Offshore Oil Drilling: Why Deepwater Is the Old New King

Onshore – the beginning of the end

Oil is still mostly produced onshore. The giant fields like Ghawar in Saudi Arabia, Burgan in Kuwait, or Rumaila in Iraq have pumped out hundreds of billions of barrels. These are deposits where the oil is light, the reservoirs huge, and production costs among the lowest in the world, often below $30 a barrel. Today, the majority of proven global reserves, around 1.2 to 1.3 trillion barrels, are concentrated on land. But the truth is that the best and cheapest fields have already been discovered. What remains are smaller, more expensive, and heavier reservoirs.

Oil will not disappear from our lives anytime soon. Electric vehicles are on the rise, but the transition will take much longer than most people think. In Germany alone, 55,000 auto industry jobs were lost in the past year due to EVs, and public debate has even turned to the idea of returning to the “good old” combustion engines. Every serious projection shows that oil demand will continue to grow over the next decade. For me, that still makes oil a relatively safe bet.

But onshore oil has its big problems – and the first is geopolitics. If the Strait of Hormuz were to be closed, through which one fifth of the world’s oil passes, the price would explode. The same scenario applies to the Suez Canal, the key connection between the Middle East and Europe. The Strait of Malacca is vital for China and Japan, while Russian and Caspian oil flows through the Bosporus and Gibraltar. Each of these chokepoints is a potential crisis constantly keeping prices on edge. And the way the world reacts today shows how fragile and nervous everything has become.

Then there is shale. The fracking revolution turned the United States into an oil giant, but with serious limitations. Shale wells deplete incredibly fast, often losing up to 70% of their output in the first year. And shale feels like it is already nearing its endgame. Without some breakthrough technology to extend the life of these fields, shale will not be able to quench the world’s thirst for oil.

And here we come to another onshore problem. Venezuela is an oil emperor on paper. It has the largest proven reserves in the world, around 303 billion barrels. But that oil is neither light nor cheap. It is extra-heavy crude from the Orinoco Belt, so thick it must be mixed with lighter fractions or diluents just to flow through pipelines. When all costs are factored in, we are talking about $60–80 a barrel. Add political instability and sanctions, and you realize that those massive reserves are, in practice, often unusable. To remind you, Brent crude trades today at about $65.

Because of all this, the world has little choice but to turn to the old, and yet new, king – the sea.

Why Offshore is the Old New King

Onshore still holds the bulk of proven oil reserves – about 1.2 to 1.3 trillion barrels.

Offshore, in comparison, has around 250 to 300 billion barrels of proven reserves. To put it simply, we still have no idea how much oil lies beneath the seas. Oceans cover 71% of the Earth’s surface and you don’t have the major risk of passing through straits and. Until very recently we had no real way of exploring the deep waters. For most of the past century, drilling was limited to shallow offshore shelves and, of course, to land.

That has changed. Today we have the technology to “see” beneath the ocean floor and drill at depths once thought impossible. It works in two steps. First, seismic survey ships send sound waves into the seabed. Those waves bounce back differently depending on the rock layers, allowing geologists to build a 3D picture of what lies beneath – like an ultrasound of the Earth. Then come modern drillships, floating platforms equipped with dynamic positioning systems, which can stay perfectly still in thousands of meters of water and drill down another 5–7 kilometers below the seabed. Twenty years ago, this was science fiction. Now it is routine.

The proof is in the discoveries. Brazil’s pre-salt fields in the Santos Basin revealed more than 30 billion barrels. Johan Sverdrup in Norway turned into the largest European oil find in three decades, with reserves of nearly 3 billion barrels. And the newest frontier is Africa: in 2022, Shell and Total uncovered Venus and Graff in Namibia, with potential in the range of 3 to 12 billion barrels.

Production costs tell the same story. Onshore giants like Saudi Arabia can still pump at $10–20 a barrel, but most new land-based fields are much more expensive. Shale in the U.S. comes in at $35–50. Extra-heavy Venezuelan crude can cost $60–80. Offshore is competitive: shallow water projects run at $20–40 a barrel, while deepwater averages $40–60.

