Notes from the Singapore Coking Coal Conference 2026

The Singapore Coking Coal Conference is one of the few times each year when the people who actually move this market are in one room. Traders, producers, the big Indian and Chinese steelmakers, the price agencies. If you want a read on where seaborne met coal is heading, this is about as good a signal as you get. So I went through everything that came out of it, and here are the takeaways that stuck with me.

The one line summary is that met coal is really two markets now, and most headlines miss it.

1. There are two coal markets, not one

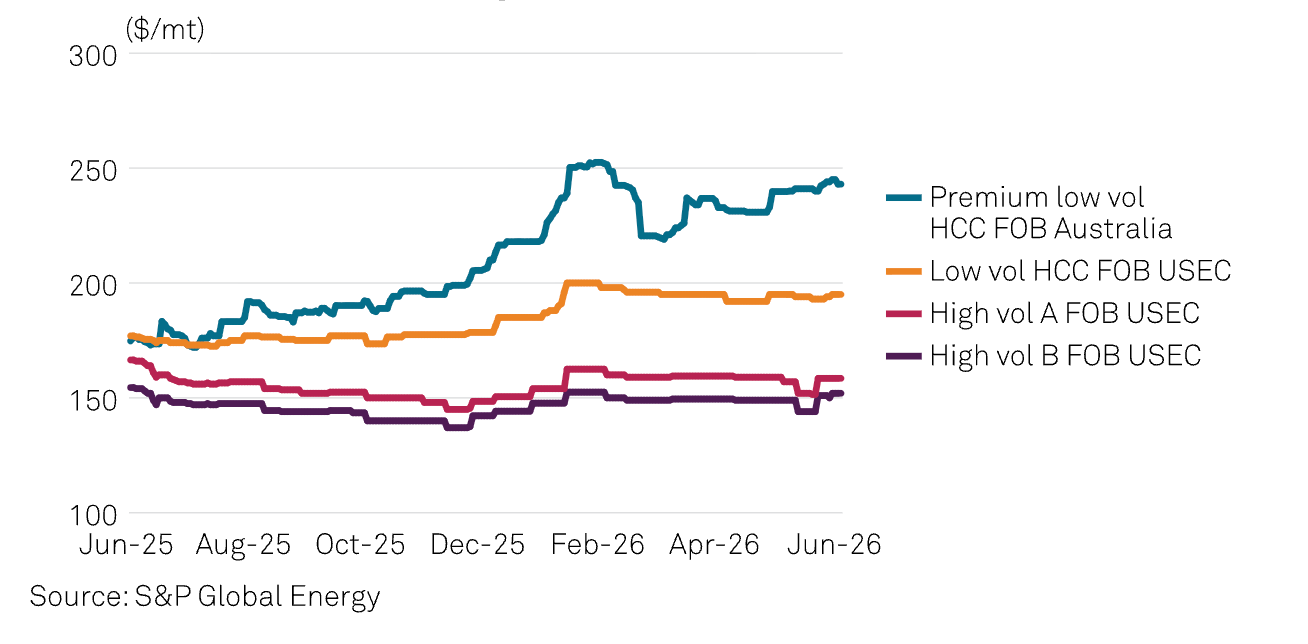

There is ordinary coking coal, and there is premium, high quality coal. People lump them together, but they are behaving very differently.

The lower and middle of the market is fine. New supply keeps coming from Mongolia and Indonesia, and prices there are calm. The premium end is the opposite. That is the good coal the big steelmakers cannot substitute, and it keeps getting tighter. When you hear that coal prices jumped this year, that is the premium part. The cheap stuff is not the story.

2. The China accident did not cause the tightness, it exposed it

In late May a gas explosion at a mine in Shanxi killed 82 people, the worst Chinese mining accident since 2009. Inspectors then shut more than a hundred mines. Shanxi makes about a quarter of China’s coal, so this was big.

The interesting part is that the mines did not fully reopen. Before the accident they were running above their official capacity, over a hundred and ten percent. After, the safety crackdown pushed them down to seventy or eighty. One trader thought the lasting loss could be twenty to thirty million tonnes even after restarts. And it hit the good coal hardest, the exact grades you cannot get from Mongolia or Russia. So China went and bought Australian and Canadian premium instead, and prices jumped. The accident just reminded everyone how thin the premium market already was.

