TAV Airports (TAVHL). They Bought an Airport With Zero Passengers. Then a Mob Stormed It.

The first serious English deep dive on the company where Mohnish Pabrai owns more than 5 percent and refuses to sell

On January 5, 2022, men with weapons broke through the fences of Almaty International Airport.

They took the terminal in minutes. Flights stopped. Passengers ran. The biggest airport in Central Asia belonged to the street. In Istanbul, the executives who had just made the largest purchase of their lives watched the news come in.

They had owned that airport for nine months.

They bought it during the pandemic, when it had almost no passengers. Now it had too many. Armed ones.

Any sane investor would call this the worst deal in aviation history. I am going to show you why it might be the best one of the decade. Why Mohnish Pabrai built a position above 5 percent of this company and refuses to sell while the stock bleeds 30 percent in dollars. And why every dollar spent in that terminal is making his investors richer.

Nobody has written a serious analysis of TAV Airports in English. You are reading the first one. And at the end I will do something no newsletter does. I will grade the company and grade the investment separately, and the two grades are not the same.

The word that changes everything

First you need to understand one word. Because this word is the entire thesis.

Almost every privatized airport on Earth works the same way. The government gives you a concession. Build, operate, transfer. You run the airport for 25 or 30 years. You pay for the privilege. And when the clock runs out, you hand the keys back and walk away with nothing.

You are a tenant. A well paid tenant. But a tenant.

Out of every airport on the planet, only 3 percent are privately operated at all. And of those, almost none are actually owned.

