What the Strait of Hormuz Closure Means for Offshore Drilling

The $150 Barrel Nobody Saw Coming

“The big money is not in the buying or selling, but in the waiting.”

Charlie Munger

On the night of February 28th, 2026, the United States and Israel launched the largest coordinated military strike in the Middle East since the 2003 invasion of Iraq. Supreme Leader Khamenei was killed. Iran retaliated with missiles across the Gulf. And within 72 hours, something happened that energy analysts had modeled for decades but never truly believed would occur:

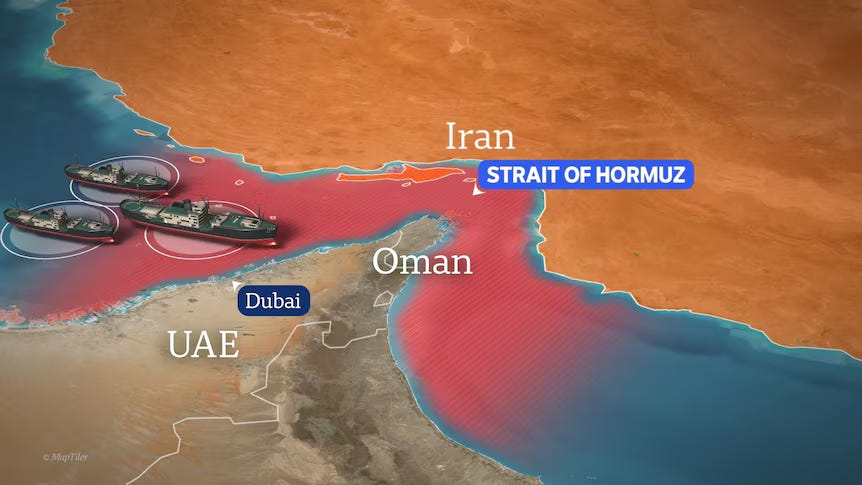

The Strait of Hormuz — through which 20% of the world’s oil and 20% of its LNG flows daily — went dark.

No tankers. No AIS signals. No insurance.

They shut down the most critical energy chokepoint on Earth with a handful of drones and a radio broadcast.

What does this mean for the companies that drill for oil in the safest basins on the planet — thousands of miles from the Persian Gulf?

If you think the answer is “nothing,” close this tab. If you think the answer is “everything,” keep reading.

The Soft Closure: How Insurance Killed Hormuz

Before we get to offshore drilling, you need to understand the mechanism of what actually happened. It’s far more elegant — and terrifying — than any military blockade.

Within hours of Operation Epic Fury, Iran’s Revolutionary Guard began broadcasting VHF warnings to every ship near Hormuz: no vessel is allowed to pass. Then they hit three tankers. Just three. That was enough.

Here’s the chain reaction:

Day 1 (Feb 28): Tanker traffic drops 70%. Over 150 ships anchor outside the strait. Outgoing traffic is heavy as ships flee; incoming traffic collapses.

Day 2-3 (March 1-2): Zero tankers broadcasting AIS signals in the strait. Maersk, Hapag-Lloyd, and every major container line suspend transits. Houthis announce they’re resuming Red Sea attacks. The Suez route dies simultaneously.

Day 4-5 (March 3-4): Protection & Indemnity insurance — the kind that covers a $200 million VLCC — is formally withdrawn for the Persian Gulf. Gard, Skuld, London P&I Club: all out. War-risk premiums surge over 1,000%.

Day 5 (March 4): IRGC claims “complete control” of the strait.

Let that sink in. Iran didn’t need a single submarine. They didn’t need to close anything officially. Their foreign minister actually said they had no intention of closing the strait. But the strait is closed. Because when your insurance company says “we won’t cover you,” and the alternative is risking a $200M vessel and a crew of 25, you don’t sail.

This is the soft closure. And it’s arguably more effective than a hard one, because there’s no single military action the US can take to reverse it. You can escort tankers with destroyers. You can’t escort insurance underwriters.

The Numbers That Should Terrify (or Excite) You

Let’s talk about what 20% of global oil supply disappearing actually looks like in practice.

13 million barrels per day of crude oil passed through Hormuz in 2025. That’s not the total energy flow — add LNG, jet fuel, LPG, and diesel, and you’re looking at roughly 20 million barrels per day of total petroleum products.