Important Valaris (VAL) Update

Why is my offshore bet specifically Valaris? I talked more about this in my post on Valaris.

Basically, my offshore bet is asymmetric because demand for offshore drilling is rising, while the existing fleet of about 80 drillships is unlikely to increase and will likely shrink—and by 2030, more than 100 drillships could be needed. As of today, September 9, 2025, nobody has filed a request to build a new drillship – proven fact. The only significant order in 2024–2025 was for jackup rigs. ARO Drilling (the Saudi Aramco–Valaris joint venture) ordered a third S-116E class jackup, named Kingdom 3, from IMI (International Maritime Industries) in Saudi Arabia in 4Q 2024. But these are jackups for shallow waters, not deepwater drillships. That distinction is important.

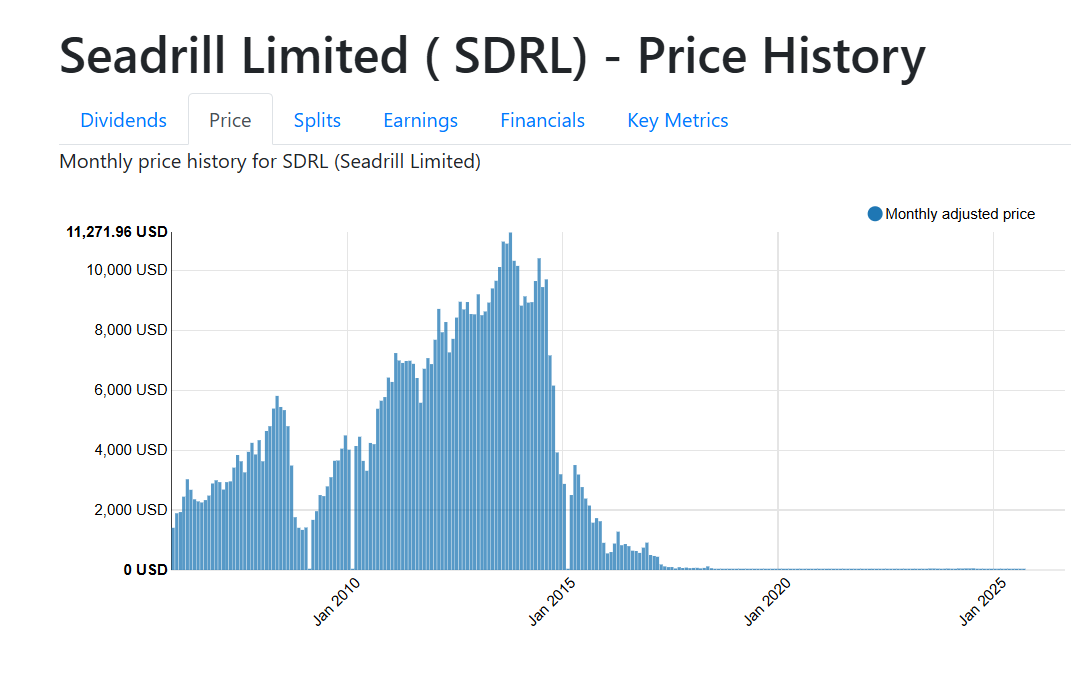

No one will order new rigs, since they cost over $1B and nobody wants to finance them after the bankruptcies. But the beauty of the market is that sometimes you have asymmetry in price compared to value. These companies are usually dull and not much happens, but recently news came out that Seadrill, whose CEO said they would be happy to be acquired for the right price, is open to a deal. Seadrill’s market cap is around $2.2B and they operate a fleet of 17 rigs. I think an acquisition could realistically be done for about $3B. To put it simply, you’re getting 17 rigs worth around $15B for just $3B. So who can take them over?

Noble (NE) has just announced the acquisition of Diamond in a stock-plus-cash transaction, so another big move from them is very unlikely.

