Transocean (RIG) Bull Case: Why Offshore Drilling Bears May Be Wrong

Transocean controls 40% of the world's deepwater fleet. Full cash flow model, debt breakdown, and price targets inside.

“The time of maximum pessimism is the best time to buy.” - John Templeton

Note: This article is a bull case for Transocean. It lays out what I believe can happen if the offshore cycle plays out the way the supply picture suggests. It is not a balanced report — it is an optimistic scenario that depends on dayrates staying elevated, utilization remaining high, and the debt paydown proceeding as modeled. If those assumptions don’t hold, the equity outcome will look very different.

If you had asked any Wall Street analyst in 2020 which offshore drilling company would survive the decade, not a single one would have said Transocean.

And honestly? They would have had a point.

The shale revolution flipped the entire energy world upside down. Between 2010 and 2014 U.S. shale producers flooded the market with cheap onshore oil. The question in everyone’s mind was why spend billions drilling miles below the ocean floor when you can frack a well in Texas for a fraction of the cost?

Offshore was declared dead. The market acted like it.

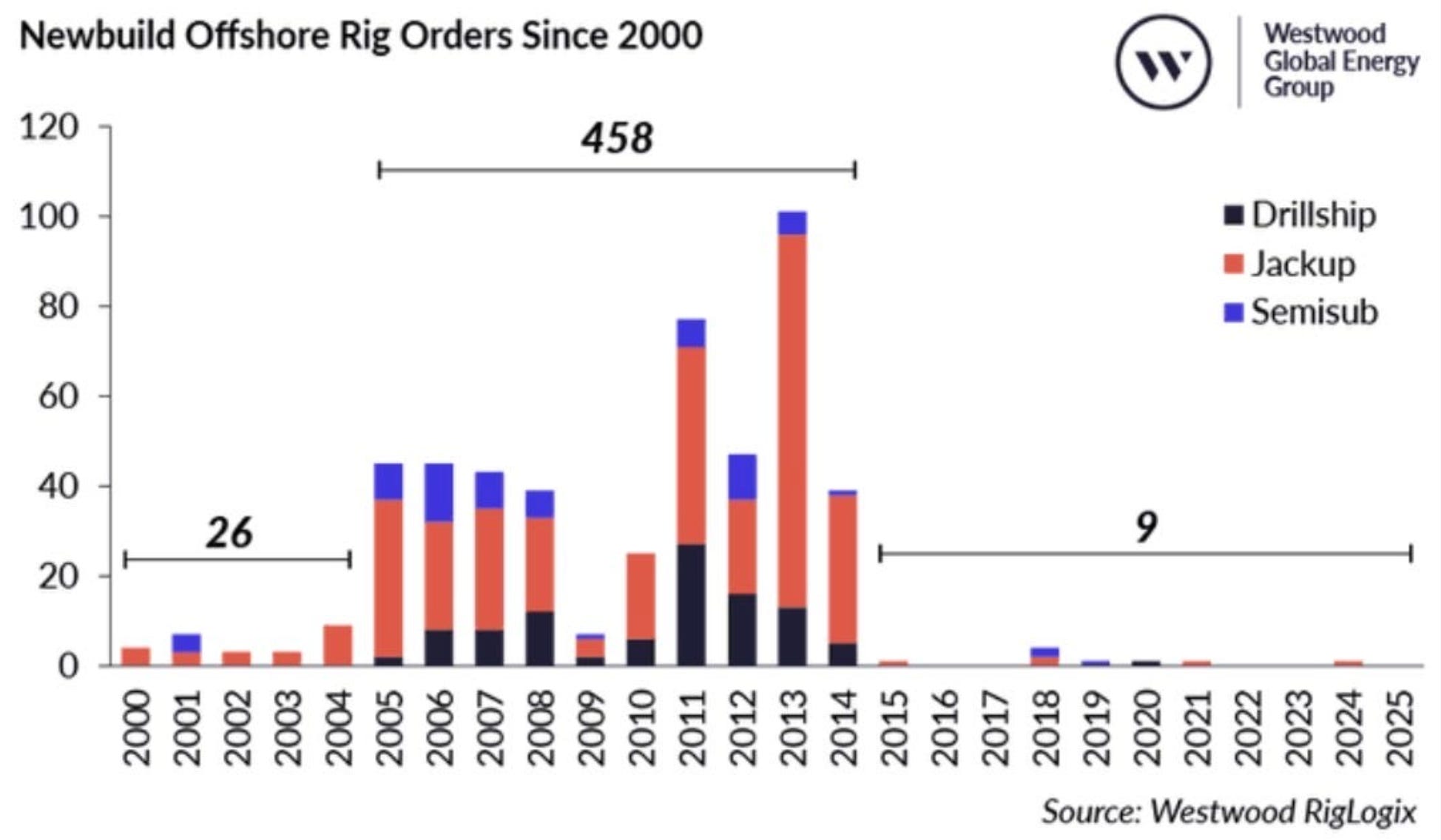

Oil crashed from $100 to $26 in 2016. Offshore drillers — who had ordered rigs like there was no tomorrow during the boom years (458 newbuild orders between 2005 and 2015 alone) — were sitting on massive overcapacity, crushing debt, and collapsing dayrates. The industry had the worst hangover in energy history.