For context: the 1973 Arab oil embargo removed about 5 million barrels per day from global markets. Oil quadrupled. The 1979 Iranian Revolution removed about 5.6 million barrels per day. Oil tripled. A full Hormuz closure would remove 8-10 million barrels per day, even after accounting for Saudi and Emirati bypass pipelines. Do the math.

As one energy analyst put it: this could be three times the severity of the Arab oil embargo and Iranian revolution combined.

Yet Brent crude is sitting at around $80. Not $150. Not $200. Eighty dollars.

Why? Because the market is betting this ends quickly. Traders are pricing in a 2-4 week disruption followed by normalization. They’ve seen geopolitical scares come and go. They’re looking at Chinese strategic reserves, at OPEC spare capacity, at Saudi Arabia’s East-West pipeline.

They’re wrong to be this calm. Here’s why.

Saudi Arabia’s East-West pipeline has a capacity of 7 million barrels per day, but terminal infrastructure at Jeddah limits actual throughput. UAE’s Fujairah pipeline can move some barrels. Together, these alternatives might offset 2.5-3 million barrels per day. That still leaves a 5-7 million barrel per day hole.

Meanwhile, Iraq — one of OPEC’s largest producers — is literally shutting down production because it has nowhere to export its oil. These barrels aren’t being rerouted. They’re being shut in.

OPEC+ just agreed to a production increase. It’s “an entirely moot point,” as RBC’s Helima Croft wrote, because you can’t produce oil you can’t ship. “The lion’s share of OPEC barrels in the region could essentially become stranded assets in an extended war scenario.”

And if you think the US military can simply reopen the strait — think again. Trump announced on March 3rd that the Navy would escort tankers through Hormuz. Bold statement. One problem: the US Navy itself told shipping industry leaders it doesn’t have the naval availability to provide escorts. They have nine guided-missile warships in the Arabian Sea and three Littoral Combat Ships in Bahrain. That’s it. As one Hudson Institute analyst put it, escorting tankers under current conditions would require a complementary air campaign to neutralize every missile launcher along Iran’s coast. This isn’t a weekend operation.

Meanwhile, European natural gas prices on the TTF benchmark jumped from €31.9/MWh on Friday to €54.3/MWh by Tuesday — nearly doubling in three trading days. European gas futures posted their biggest single-day gain since the 2022 energy crisis: 38%. Qatar, one of the world’s largest LNG suppliers, halted all production after Iranian drones hit its Ras Laffan and Mesaieed facilities. Daily freight rates for LNG tankers surged over 40% in a single session. If this drags on, China, Japan, South Korea, and India — the biggest consumers of Qatari LNG — will compete with Europe for American LNG cargoes, pushing prices to levels we haven’t modeled since the worst of the post-Ukraine shock.

Now Let’s Talk About Offshore Drilling

Here’s where it gets interesting for anyone who has been following the offshore drilling thesis.

The Middle East is the largest jackup rig market in the world. According to Esgian, there are currently 177 drilling jackups in the region — roughly 36% of the global supply. Of those, 138 are actively drilling.

These rigs aren’t standalone assets. They depend on supply vessels, logistics chains, crew rotations, equipment deliveries — all of which flow through ports and waterways that are now either closed, under attack, or commercially unusable.

Offshore drilling in the Middle East now sits squarely on the geopolitical fault line.

The jackup rigs drilling in Saudi waters, Kuwaiti waters, Emirati waters, and Qatari waters are operating in a region where Iranian drones have struck the Ras Tanura refinery — one of the world’s largest — and QatarEnergy has halted all LNG production. Amazon data centers in Bahrain and UAE have been hit. Insurance companies have pulled coverage for the entire Gulf. Crew evacuation routes are compromised. Supply chain reliability has collapsed.

And it’s not just the existing rigs that are affected. Saudi Aramco’s latest multi-rig jackup tender, upcoming requirements in Kuwait, UAE, and Oman — all of this enters a fog of execution risk, logistics uncertainty, and timeline delays.

This is the repricing event that deepwater bulls have been waiting for.

The Deepwater Thesis, Turbocharged

If you’re an E&P executive who just watched 20% of global oil supply evaporate overnight from the Persian Gulf, you’re asking one question: where can I drill that isn’t next to a warzone?