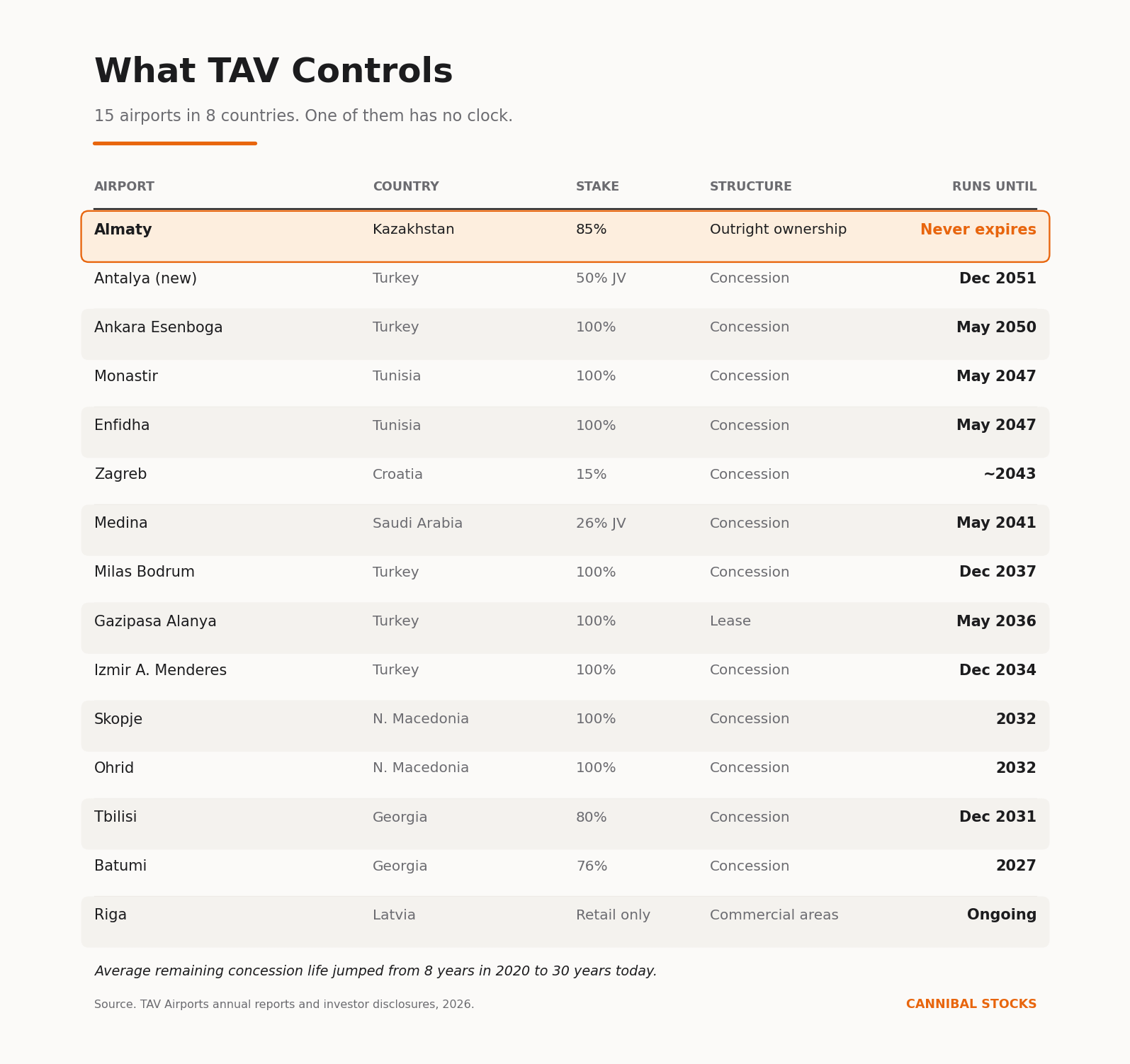

Almaty is owned.

When TAV closed the deal in April 2021, they did not sign a concession. They bought the airport. The runways. The terminal. The land. No expiry date. No transfer clause. Their CEO does not have to think about what happens in 2047 because nothing happens in 2047.

The price was 365 million dollars.

Hold that number. At the end of this post I will show you a return calculation I checked three times, because on today’s price the result looked too clean to be true.

Here is what TAV controls today.

Why nobody outbid them

In 2020, Almaty Airport handled 3.6 million passengers. A year earlier it handled 6.4 million. The business had been cut in half by a virus and nobody knew if flying would ever come back.

The infrastructure funds that fight over airports in London and Sydney did not even show up. Who buys an airport with empty runways? Who buys anything in Kazakhstan while the world hides at home?

Pabrai has a line for this. He says investing in these situations is like playing bridge against people who have been told it does no good to look at the cards.

TAV looked at the cards. The cards said Kazakhstan is a landlocked country the size of Western Europe. The cards said Almaty is its front door. The cards said passengers come back after every crisis in aviation history, and monopolies do not stop being monopolies because of a bad year. So while the world was frozen, a Turkish operator bought the front door of Central Asia for less than the price of a single wide body aircraft.

Then the mob came. TAV got the terminal back in one day, patched the damage, and kept building. Riots, then a war starting next door in Ukraine.

They never stopped construction.

A traveler buys a $100 bottle at the airport

Now let me show you what they actually bought. Forget passenger counts for a second. Follow one bottle of perfume.

Pabrai explains the economics with a simplified 100 dollar duty-free purchase. The product itself costs roughly 30 dollars at the factory gate. The airport operator can collect around 40 dollars as rent for the retail space. What remains pays for inventory, staff, utilities and logistics, leaving the duty-free operator with a much smaller profit.

At Almaty, TAV participates on both sides. The airport vehicle, in which TAV owns 85 percent, collects the rent. ATÜ, the duty-free operator, is 50 percent owned by TAV. Not every dollar reaches TAV shareholders, but the company earns from both the floor beneath the shop and part of the business operating on top of it.

Look at the structure again. The brand manufactures the product. The retailer stocks and sells it. The airport owns the scarce piece of floor that every international passenger must walk past. That floor can earn more than either of the businesses doing the visible work.