Then came COVID. Oil went negative. Yes, negative. Producers were literally paying people to take their oil. For offshore drillers already on life support, this was the kill shot. One by one, the giants fell: Diamond Offshore, Noble Corporation, Valaris, Pacific Drilling, Seadrill — all filed for bankruptcy.

Every single one of them wiped out their shareholders and emerged with clean balance sheets. Every single one.

Except Transocean.

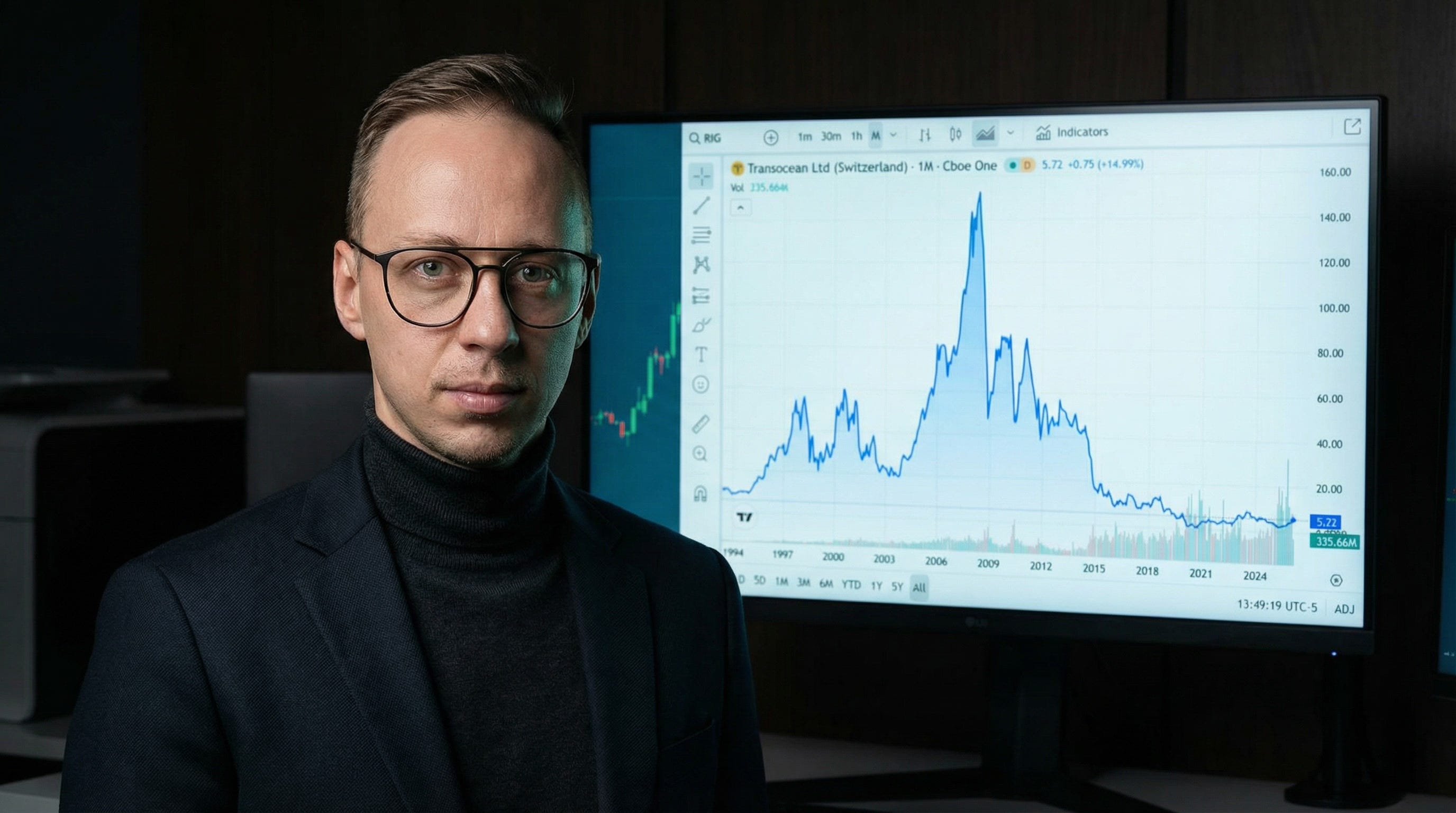

Transocean chose a different path. Instead of filing for bankruptcy and starting fresh, management decided to fight through it. They loaded up on debt to keep the company alive, to keep paying for their newbuild rigs, to bet everything on the cycle eventually turning. The stock went from $150 to under $2. Shareholders bled for years. The bears screamed that bankruptcy was inevitable.