The answer is deepwater. Brazil’s pre-salt in the Santos and Campos basins. The US Gulf of Mexico, deepwater and ultra-deepwater. West Africa — Nigeria, Angola, Namibia, Senegal. Norway’s harsh environment, politically bulletproof. And Guyana’s Stabroek block, the fastest-growing offshore province on the planet.

These basins share one thing in common: they are nowhere near the Strait of Hormuz, the Red Sea, or any Iranian proxy’s missile range. They offer something the Persian Gulf can no longer guarantee — operational reliability.

And who dominates these basins? The company that just announced the largest offshore drilling merger in history.

Transocean-Valaris: The Right Fleet at the Right Time

On February 9th, 2026 — exactly 19 days before Operation Epic Fury — Transocean announced it would acquire Valaris in a $5.8 billion all-stock deal. The fleet composition matters enormously right now. Here’s the geographic breakdown of where these assets sit:

Deepwater (safe basins): 10 drillships in the US Gulf. 9 in Brazil. 8 in West Africa. Multiple semis in Norway. This is the crown jewel — ultra-deepwater assets positioned in the world’s most politically stable offshore basins.

Jackups (and here’s where we need to be brutally honest): Of the 31 Valaris jackups, nearly 40% are marketed in the North Sea — safe. But the Middle Eastern exposure is not trivial. Valaris leases 7 rigs to ARO Drilling, the 50:50 joint venture with Saudi Aramco. And ARO’s own contract backlog? $2.3 billion as of mid-2025. For context, Valaris’s total backlog is roughly $4.7 billion. So the ARO-linked backlog represents a massive chunk of the revenue pipeline flowing into this merger.

Saudi Aramco already suspended over 30 jackup contracts back in 2024, sending shockwaves through the jackup market and pushing global marketed utilization down to 82%. Valaris felt that directly — one ARO rig (Valaris 143) had its contract terminated and was returned to Valaris. Going into 2026, Valaris was spending roughly $260 million in capex, including upgrades for jackups VALARIS 116 and 250 specifically to continue their long-term bareboat charters with ARO. That’s capex committed to assets sitting in what is now a war zone’s supply chain.

And it gets more complicated. Valaris’s Q4 2025 revenues dropped from $556M to $502M, with the company explicitly citing “lower bareboat charter revenues from rigs leased to ARO Drilling” as a contributing factor. The ARO relationship was already under pressure before a single bomb fell on Tehran.

So let me be direct: if you’re buying the Transocean-Valaris thesis, you’re buying a portfolio where the deepwater crown jewels are worth more than ever, but the jackup backlog in the Gulf carries real and quantifiable downside. A sustained disruption to Saudi operations, or Aramco delaying its jackup program again, could shave hundreds of millions off the combined company’s near-term cash flow.

The bull case isn’t that Middle Eastern risk doesn’t exist. It’s that the repricing of deepwater assets in safe basins overwhelms the jackup risk by a wide margin. The probability-weighted math still favors the combined company — 33 ultra-deepwater drillships in Brazil, GOM, West Africa, and Norway are worth dramatically more in a world where the Persian Gulf is a war zone. And the combined company’s pricing power across all basins increases as the global rig market tightens. But anyone who tells you this is a clean, one-directional trade isn’t being honest with you.

The Repricing Has Barely Begun

RIG is currently trading around $6. Up about 25% in the past month. Up 144% in the past year. The 52-week range is $1.97 to $6.96.

Analyst consensus price target? $6.60. That target was set before Operation Epic Fury. Before Hormuz closed. Before 20% of global oil supply went offline.

Here’s what the market hasn’t fully priced in:

1. Dayrates are going up. When oil was at $66, offshore operators were squeezed. At $80+, the economics of deepwater projects improve dramatically. If Brent sustains above $90, dayrates will reprice higher as E&P companies rush to sanction projects in safe basins.

2. Supply is tightening. 177 jackups in the Middle East face operational uncertainty. Some projects will be delayed. Some rigs will be unable to relocate. This tightens the global supply of available rigs, particularly in basins outside the Gulf.

3. The merger creates a monopoly-like position in ultra-deepwater. Post-merger, Transocean will have nearly twice as many drillships as Noble Corp, the next largest competitor. In a tightening market with rising demand, this fleet concentration is pricing power.