Pabrai estimates that an average international flight produces roughly 1,500 dollars of duty-free sales and about 600 dollars of rent for the airport operator. Scale that across thousands of flights, then add passenger fees, ground handling, catering, lounges and parking. In 2025, the group served 113 million passengers. An airport is a toll booth where the cars line up voluntarily and buy perfume while they wait.

The pettiest revenge in aviation

Here is my favorite part. It tells you more about this management team than any annual report.

When TAV took the keys in Almaty, they discovered something absurd. Years earlier, someone had sold the duty free retail space inside the terminal. Not leased. Sold. The shopkeepers owned their square meters inside a building that now belonged to TAV.

TAV owned the airport and earned zero from duty free inside its own terminal. They went to the owners and asked to buy the space back. The owners named a fantasy price. They thought they had TAV trapped. Where else do the passengers go?

TAV said fine. Keep it.

Then they spent 270 million dollars building a brand new international terminal next door. It opened in June 2024. Capacity doubled to 14 million passengers. And on opening day, every international flight moved to the new building. Every international passenger. Every dollar of duty free spending. All of it now flows through 3,400 square meters of shops run by TAV’s own duty free arm.

The old owners still own their space. In what is now a domestic terminal. Where nobody buys hundred dollar perfume. Their monopoly evaporated in one morning, legally, without a single lawsuit.

That is who is running this company.

Built by losing everything twice

This ruthlessness was not learned in business school. It was beaten into them.

TAV was born in 1997 to build the international terminal of Istanbul Ataturk, and Ataturk became its crown jewel. In 2016 a terrorist attack hit that terminal. In 2019 the government moved all traffic to the new Istanbul mega airport and TAV lost its flagship overnight. Compensation and a 49 percent stake in the Sabiha Gokcen operator kept them alive. A year later the pandemic took traffic to zero everywhere at once.

A bombing, the loss of the crown jewel, a global shutdown, an armed mob. Four near death experiences in five years. The response to the last two was to buy Almaty at the bottom and outbid everyone for Antalya through 2051. Capitalism destroys businesses every day. The few that survive are impressive. The ones that use every crisis to become even stronger are exceptionally rare. TAV belongs in that category.

The employee discount called hyperinflation

TAV is listed in Istanbul, and the moment investors hear the word Turkey they close the tab. Lira down more than 80 percent in five years. Inflation that touched 85 percent. Why would anyone go near it?

Because TAV is built backwards, and backwards is exactly right.

Around 75 percent of its revenue arrives in euros and dollars. Passenger fees at its Turkish airports are set in euros. Duty free is hard currency. Almaty charges in dollars. Meanwhile the costs, mostly thousands of salaries, are paid in lira.

So revenue is denominated in currencies that hold. Costs are denominated in a currency that melts. Every year the lira falls, TAV’s workforce gets cheaper in real terms while the toll booth keeps charging in euros. For a normal Turkish company inflation is a death sentence. For TAV it is a permanent discount on labor.

So why is the stock down 30 percent

If this machine is so good, why has it lost a third of its dollar value in two years?

Ask the market and it points at the map. Iran. Israel. Missiles near Turkish routes. War zone, avoid.

Pabrai argues that the three largest structural headwinds have little to do with Iran. Management is more cautious. It acknowledged that geopolitical disruption hurt the first quarter of 2026. Both can be true. War affects traffic today, while the constraints Pabrai describes determine how much traffic TAV can handle when conditions normalize.

Here were his three answers.

One. The planes are in the repair shop. The passengers are there. The demand is there. The planes cannot fly until the engines are fixed. The backlog clears through 2027. Two. Boeing cannot build fast enough. Airlines want to grow. The planes are still in the factory. The delivery queue is finally moving. Three. Kazakhstan took the fuel business. A real loss. But in return, the government is backing higher passenger fees. TAV traded a business the state was likely to reclaim anyway for pricing power that compounds for decades.

Grounded planes fly again. Queues move. Fees compound for decades. The market has taken three problems with deadlines and priced them like a diagnosis.

