Transocean: The Debt Stress Test

Survival or Bankruptcy?

“It’s very hard to go bankrupt if you don’t have any debt.” — Peter Lynch

Transocean has about $6 billion of debt.

Its contracted backlog is roughly $6.7 billion. Cash on the balance sheet is $1 billion.

The only question is time. Can the backlog turn into cash before the maturity wall hits? This post is a stress test. Three variables decide the outcome. Cash generation from the rigs. The timing and size of debt maturities. And how much breathing room the calendar provides.

If Transocean clears the wall, the equity becomes a leveraged claim on a tightening market. If it does not, none of the dayrate narratives matter.

Let’s start with the clock.

What management actually did

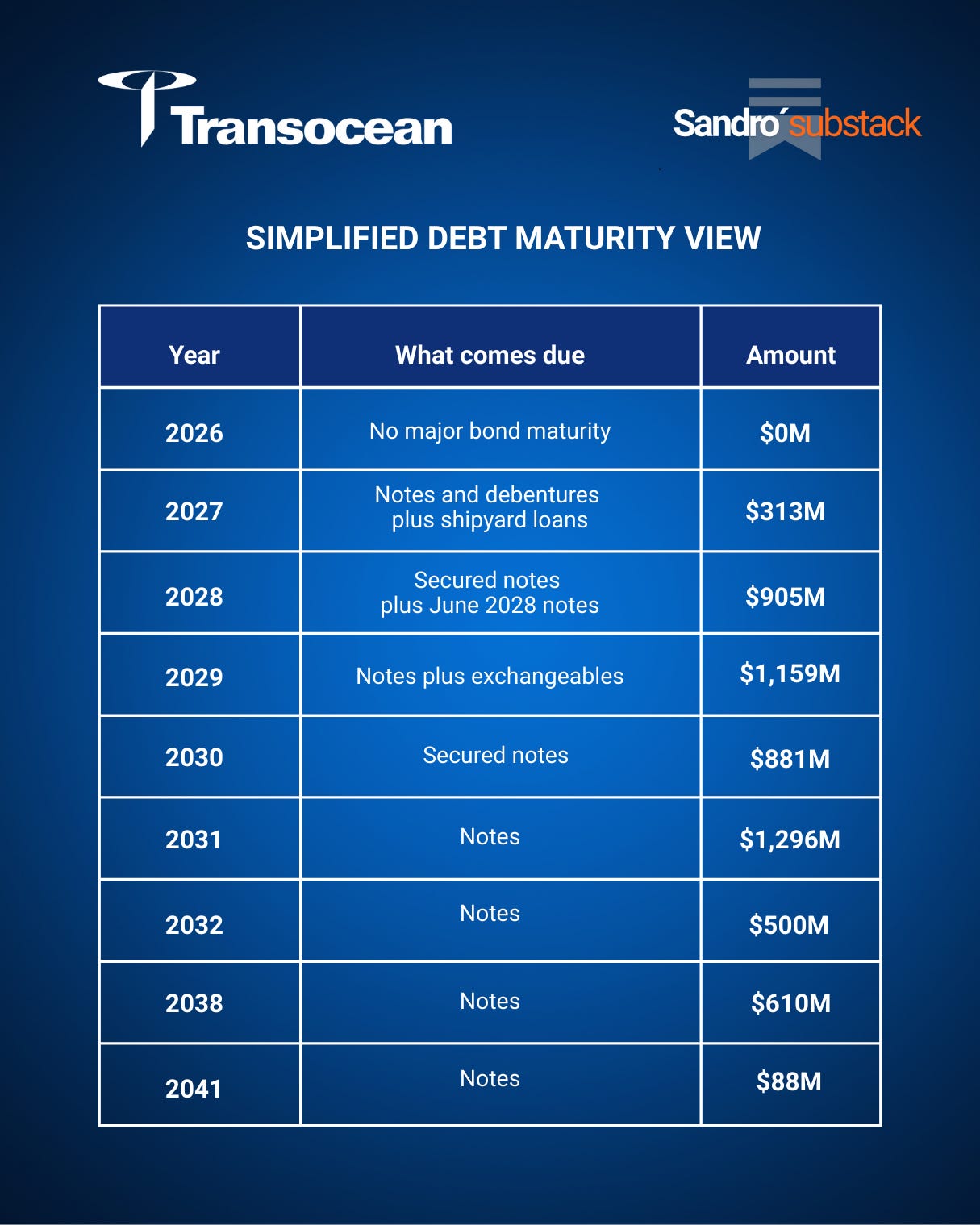

In October 2025, Transocean removed the February 2027 maturity, roughly $903 million. That was the real danger point. If that wall stayed in place, everything else in the story would be secondary.

At the same time, they retired small pieces of very long dated debt from 2028 and 2041. That part was not urgent. It was deliberate. Long dated notes sit in the background and remind the market that leverage never really goes away. Cleaning them up improves confidence and simplifies the structure.

To do this, they issued a new bond due in 2032. This pushed pressure further into the future and bought time for the backlog to turn into cash.

This chart shows Transocean’s debt maturities after the October 2025.

How the cash engine looks today

The fleet is working, so cash is showing up. There is no newbuild program. A new rig only makes sense with extreme economics. Think a million a day on a long contract. That market is not here.

Interest is still the main drain, but it is easing. Management points to roughly $480 million of cash interest in 2026, with a lower run rate after the 2025 refinancing. Low capex, a working fleet, and a smaller interest bill. That is the deleveraging setup.

Everything above explains why the story looks fine on the surface. Everything below is where it gets real.

I translate management’s 2026 framework into cash, then run the base case, the stress case, and the exact point where the debt calendar starts to control the equity.

This is where the stress test begins.