Valaris (VAL): The Biggest Asymmetric Opportunity of the Next 5 Years

Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble.

Every now and then, the market gives us a gift. After bankruptcy, a company is left for dead. The scars are deep, but the balance sheet is clean. Debt is gone. Equity holders own the business free of the old burden.

These companies often trade at a fraction of what their assets are worth. But nobody wants them. They are ignored, unloved, and left behind. And that is exactly why the opportunity exists. What matters is not the past, but the future. And in this case, the future looks very different.

A Business That Would Cost ~$30B to Rebuild, Trading for Just $3B

"When you find a mispriced bet with a big upside and very little downside, you should bet heavily. It’s not often that you get a chance like that."- Charlie Munger

As I’ve already discussed in my free Substack, the company in question is Valaris (NYSE: VAL). Now it’s time to go deeper and explain why there are really two main scenarios for this stock over the next five years.

Either it re-rates closer to its replacement value — and delivers a clean 10x return — or it stays depressed, which paradoxically could create even more extraordinary upside through buybacks. Allow me to explain.

A Short Reminder

Offshore drilling means using massive floating rigs to extract oil and gas from deepwater fields. For decades, offshore was king — supplying roughly one-third of global oil production.

But in the last decade, it became a case study in how investor dreams can unwind. Oil was above $100; companies ordered rigs worth up to $1 billion each, financed with heavy debt. Then U.S. shale exploded — cheaper, faster, more flexible. Oil prices fell. Offshore projects became uneconomical overnight. Billions worth of rigs sat idle, crews were fired, and dayrates slipped below operating costs.

When COVID hit, demand for oil collapsed, prices briefly went negative, and the sector went through a brutal reset. Ensco had merged with Rowan in 2019 and rebranded as Valaris. Valaris filed for Chapter 11 in August 2020 and emerged in May 2021 — leaner, deleveraged, and with a fresh balance sheet.

Why This Time Is Different

First, Valaris has a backlog of about $4.7B (July 2025). That is contracted work — revenue already secured.

For comparison, current annual revenue is about $2.3 billion. So the backlog is nearly twice today’s revenue. That gives me confidence that business and cash flow are secured for the coming years. On the downside, it also means the room for loss is minimal: revenues are locked in, the fleet is active, and yet the valuation remains absurdly low.

Many believe oil and gas are in structural decline, but the reality is that offshore still supplies roughly one-third of global oil production — and starting in 2026, offshore activity is projected to step up significantly. Industry data suggest floater demand will be about 13% higher in 2026–2028 vs. 2024–2025, while subsea installations could rise more than 20%.

Second, demand is rising while no newbuild cycle is underway. A modern drillship costs ~$850m–$1B and takes 3–5 years to build. After the bankruptcies of the last cycle, no offshore driller is willing to take on that kind of risk, and no bank is willing to finance it. On top of that, there is currently no shipyard in the world building new offshore rigs. In other words, for at least the next five years, the supply of rigs is effectively fixed. The result is structural scarcity.

Third, the stock remains unloved: many funds and endowments have mandates or ESG restrictions that prevent them from investing in offshore. That leaves Valaris overlooked and undervalued — exactly where asymmetric opportunities usually hide.

Finally, book values were reset through Chapter 11 and do not reflect replacement cost. The focus should always be on free cash flow, but it is telling that Valaris controls assets that would cost tens of billions to rebuild, while its market cap is only ~$3–3.5B.

How Much Cash This Company Can Generate

The key question is not the balance sheet — it’s the cash. How much free cash flow (FCF) can Valaris generate through the cycle?

Based on the company’s sensitivity analysis, depending on dayrates and utilization, annual FCF could range from a few hundred million dollars to ~$2B in a strong cycle. Illustrative:

$400k/day @ 70% util. → ~$0.3–0.5B FCF

$500k/day @ 80% util. → ~$1.0–1.2B FCF

$600k/day @ 85% util. → ~$1.6–2.0B FCF

For perspective: Valaris’ market cap today is only about $3–3.5B. In a strong upcycle, the company could generate a significant portion of its market value in free cash flow in just one year.

Most importantly, management has been explicit: they intend to return essentially all FCF to shareholders, primarily through aggressive buybacks.

In the last offshore bull market (2007–2008), Ensco was earning nearly $1B of net income per year — with a smaller fleet and before modern drillships even entered service. Today, the assets are larger, dayrates are rising, and the cycle setup is even tighter.

Dayrates & Market Dynamics

Valaris’ average drillship dayrates have risen from $288k in Q3 2023 to ~$410k in Q2 2025. With supply capped and demand tightening, it is reasonable to expect new contracts to move toward $500–600k/day — or higher.

Two dynamics are driving this cycle:

Floaters: demand projected to be ~13% higher in 2026–2028 vs. 2024–2025, with no newbuilds.

Deepwater: industry estimates suggest sustained growth as investment in deep and ultra-deepwater projects accelerates.

Valaris controls one of the largest and most modern fleets in the world. In addition, it has three drillships scheduled to return to work starting in 2026 — premium assets entering the market just as conditions tighten further. From 2026 to 2030, one thing looks very likely: no new rigs will be delivered to the market. This sets up structurally higher dayrates.

The Only Two Scenarios Ahead

Base case: ~$1.0–1.2B annual FCF (at ~$500k/day, ~80% utilization).

Upside case: ~$1.6–2.0B annual FCF (at ~$600k/day, ~85% utilization).

