Warrior Met Coal Q1 2026

Did Warrior just turn cannibal?

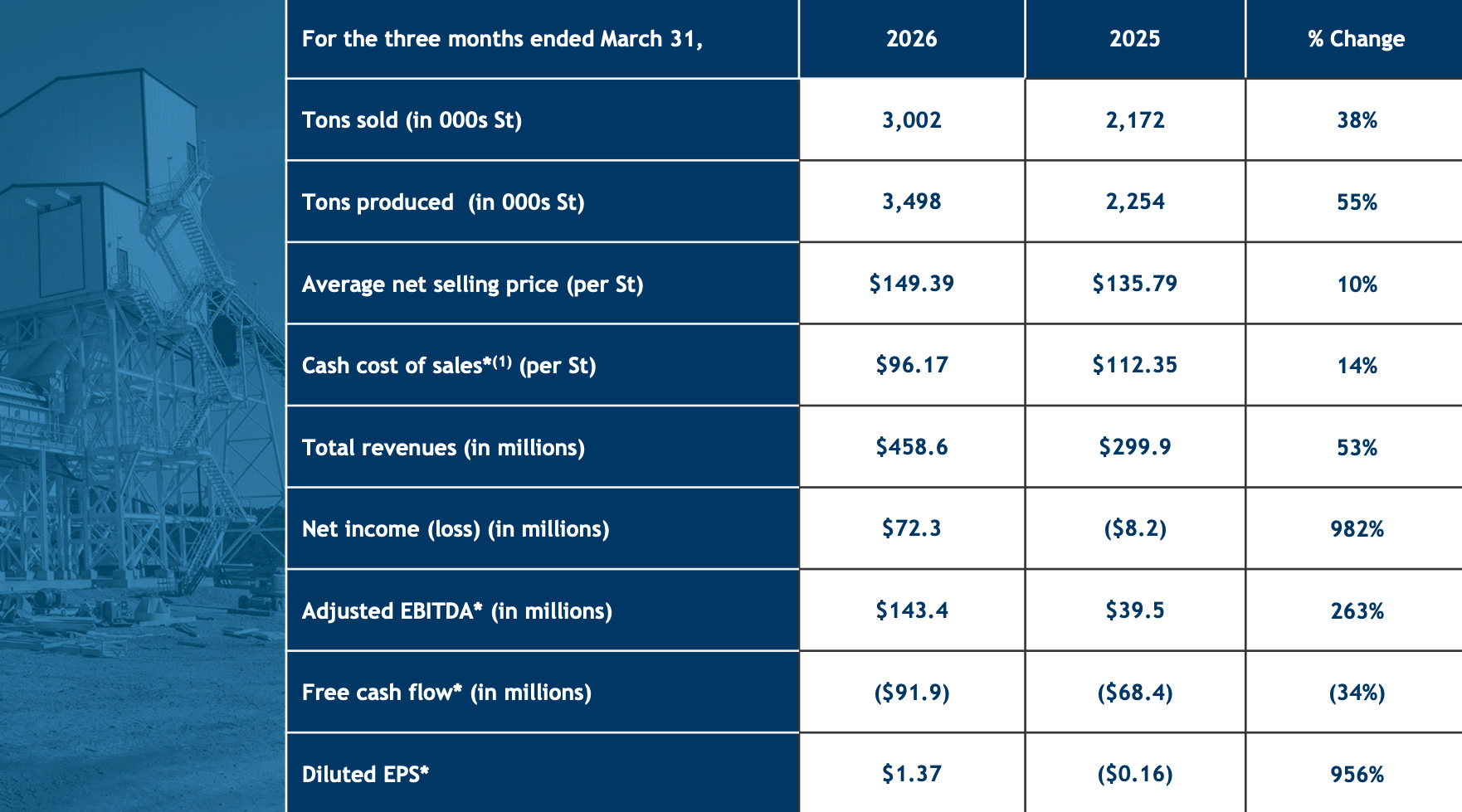

Warrior Met Coal reported Q1 2026 results. Record sales volumes. Record production. EBITDA up 263 percent. Net income of $72 million after a loss in the same quarter last year.

All true. But none of it is the point.

Blue Creek is finished.

Walter J. Scheller said it like this on the call.

“Blue Creek was delivered ahead of schedule and fully in line with our capital expenditure guidance, on budget and fully paid out of cash from operations without incurring any funded debt.”

Total spend $1,022.9 million. Not a single cent of new debt. Delivered ahead of schedule. The final $66 million tranche was paid in Q1.

Built a $1 billion mine without a bank.

The number that matters

“When a company is selling a product with commodity-like economic characteristics, being the low-cost producer is all-important.”

— Warren Buffett, Shareholders letter 2000

Cash cost of $96.17 per ton FOB port.

Q1 2025 cash cost was $112. A 14 percent drop in one year. Fifteen dollars per ton lower. Three dollars of that came from the new 45X tax credit. Strip out the subsidy and the underlying cost is $99 per ton.

Ninety nine dollars per ton FOB port.

That is the number you need to remember. The question I always ask about a cyclical commodity company is what happens in a brutal bear market?

If PLV drops to $130, Warrior makes money. If it drops to $110, Warrior makes money. If it drops to $100, breakeven. Look at the history. PLV has almost never traded below $100 in the last twenty years. This is the definition of a company that cannot lose money.

And it gets better. Blue Creek is just starting. Once it ramps to its full 6 million tons per year, cash cost goes lower. I think we see numbers in the mid eighties by 2027.

Why diesel prices do not hurt Warrior?

Read the recent commentary on coal stocks and you keep hearing the same worry. Diesel is up. Oil is up. Surface miners are getting squeezed. Trucking is more expensive. Margins are tightening.

This is where Warrior is different from almost every other met coal producer. When asked directly about diesel exposure on the call, Walt was almost dismissive.

“We do not do a lot of trucking of coal. We do truck a little bit to the barge load-out, so we are not a high user like strip mines or surface mines. We just do not use a lot of diesel.”

Warrior runs longwall underground mines. The coal moves on belts and rails, not on diesel trucks. For a typical surface miner, diesel can be 10 to 15 percent of total cost. For Warrior it is a rounding error.

This is what a real moat looks like. Warrior is the turtle. Slow, low to the ground, hard to crack. The diesel storm passes over the surface miners. Warrior just keeps producing at $99 a ton and lets the market price adjust around it.

I am not going to tell you what Warrior is worth. I am going to show you what it pays you while you wait. You have seen the business. Now you will see what it pays you.