Meanwhile the business printed records. Revenue up 10 percent to 2 billion dollars in 2025. EBITDA up 14 percent to 600 million dollars, above the pre pandemic peak. Free cash flow up 44 percent. Debt falling.

A price dropping.

You buy one airport. Fourteen come free.

The equity trades on the Istanbul exchange for about 2 billion dollars.

Now ask a different question. Not what TAV paid for Almaty, but what it would cost to build it today. TAV paid 365 million dollars for the airport and poured roughly another half billion into the new terminal and the projects around it. Try to replicate that from scratch. Industry cost guides put a new international hub for 10 to 15 million annual passengers at 8 to 14 billion dollars. And that buys you concrete, not a monopoly with cargo, rail links and forty years of operating know how already inside.

So the replacement value of Almaty alone is a multiple of what the whole company costs on the Istanbul exchange. The market is selling you the entire fifteen airport company for less than the cost of rebuilding one of them.

Now forget replacement value and count only cash. Almaty ramps toward 110 million dollars of EBITDA a year by 2030 as fees rise and duty free flows into TAV's own hands. Add up the next 15 years and this one airport alone throws off roughly 2 billion dollars of EBITDA, close to the entire equity value of the company. One airport covers what the market is charging for all fifteen.

And then it keeps going, because Almaty is owned, not leased. Year 16 looks like year 15. So does year 50.

Which means the trade on the table is this. You pay about 2 billion dollars for the equity. One asset covers the ticket. And stapled to it come 14 other airports. Antalya, the busiest leisure airport in the Mediterranean, locked until 2051 in a country that just set a tourism record of 64 million visitors. Ankara until 2050. Georgia, Macedonia, Tunisia, Medina, Riga. A management team with a proven ability to win concessions and compound value. Over 100 million passengers a year, priced at zero.