3. Australia is not going to grow

This is the big one. Normally when premium prices rise, Australia digs more, since it sells more than half the world’s seaborne met coal. Not this time.

Australian exports are flat, around 150 to 160 million tonnes, and it is structural. Queensland brought in a brutal royalty regime in 2022. You can see it in the decisions. BHP suspended a mine and cut hundreds of jobs, blaming lower prices and higher royalties, and passed on another project. Exploration spending has dropped hard. The line that stuck with me most from Singapore was that only three new met coal mines are confirmed to start anywhere before 2030. Three. For the supplier that carries half the world’s premium coal. So when a shock hits, there is no wave of new Australian tonnes waiting.

4. Mongolia and Indonesia do not fill the gap

The obvious pushback is that Mongolia and Indonesia are growing, so it will ease. Both are growing, and both help less than you would think.

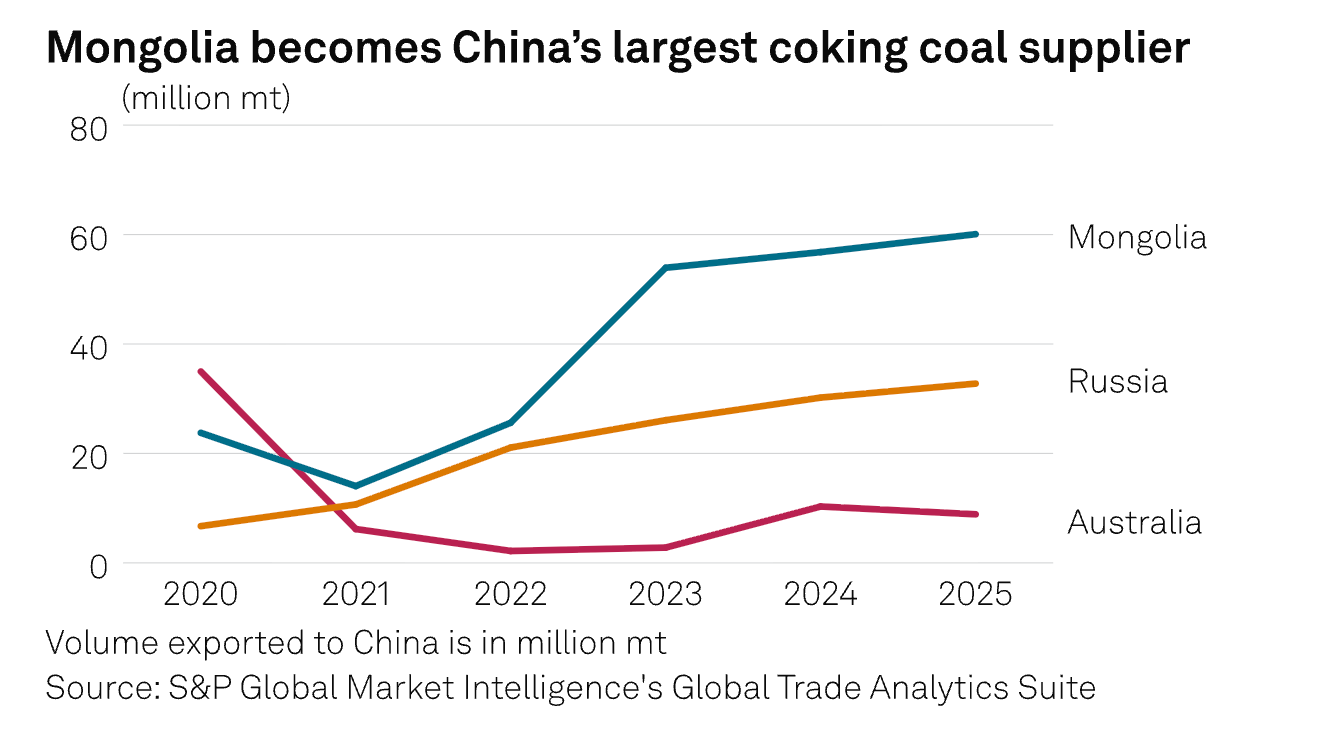

Mongolia is exporting record volumes, but it is landlocked and ships almost everything to China by land. It helps China, not the seaborne market. If you are a mill in India or Japan, a Mongolian tonne is not really available to you. And even that is fragile. Mongolian energy workers are now preparing a nationwide strike, a reminder that this supply rides on a narrow overland chain. Indonesia is growing fast too, but its coal is lower quality and held back by logistics and washing capacity. It fills the bottom of the market, not the premium gap.

