What Is Transocean Worth Now?

Transocean printed shares and bought the best offshore fleet on earth. The market hasn't done the math yet. I did.

In 2008, Transocean operated 136 rigs and earned $4.2 billion in net income. The stock traded at $150.

Today, after the pending Valaris merger closes, the combined company will operate 73 rigs. Half the fleet. And the market cap? Roughly $12 billion.

In drillships, the new Transocean will own 32 out of roughly 89 globally. That is about 37 percent of world supply. The rest of the industry combined controls only around 56 drillships.

Read that again. And yet, I would argue this fleet is better than the one that printed $4.2 billion seventeen years ago.

The market is not doing the math on this deal. I did. And the numbers stopped me cold.

The Deal

On February 9, 2026, Transocean announced the largest offshore drilling acquisition in over a decade. They are buying Valaris for $5.8 billion. All stock. No cash left the building.

Valaris shareholders receive 15.235 shares of RIG for every share of VAL. No new debt is taken on. Existing RIG shareholders go from owning 100% of Transocean to owning 53% of the combined company. Valaris shareholders get 47%.

That is dilution. Your slice of the pie got smaller.

But the pie got much bigger. And almost nobody on Wall Street has done the arithmetic on how much bigger.

What the Market Sees — and What It Is Missing

Here is what the market sees: $6+ billion in net debt. A leverage ratio around 4x. An offshore driller — the sector that destroyed more investor capital in the last decade than almost any other. The reflex is to run.

Here is what the market is missing: this is a company buying one of the best offshore fleets on the planet with paper — not cash, not debt. They printed shares and handed them over. And the fleet they just acquired is sitting on $10 billion in contracted revenue. The backlog alone nearly doubles the purchase price.

What happens to the debt now?

The CEO laid it out on the investor call. He expects leverage to collapse from 4x to approximately 1.5x within two years. If that happens — and I will walk you through exactly why it can — this stock transforms from a leveraged offshore play that institutions cannot touch into the world's premier deepwater drilling company. The kind of company that gets index inclusion, institutional capital flows, and a completely different multiple.

That is a binary shift in how the market values this equity. And it has not priced it in yet.

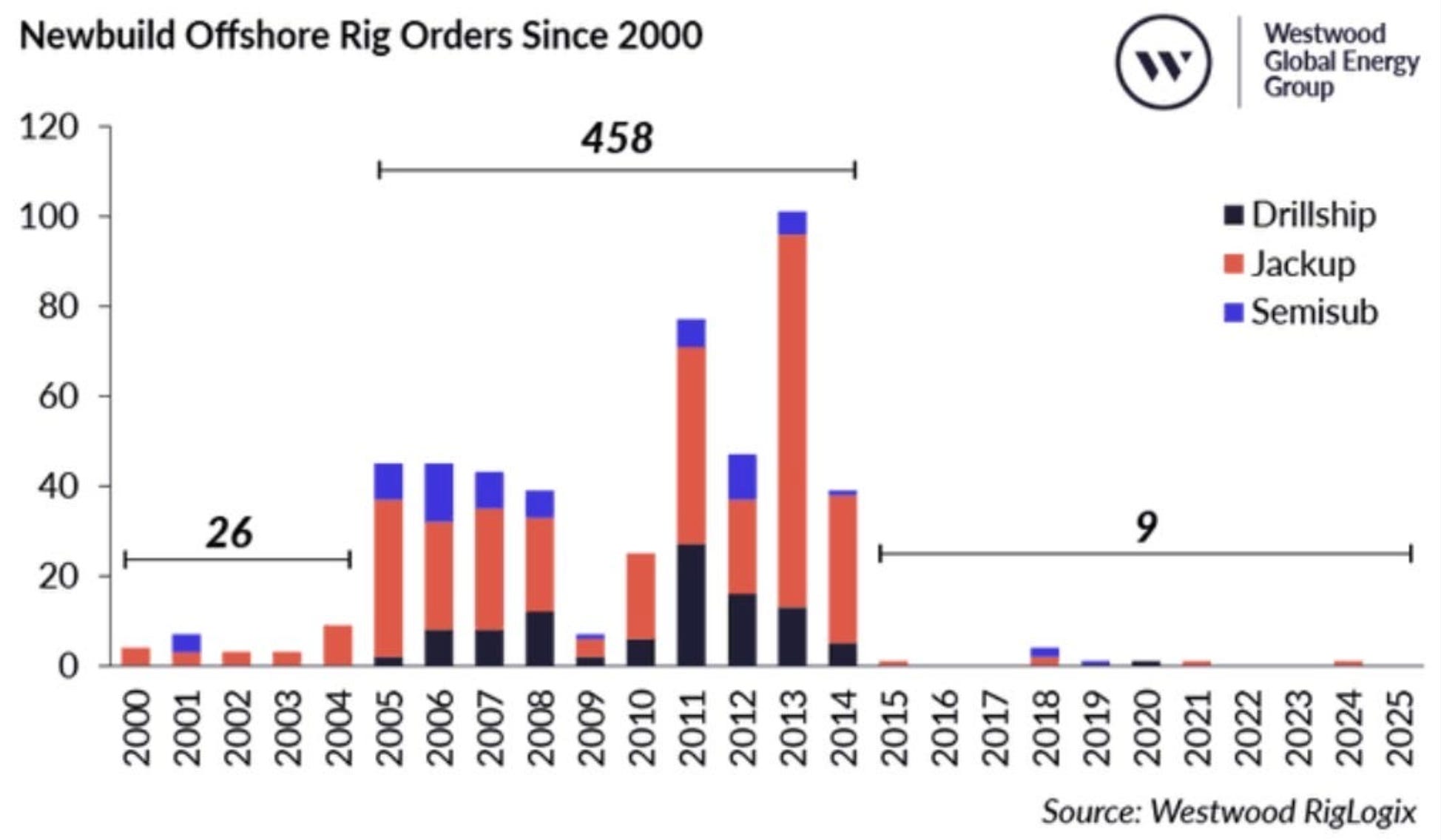

The Supply Wall

No new ultra-deepwater rigs are being built. None. Zero.

The last cycle taught the industry a painful lesson about oversupply. Billions were poured into newbuilds during the boom, and most of those rigs sat idle when oil cratered. The shipyards stopped taking orders. The industry collectively decided: never again.

The existing fleet is all there is. And after this merger, Transocean will own the biggest and best chunk of it.

Demand rising. Supply fixed. Debt disappearing. Free cash flow growing.

That is the setup.

What Is Behind the Paywall

In the paid section below, I go deep on the numbers that nobody else has put together on this deal.

First, I break down what Transocean actually bought by rig class. The fleet composition, the backlog, the synergies, and why Valaris said yes at this price.

Then I walk through the deleveraging math step by step. How does 4x become 1.5x? Where does the cash come from? And what is the hidden optionality in 31 jackups that management says they will keep — but probably will not.

After that, I build a liquidation value framework for the 73 rig fleet using replacement cost and conservative secondary market assumptions. The number I arrived at versus today's market cap will surprise you.

Finally, I put this fleet side by side with Transocean's 2008 fleet. That comparison is most important in this entire analysis. If you understand why 73 rigs today might generate more earning power per unit than 136 rigs did in 2008, you understand the thesis.

Let's get into it.