I tried to kill this thesis

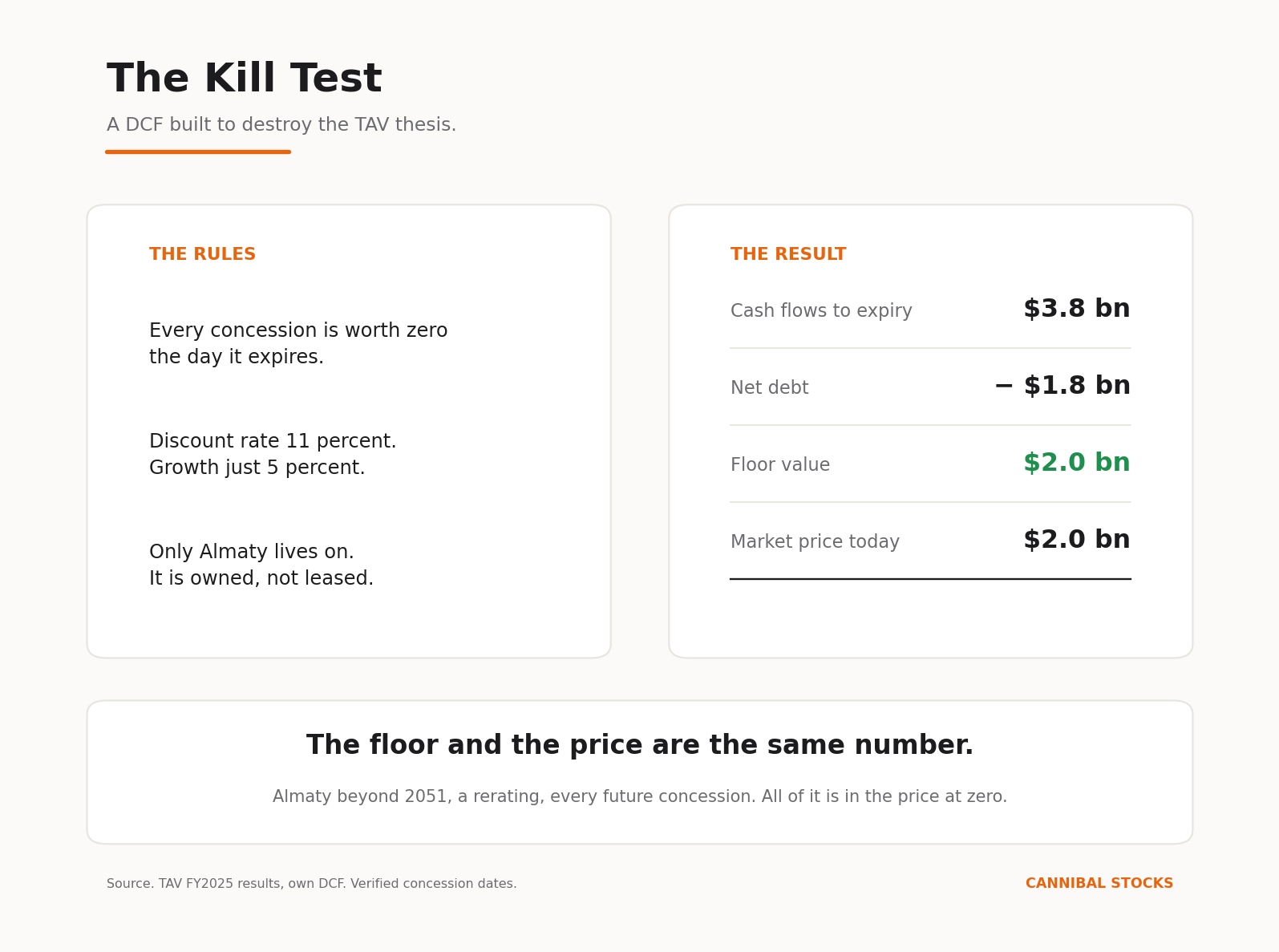

I do not trust stories, not even my own. So I built the most hostile DCF I could design and pointed it at TAV.

The rules were simple and cruel. Every concession is worth zero the day it expires, as if the buildings burn down with the keys. Antalya's payments to the Turkish state, more than 110 million dollars a year, come off the top. Discount rate 11 percent. Growth just 5 percent. Only Almaty, the one airport that is actually owned, lives past its horizon.

The result. The cash flows to expiry, minus roughly 1.8 billion dollars of net debt, are worth almost exactly what the equity costs today.

So the market is pricing TAV as if every concession dies on schedule and nothing ever replaces it. Almaty’s cash beyond 2051, which runs forever. The 3 to 5 billion a strategic buyer would pay for it. Any rerating toward peers at 10 to 13 times EBITDA. Every concession this team wins or extends over the next 25 years. All of it sits in the price at zero.

Most stocks fail this test catastrophically. TAV lands exactly on it. The price is the floor. Everything above the floor is a gift.

And the floor is not even the point. The point is what sits on top of it, paid for by nobody.