Transocean (RIG) looks the most interested, but the chances they actually buy Seadrill (SDRL) are very small. They already carry around $7–8B in debt, and to acquire Seadrill they would need to raise more debt or issue a huge amount of stock. All their free cash flow is currently used for debt repayment, and while they have recently moved a subsidiary to Bermuda to prepare for a possible acquisition, it is still very unlikely.

I found it very interesting that Valaris management said in their last presentation that almost all FCF would be returned to shareholders through buybacks, unless they found a better use. And now they’ve stopped buybacks and are piling up cash. :)

I think that Valaris is the most serious candidate. It has low debt and strong free cash flow, it has stopped buybacks and is clearly accumulating cash, its headquarters are already in Bermuda like Seadrill, and its CEO is a former Seadrill CEO who knows the fleet well. Valaris could finance such a deal with about $1B of free cash flow and an additional $2B in debt without dilution. Isn’t this interesting?

Will the deal happen?

The chances are high. And this would be a great deal for Valaris if it goes through. Let’s see why.

If Valaris acquires Seadrill, they don’t just expand their fleet—they become the undisputed leader in offshore drilling. That leadership would likely change how the market values them, giving Valaris a “leadership multiple” or premium that comes with being the clear number one.

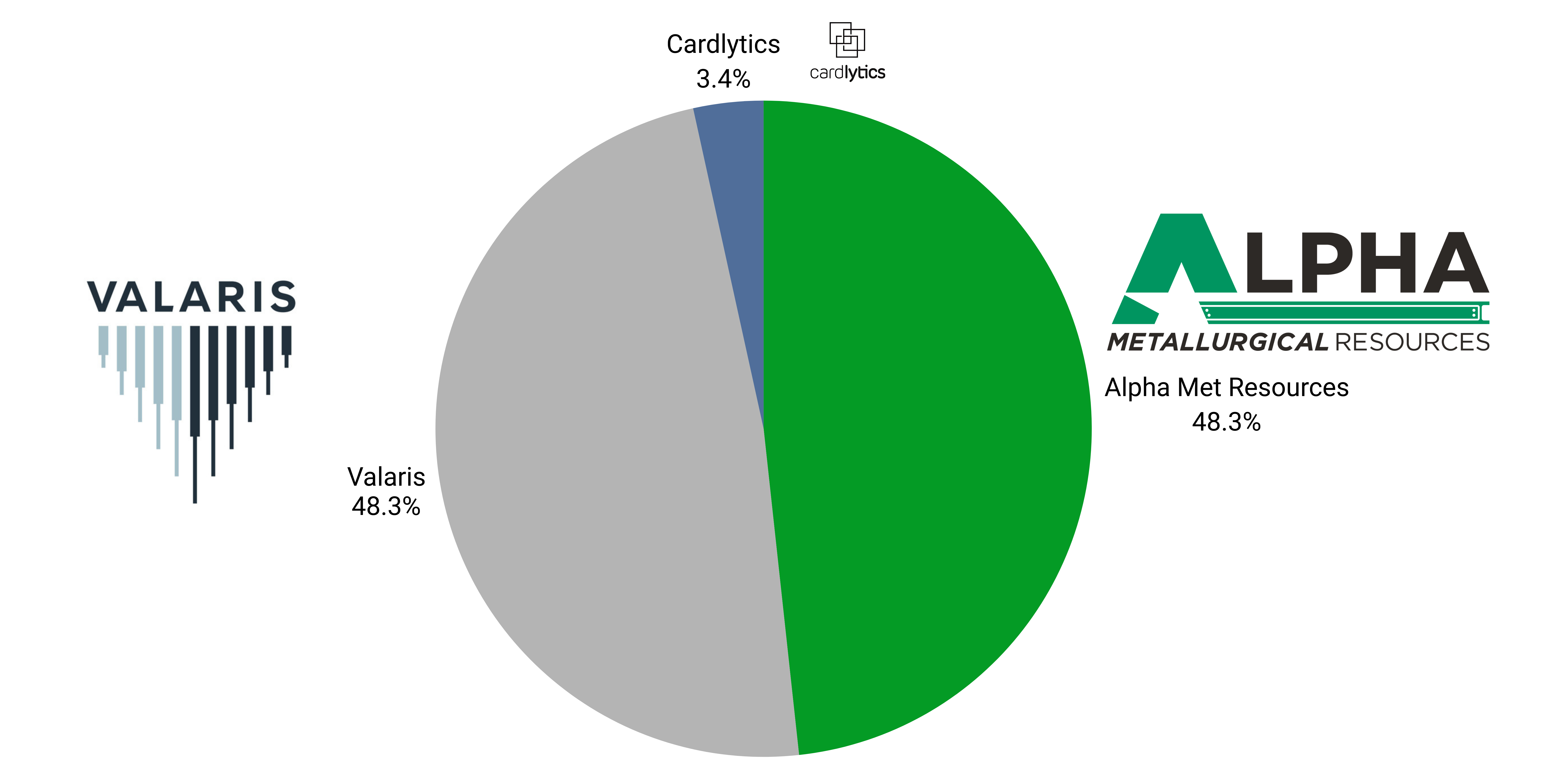

The combined company would control 31 drillships and 33 jackups, by far the largest offshore fleet in the world. This scale matters. A fleet of that size gives them bargaining power exactly when the world needs more rigs and there are fewer available. Replacement cost for such a fleet would be over $40B, yet Valaris today is valued at just over $3.5B. The disconnect is obvious.

The odds are high that demand for offshore rigs continues to tighten. Historically, drillship dayrates have reached $650–700K at peaks, and jackups $180–200K. Given the shrinking supply and no newbuilds in sight, it isn’t unrealistic to think we could return to or even exceed those levels in the next cycle. Under such conditions, the combined Valaris–Seadrill entity could generate enormous revenues. With utilization around 90%, 31 drillships earning around $600–700K per day and 33 jackups at $140–170K per day translates into annual revenues approaching $8–10B by the late 2020s.

