Warrior Met Coal: Fourth Quarter 2025 Earnings Results

The CEO is selling, the stock could fall, and Wall Street doesn't get it. Here's what they're missing.

To me, Warrior is what Saudi Aramco is to oil — but in the world of metallurgical coal.

When oil collapsed in 2020 and WTI briefly traded below zero, Aramco still generated $49 billion in net income. When you sit at the bottom of the global cost curve, the day-to-day price simply does not matter. Everyone else bleeds. You keep printing. Think about that for a second.

2025 was a bad year for met coal. A lot of mines lost money. Many are barely surviving. Warrior is not one of them. They sit deep in the first quartile of the cost curve. They run a tight, low-cost operation. And when Blue Creek reaches full capacity, they should move even lower on the curve — further away from everyone else.

That is why I see Warrior as one of the last players standing in a downturn. If the market gets truly ugly, they are the kind of company that keeps operating while higher-cost mines shut down around them. In a bad market, they survive. In a good market, they dominate.

They also have a logistics edge. Warrior can move coal by river barge as well as rail. If rail rates spike, they shift volume to the river. The Port of Mobile is close, and congestion in Alabama is lighter than most competing export routes. That keeps logistics costs down and makes seaborne exports significantly easier than for their peers.

Warrior Met Coal insider trades Q4 2025

In Q4 2025, based on primary Form 4 filings on the U.S. SEC EDGAR system, I found two filings covering three separate transactions in Warrior Met Coal common stock. All three were sales. Zero purchases.

In total, insiders sold 21,049 shares for approximately $1,592,678. That makes Q4 2025 net insider activity a clear net sale — both by share count and by dollar value.

The largest sale was by CEO Walter J. Scheller on November 6, 2025 — selling 18,966 shares at $75.00 for $1,422,450. This was executed under a Rule 10b5-1 plan adopted on November 8, 2023. Chief Accounting Officer Brian M. Chopin reported two smaller sales on November 12 and 13, totaling 2,083 shares at prices around $81.56 to $81.70. Both were also under a pre-arranged 10b5-1 plan.

Fourth Quarter and Full Year 2025 Results

This is what Warrior looks like in a bad year.

The Blue Creek longwall started eight months ahead of schedule and on budget. In Q4 alone, Warrior sold 881 thousand tons of steelmaking coal from Blue Creek and produced 1.3 million tons. That is a transformational mine delivering serious volume in its very first full quarter of longwall operations.