4. The structural narrative has shifted. Before the war, the investment case for offshore drilling was “multi-year upcycle driven by underinvestment.” Now it’s “multi-year upcycle driven by underinvestment PLUS a permanent repricing of geopolitical risk that favors deepwater in safe basins.” That’s a different animal.

But What About the Risks?

I’d be lying if I told you this was a one-way trade. Here are the things that could go wrong:

The war ends quickly. If Iran’s regime collapses in weeks and Hormuz reopens, the geopolitical premium evaporates. Oil falls back to $65-70. The offshore thesis still works long-term, but the urgency dissipates.

Global recession. A sustained oil spike above $100 is stagflationary. Central banks pause rate cuts or hike. Demand destruction kicks in. E&P companies pull back on capex. Offshore drilling is cyclical — it doesn’t escape a demand collapse.

Transocean’s debt. Even with deleveraging progress, Transocean’s credit rating is CCC+ from S&P. The company reported a $2.92B net loss for 2025 (driven by rig impairments). In a scenario where oil collapses, that debt load becomes existential again.

Middle Eastern jackup exposure. This is the biggest risk specific to the merger thesis. ARO Drilling’s $2.3 billion backlog is tied to Saudi Aramco — the same Saudi Arabia whose Ras Tanura refinery was hit by Iranian drones. Aramco already suspended 30+ jackup contracts in 2024, and Valaris’s Q4 revenues dropped partly because of lower ARO charter income. If Aramco suspends or delays jackup operations again — entirely plausible given the war in its backyard — the combined company loses hundreds of millions in near-term cash flow. Valaris was spending $260M in 2026 capex partly on upgrading rigs for ARO. That’s capital deployed toward an increasingly uncertain revenue stream.

Merger execution risk. The deal isn’t closed yet. Expected in H2 2026. Regulatory and shareholder approvals are still pending.

The Buffett Framework

Charlie Munger used to say that the big money is made not in buying and selling, but in waiting. The offshore drilling sector has been waiting — through years of oversupply, debt restructuring, scrapped rigs, and depressed dayrates — for the cycle to turn.

There’s a concept in Munger’s thinking called “lollapalooza effects” — when multiple forces converge in the same direction, the results are far more powerful than any single force alone. That’s what’s happening here: structural underinvestment in offshore since 2014 tightening supply, rising oil prices improving deepwater economics, geopolitical risk repricing driving demand toward safe basins, industry consolidation concentrating pricing power in the largest operators, and insurance market dislocation creating a permanent risk premium for Gulf operations.

Each of these is bullish for deepwater drilling. Together, they create a setup that the offshore industry hasn’t seen in a decade.

The market is pricing RIG like a company that operates in a world where Hormuz is a temporary scare. But what if it isn’t? What if the insurance market never fully reverts? What if E&P capital expenditure permanently tilts toward deepwater in the Americas and West Africa? What if the Transocean-Valaris merger closes into a market where dayrates are 30% higher than anyone modeled?

That’s not a $6 stock. That’s a $10-15 stock. Maybe more.

The Bottom Line

The Strait of Hormuz is closed because a few drones made it uninsurable. And in doing so, it exposed the single biggest vulnerability in the global energy system — dependence on a 21-mile-wide chokepoint controlled by a hostile regime.

The fix isn’t military escorts. The fix isn’t government insurance. The fix is structural diversification of energy supply toward basins that don’t require threading a needle between Iran and Oman.

That means deepwater. That means Brazil, the Gulf of Mexico, West Africa, Norway, and Guyana. And the company best positioned to capture that shift — with the largest fleet, the strongest backlog, and the most diversified geographic exposure — just merged into existence.

The question for investors isn’t whether the thesis is right. It’s whether the market gives you time to get positioned before it reprices.

The next time someone tells you Hormuz will reopen any day now, ask them one question: who’s writing the insurance?

Cheers, Sandro

Disclaimer: This is not financial advice. I hold a long position in Transocean (RIG). The offshore drilling sector is highly volatile and leveraged to commodity prices. This post reflects a bull case analysis — I’ve tried to present the risks honestly, but my positioning means I’m not a neutral observer. Do your own research.

Thank you! Are you holding your position?