5. Demand is moving from China to India

China’s steel output is falling, at a seven year low, yet its coking coal imports were up about twenty percent early this year. Lower steel, higher coal imports. The demand is shifting toward imported premium tonnes, not disappearing.

And the real growth has moved south, to India and Southeast Asia. India is the one I keep coming back to. It is expanding steel capacity in a big way and imports the overwhelming majority of its coking coal. That combination is becoming the most important demand story in the whole market.

6. Why I am bullish from 2028, and why everything depends on India

Now let me put it all together.

Start with supply. New seaborne supply is extremely hard to bring on, and most people underestimate just how hard. When a mine shuts down, the workers leave, the equipment gets sold, and the licenses expire. Restarting is far harder than it sounds. Banks will barely finance coal projects anymore. Skilled miners are hard to find and take years to train. New mining equipment can take years to be delivered. And in most Western countries, permits for coal are slow and political. Once a mine shuts, it stays shut.

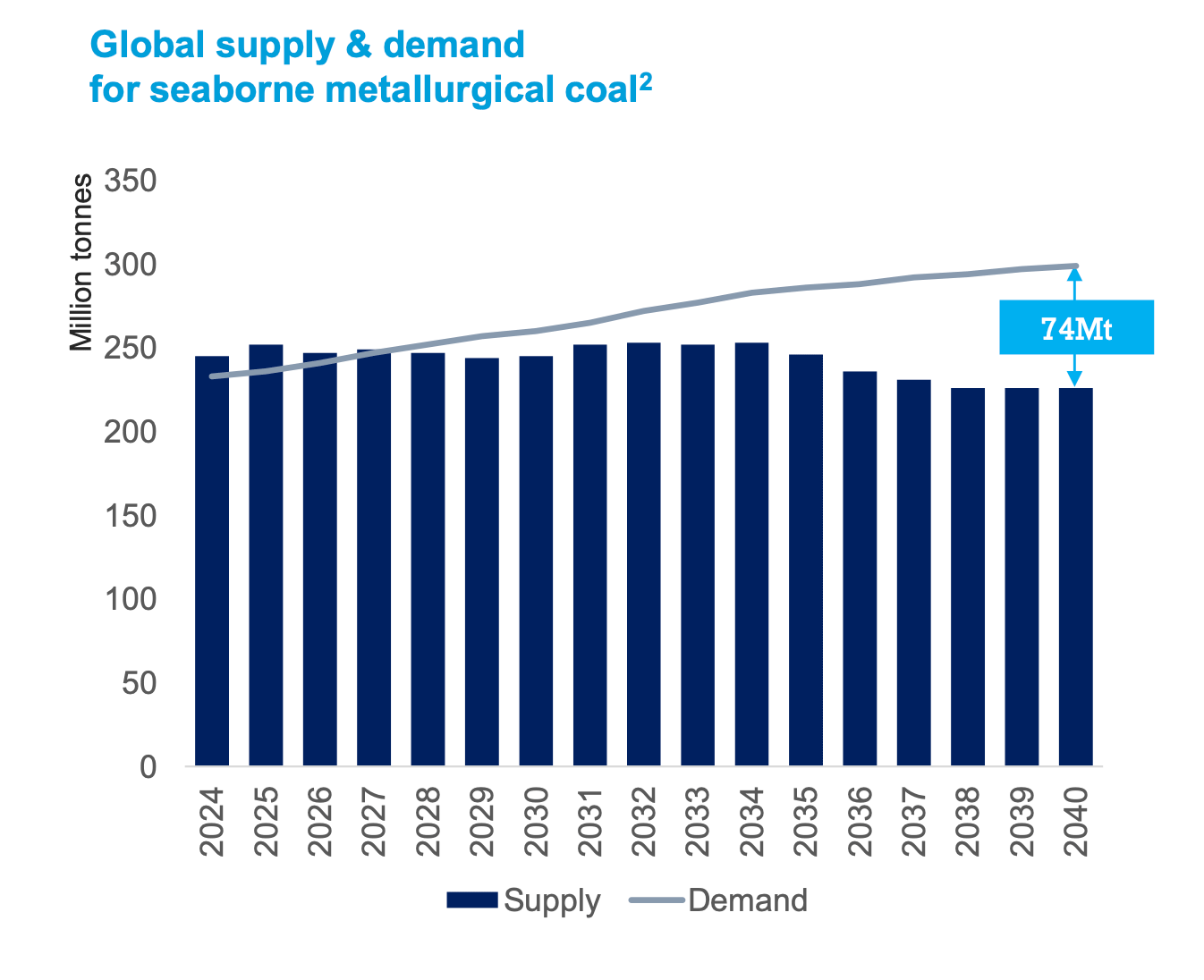

That is why global coal investment has fallen roughly two thirds since 2010, and why Wood Mackenzie sees a seaborne met coal supply gap opening as old reserves deplete and almost no new projects get approved. The supply side is not just tight today. It cannot respond for years, no matter what the price does. That is the foundation of why I am bullish on met coal, and specifically why I think 2028 and 2029 is when it shows up in earnest. Any new mine someone decided to build today would not produce a tonne before then anyway.

Now the demand side, and this is where India stops being a slogan and becomes a list of real furnaces.