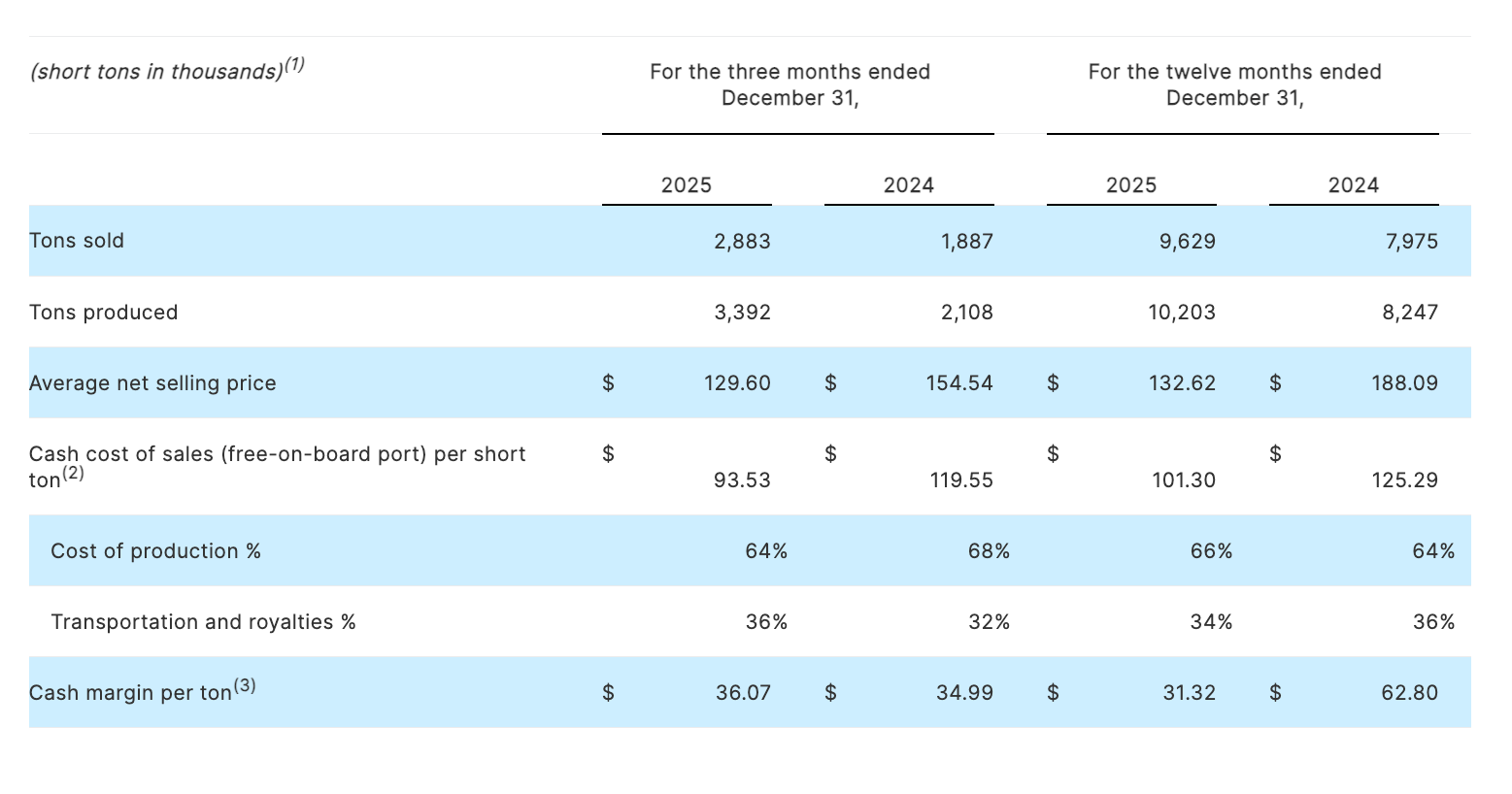

In Q4 2025 versus Q4 2024, sales volumes increased 53 percent to a record 2.9 million short tons. Production surged 61 percent to 3.4 million short tons. Cash cost per ton fell 22 percent — from $119.55 to $93.53. Read those numbers slowly. In a quarter when the market was punishing everyone, Warrior simultaneously grew production, grew sales, and crushed its cost structure.

This is the key point. In Q4 2025 compared to Q4 2024, the market was weaker — yet Warrior earned dramatically more.

The average net selling price fell 16 percent in Q4 — from $154.54 per ton to $129.60. For the full year, prices were down nearly 30 percent. The premium low-vol index itself dropped 22 percent year-over-year. In any normal business, that kind of pricing collapse would be devastating.

Q4 2025 net income was $23 million — compared to just $1.1 million in Q4 2024. That is a 20x increase. Adjusted EBITDA came in at $92.9 million versus $53.2 million a year ago — a 75 percent jump. Revenue rose 29 percent to $384 million, driven entirely by record volumes. All of this happened while prices were falling.

So in Q4, earnings increased while prices collapsed. Crazy.

Warrior is now firmly in the first quartile of the global cost curve. Q4 cash cost was $93.53 per ton. Full-year cash cost was $101.30 — better than guidance. That puts them among the lowest-cost met coal producers on the planet, and the cost trajectory is still improving as Blue Creek ramps further.

For the full year 2025, Warrior generated $57 million in net income and $256.5 million in Adjusted EBITDA — despite a 30 percent drop in average selling prices. Revenue was $1.3 billion with record production of 10.2 million short tons.

But the full-year numbers are blurred by heavy investment in Blue Creek. Capital expenditures totaled $402 million in 2025, including $240 million for Blue Creek alone. Almost all excess cash was reinvested into the mine buildout. What you are seeing is not Warrior's true earning power — it is Warrior's earning power minus a billion-dollar investment cycle that is nearly complete. Free cash flow was negative $173 million for the year, but that was entirely by design.

The more important numbers are structural. 2025 net income does not reflect the true earning power of this business going forward. It reflects a company in the final stages of a massive capital investment — one that is about to unlock a completely different level of free cash flow. With 2026 guidance calling for 12.5 to 13.5 million tons of sales at cash costs of $95 to $110 per ton, and Blue Creek capex dropping to just $50-$75 million, the math is about to change dramatically.