M

Estimated replacement cost: over $25 billion

Noble takes the early lead — its fleet is larger, newer, and spread across every major offshore basin, giving it scale and flexibility that Valaris still lacks.

1–0 for Noble.

Noble wins on steel. Now comes the second test — how much money these fleets are actually locking in. Let’s look at the backlog.

Backlog

For those encountering the offshore industry for the first time, let me briefly explain what backlog actually means. Backlog simply means the total value of signed contracts that haven’t been completed yet — future work that’s already guaranteed.

But here’s where most people get it wrong: a bigger backlog isn’t always better.

Right now, offshore demand is strong — driven by new deepwater projects in Namibia, Brazil, Guyana, and West Africa. About 80 drillships are active worldwide, yet forecasts suggest demand could soon exceed 100, while actual supply may drop below 80 as many older rigs retire and no new ones are being built.

That’s why, ironically, a shorter backlog can be an advantage today. Companies with rigs rolling off contract in the next year or two will be able to reprice at much higher day-rates once the market tightens.