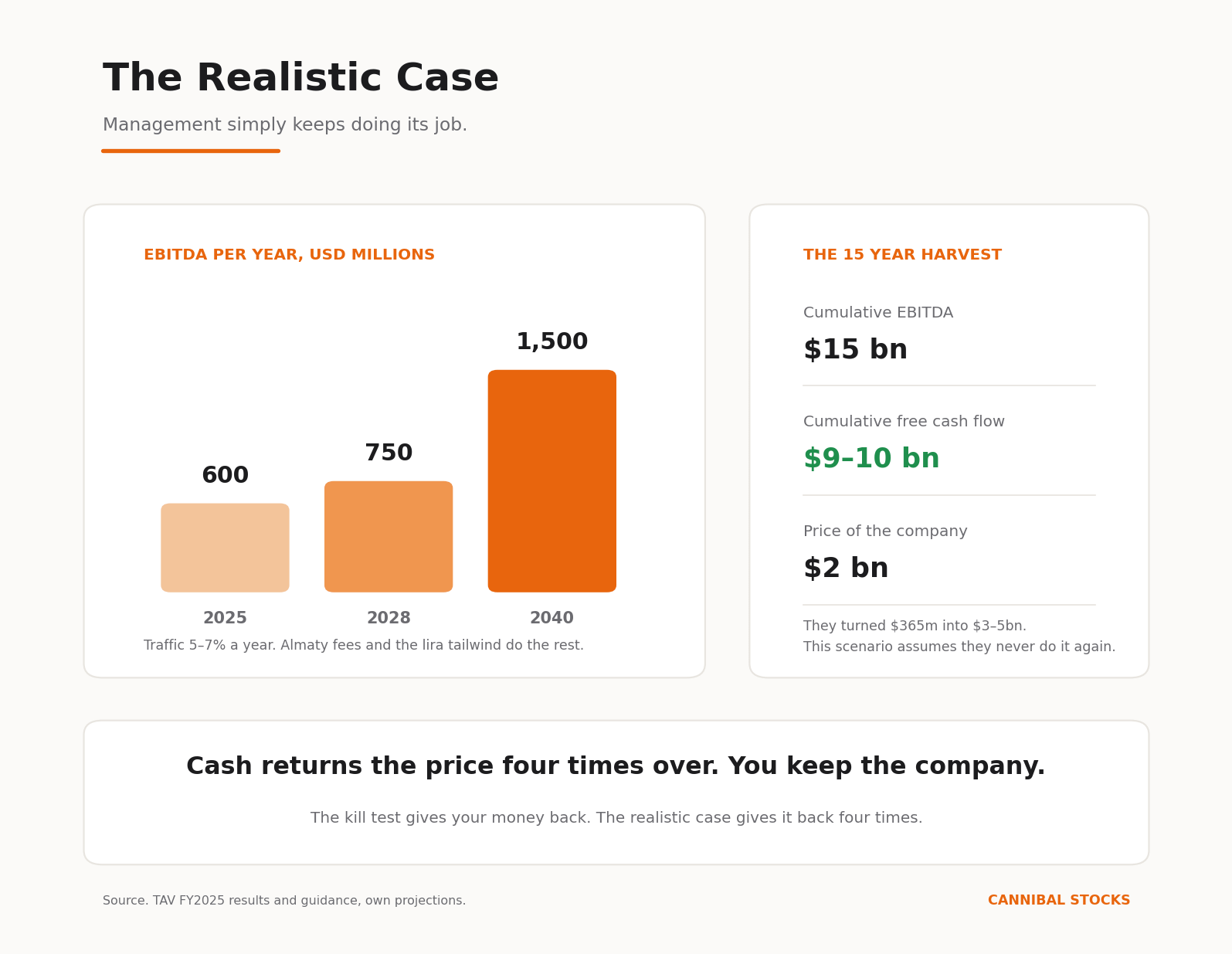

The realistic case

The kill test was deliberately unfair. It assumed this management team spends 25 years doing nothing. Now let me tell you what actually happens, moderately, without fantasy. This team has spent three decades doing exactly one thing, keeping airports and adding new ones.

So run the moderate scenario. EBITDA follows the path already in motion, 600 million dollars in 2025 toward 750 million by 2028, then grows 6 percent a year. Traffic gives 5 to 7. Almaty fees give more. Inflation keeps melting lira costs against euro revenue. Nothing in that 6 percent requires luck.

By 2040 the company earns around 1.5 billion dollars of EBITDA a year. Along the way it produces roughly 15 billion dollars of cumulative EBITDA and, once the construction decade ends and debt amortizes away, somewhere around 9 to 10 billion dollars of cumulative free cash flow to equity.

The moderate case, no miracles, no new countries, returns the equity value four times over in cash within 15 years, after the debt is served.

The kill test gives you your money back. The realistic case gives it back four times and hands you the company anyway.

And even the realistic case is pessimistic about one thing. This is a management team that turned 365 million dollars into an asset worth 3 to 5 billion in five years. My scenario assumes they never do anything like that again.