But it never came.

Meanwhile, something remarkable happened on the supply side. After the catastrophic overbuild of 2005-2015, newbuild orders for ultra-deepwater rigs collapsed to zero. Not slowed down. Not pulled back. Zero. And they stayed at zero.

And into this tightening market, Transocean just made the most aggressive move in the offshore drilling history. They're acquiring Valaris in an all-stock deal, creating the largest deepwater drilling fleet on the planet.

Yes, it's dilutive. Yes, the share count is going up. I know, I know — that's the first thing everyone screams about.

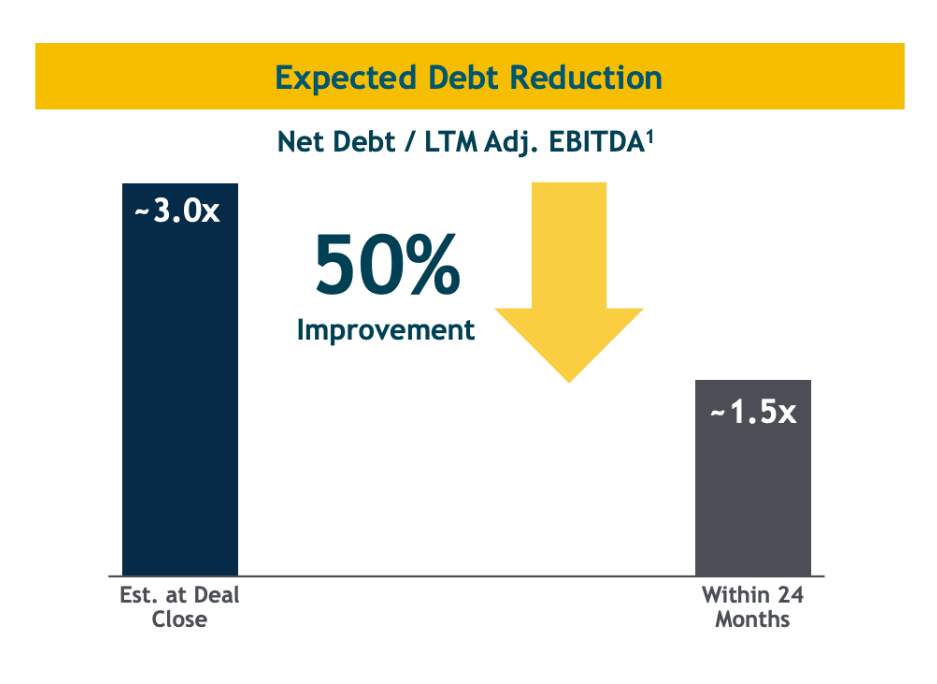

But with the combined backlog and fleet, Transocean is on track to bring net debt down to 1.5x EBITDA within 24 months of closing. The company that everyone thought would go bankrupt is about to have a balance sheet that most industrial companies would kill for.

As of September 2025, Transocean was carrying approximately $6.2 billion in total debt. Six point two billion. On a company whose market cap at times dipped below $3 billion. The bears had the math on their side.

I did a full breakdown of the debt in this post:

Valaris merger brings roughly $1.1 billion in debt. So yes, the combined debt rises to about $7.3 billion. Sounds terrifying, right? But Valaris also brings a massive cash-generating fleet and a combined contract backlog of approximately $10 billion.

$10 billion in backlog means locked-in revenue stretching years into the future. At industry-standard EBITDA margins of 45-55%, that’s $4.5 to $5.5 billion in EBITDA just from existing contracts. Add $200 million in annual synergies and $150 million in additional cost savings management has identified, and the cash flow machine becomes formidable. Over the next two to three years, the combined entity can generate enough free cash flow from its backlog alone to pay down the majority of the debt.

Debt is no longer the risk. The risk is being on the sidelines if this thing reprices.

So I sat down and built a full cash flow model for the combined Transocean + Valaris entity. I modeled the fleet, the dayrates, the backlog. The numbers surprised me. And I don’t say that lightly. This is the bull case for Transocean. And it might be the most important thing I've ever written on this Substack.