In a single strong year of the cycle, Valaris could generate nearly its entire market cap in FCF — and over 2026–2030, potentially return multiples of its current valuation directly to shareholders through buybacks.

1) Re-Rating Scenario

If the market re-rates Valaris closer to its ~$30B replacement value, with around $2B in annual FCF once dayrates move higher, even a conservative P/E of 15 would justify a ~$30B valuation — about 10x from today’s levels.

2) No Re-Rating Scenario

If stigma persists and the stock continues to trade at a depressed $3–4B market cap, with ~$2B of annual FCF possible from 2026–2030, Valaris could repurchase a very large portion of its outstanding shares within just a few years. That dynamic creates the potential for outsized, multi-bagger returns even without a re-rating — simply through the math of buybacks.

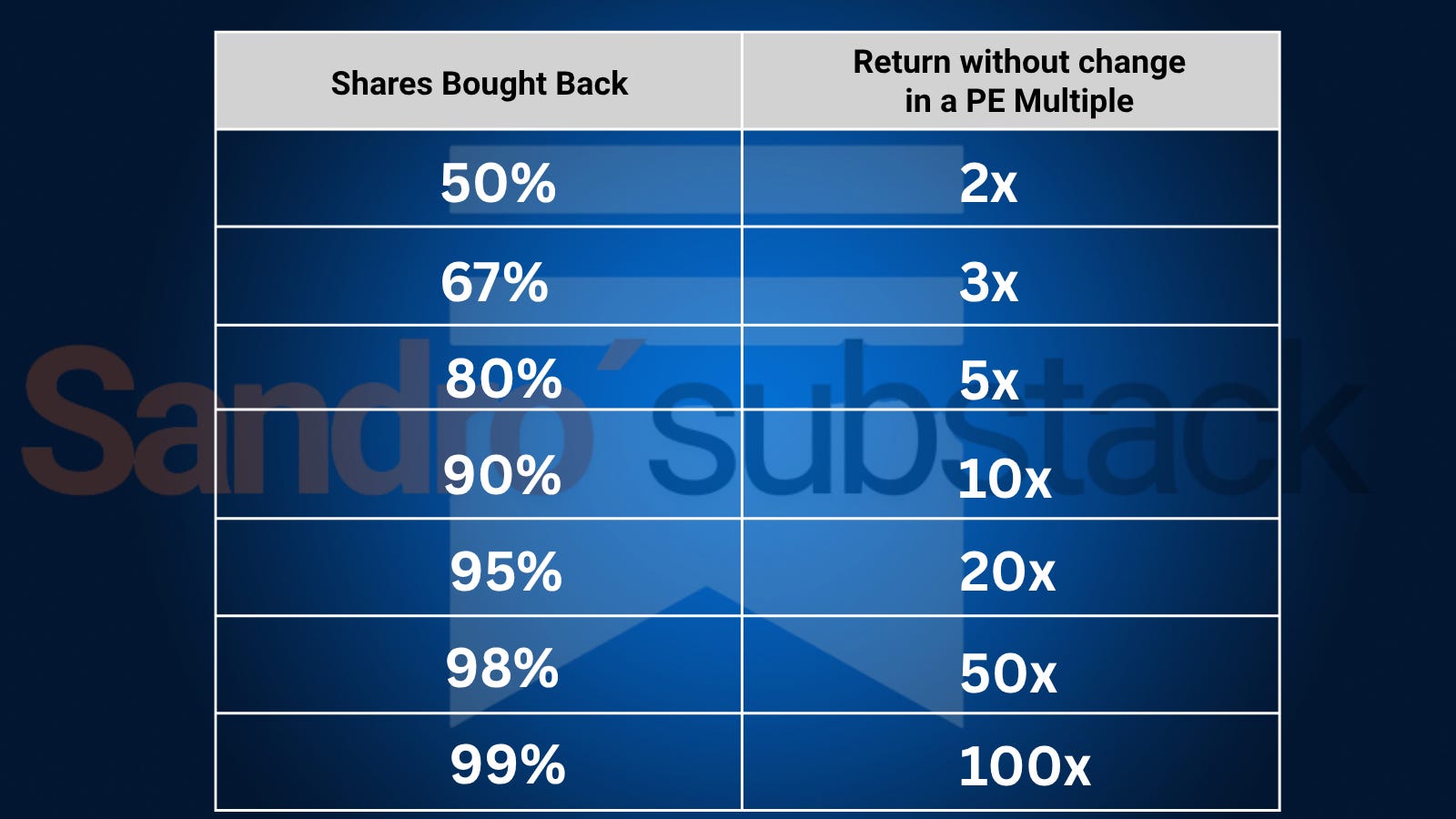

How Buybacks Work

The chart above shows the math of buybacks. Up to around 50% of shares repurchased, the effect is limited. But once buybacks move beyond that threshold — especially above 90% — returns start to accelerate exponentially.

In other words, the longer the stock stays unloved, the more powerful the outcome becomes for shareholders. Either the stock eventually re-rates 10x and investors enjoy the ride — or the price stays depressed and buyback cannibalism compounds the value even faster. Personally, I lean toward the second scenario.

"And the wise ones bet heavily when the world offers them that opportunity. They bet big when they have the odds. And the rest of the time, they don't. It's just that simple." - Charlie Munger

Cheers,

Sandro

Sandro. Very well written