What kills it

I do not write fairy tales, so here is the other side.

Net debt is roughly 1.8 billion dollars. Falling, but a 2020 style traffic collapse would turn it into a noose. Governments change rules, and Kazakhstan just demonstrated it with fuel. Groupe ADP of Paris holds 46 percent and controls the board, so minorities ride in the back seat of a French car. Turkish assets carry a permanent fear discount that can widen in any panic no matter how well the business performs.

And there is the winner’s curse. TAV and Fraport committed 7.8 billion dollars for the new Antalya concession, roughly 2 billion upfront and fixed installments until 2051. The state took its share upfront. The operator earns its return only if Turkish tourism grows for 25 years. A lost decade means they overpaid.

You are paid well for carrying these risks. But you are carrying them.

Why this belongs on Cannibal Stocks

One honest note. This newsletter hunts companies that eat their own shares, and TAV does not buy back stock. It pays dividends, half of profits starting now. The amount is small today because net income is buried under the depreciation of three brand new terminals. The payout ratio is fixed. The income is not. Turkish companies rarely repurchase shares at all.

So why write it? Because the cannibal thesis was never really about buybacks. It was about management teams that allocate capital like owners. Buying the front door of Central Asia at the bottom of a pandemic, for a price one competitive round of bidding would have doubled, did more for shareholders than any buyback in the history of Borsa Istanbul. This is the same discipline wearing a different suit.

My honest scorecard

Before the ending, let me drop the storyteller voice and tell you exactly where I land.

The company gets 7.5 out of 10. The monopoly is real, the currency machine is real, and this management team passed tests that kill normal companies. But net income in 2025 was only 55 million dollars on 2 billion of revenue, because the machine still feeds banks and governments before it feeds shareholders. The Antalya obligation of 7.8 billion dollars is a 25 year bet that Turkish tourism never has a lost decade. And Kazakhstan just reminded everyone that a state takes what it wants when it wants. TAV is a very good company in a rough neighborhood, and the neighborhood is part of the price.

The investment at today’s price gets 8 out of 10. The downside is the strongest part, the kill test showed that cash alone covers the ticket and permanent loss requires a traffic collapse and a debt crisis arriving together. The upside is roughly a double in three years if EBITDA simply follows its guided path, and more if the multiple ever moves from 7 toward the 10 to 13 its peers command.

Why not a 9 or a 10. Because part of the upside depends on a rerating that may never arrive. Turkish stocks can stay cheap for a decade, and a value trap does not announce itself, it just wastes your years. And because a temporary 30 or 40 percent drawdown in some emerging market panic is not a risk here, it is practically a promise, and you have to be able to sit through it without blinking.

So the honest summary is this. The downside protects you. The upside makes you wait. The biggest real risk is not Turkey and not war, it is that you spend five years waiting for a rerating that arrives in year ten.

This story isn’t finished.

Everything above came from filings and spreadsheets. But a spreadsheet can’t count the passengers, or tell you if the duty-free queue is real. So I’m doing something I’ve never done here.

I’m flying to Turkey.

To stand in these terminals myself, count the crowds, and watch the tills move — reporting live from the airports, straight into the subscriber chat. Raw notes from the field, as it happens. And when I land, paid subscribers get the one thing no filing can give you: my decision. Whether I’m buying, how big, and the exact price I’ll pay.

The research doesn't end here. It starts when I land.

Come along.

The mob knew

Think back to January 2022 one last time.

Thousands of people rose up in Almaty that week. They could have stormed anything. The parliament. The banks. The television station.

They took the airport.

Because everyone in that city understood what the most valuable thing in Kazakhstan was. The mob knew it. The government that sent soldiers to take it back within a day knew it. The Turks who bought it while the world hid at home knew it. Pabrai, sitting on a twentieth of the company, knows it.

The only ones who still do not know are the people setting the price in Istanbul.

They will.

Cheers, Sandro

Like and Restack. The airport isn’t the only thing that needs traffic.😂