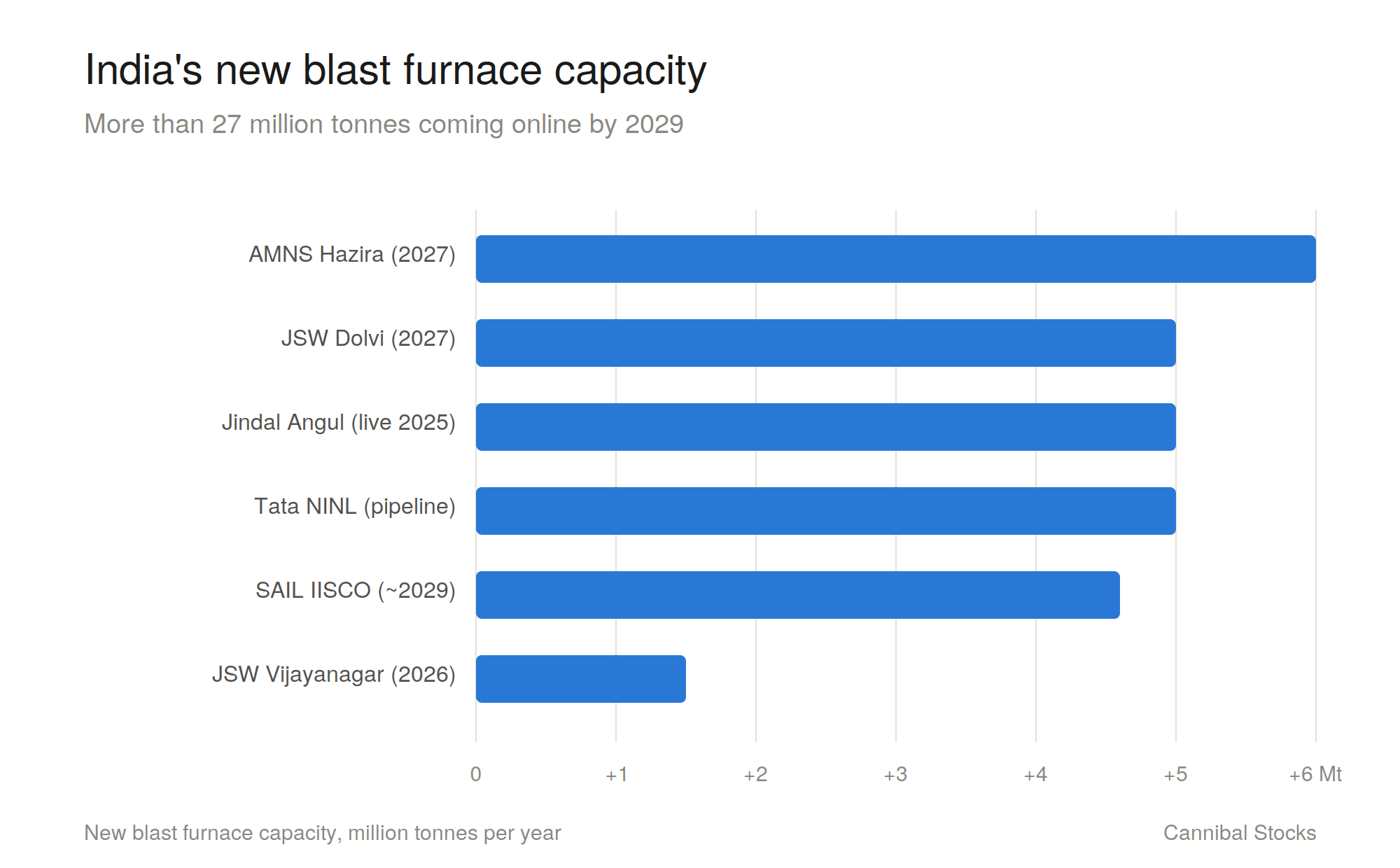

I checked the actual projects, because “India is growing” gets repeated so often it stops meaning anything. They are real and under construction. JSW commissioned a new 4.5 million tonne blast furnace at Vijayanagar and is upgrading another, taking that site toward nineteen million tonnes by late this fiscal year. At Dolvi it is going from ten to fifteen million tonnes with a new furnace by September 2027. AMNS India is taking Hazira from nine to fifteen million tonnes in the first half of 2027. SAIL has clearance for a new furnace that roughly triples its IISCO plant by around 2029. Jindal already doubled hot metal at Angul, commissioning one of India’s largest furnaces in late 2025. Tata is working on a five million tonne furnace at NINL. Add just the clearly executing projects and you get close to thirty million tonnes of new blast furnace capacity between now and 2029.

And the money is committed, not promised. The top four Indian steelmakers just announced a forty percent jump in capital spending for fiscal 2027, around 700 billion rupees. These furnaces are built to run for forty years, not to flex with one price cycle. In February 2026 it even got formal between governments, a US India joint statement where India committed to 500 billion dollars of US energy products over five years, with coking coal named explicitly.

India imports roughly ninety percent of its metallurgical coal, because its own coal is too high in ash to make steel at scale. That dependence is permanent, not temporary. S&P sees India’s met coal imports rising toward 100 million tonnes by 2030. In 2024, India became the single largest destination for US metallurgical coal exports for the first time in history.

So put the two halves side by side. Demand from India is growing on a forty year timeline with committed capital behind it. Supply cannot respond for years even if prices double, because the mines that closed are not coming back and new ones take the better part of a decade. Every furnace India lights is a furnace that will need imported coal for four decades, and the world has quietly stopped building the mines to feed it.

That gap does not close politely. Somewhere around 2028 or 2029, the furnaces will be running and the new tonnes will not exist. That is the setup, and almost nobody is positioned for it.

One last thing

Most investors will read all of this and think what they have always thought. Higher prices will fix it. That is how commodities have always worked. Every boom brings a wave of new supply, the glut arrives, prices crash, repeat. It has happened so many times that people treat it as a law of nature.

This time, in a handful of markets, that law is quietly broken. Not because producers do not want to respond, but because they cannot. The capital will not come, the people are gone, the permits take a decade, and nobody builds a forty year asset for an industry the world has declared dead. It is true in uranium. It is true for rare earth producers. It is true in offshore drilling, especially ultra deepwater. It is true even in DRAM, where higher prices have not produced the flood of new supply that markets have come to expect. And it is true in met coal.

The supply response that everyone is waiting for is not coming. And markets that assume it is coming are mispricing the ones where it is not.

The accident in China was the spark. India is the fire. And this time, there is no fire brigade.

Cheers, Sandro