At 55–60% EBITDA margins, this points to $4.5–6B of operating profit. After deducting maintenance capex, interest, and modest taxes, free cash flow could easily run in the range of $4–5B per year. In other words, if Valaris pays around $3B for Seadrill, they would recover that outlay in less than a single year of strong cycle cash flows. Over a five-year horizon, cumulative free cash flow could reach about $20B, all while controlling the most powerful fleet in the sector.

This kind of profile fundamentally changes the equity story. Instead of being valued like a cyclical, capital-intensive driller, Valaris would trade more like an industry leader with pricing power. That’s where the “leadership multiple” comes in. But will it ever trade at replacement cost? Well, we have to remember that replacement cost is a data point that sometimes may not be the most important one. In the end, the real way all businesses get valued is the cash they are going to produce from now until judgment day and then discounting it back. That is the way Valaris is going to be valued eventually. The fact that the replacement cost of the assets is high is interesting, but it does not mean that it will trade at that value. It could even trade above that value, depending on how tight the market gets. But the bigger determinant of how we do on these bets is not so much replacement cost as it is where we are on supply and demand. It is difficult to imagine that any of these offshore oil service companies will ever place an order for a new drillship.

Will all of this happen? The chances are there. But I like this bet. I am happy to keep adding Valaris even at $50 per share. If they make the acquisition, they will become the largest offshore company in the world. And if not, they now have $1B in cash, next year they will generate another $1B in FCF, and with that, if the share price stays where it is today, they could buy back 50% of their shares.

So: Heads I win, tails I don’t lose much.

Cheers,

Sandro

Brilliant macro-to-micro analysis, Sandro — especially the way you connect declining onshore economics to offshore scarcity. One question I’d love to hear you explore further: what are the geopolitical and policy implications if offshore truly becomes the “old new king”?

Could deepwater fields shift global energy sovereignty — away from landlocked states and toward maritime powers? And how might this reshape OPEC influence, naval security, or even ESG-driven investment mandates over the next decade?

Thanks for the great question.

I think everyone’s attention is on the sea right now, because even the smallest spark of geopolitical tension in the Middle East could send oil prices soaring. The U.S. can’t release massive amounts of oil from its strategic reserves anymore like it did a few years ago to calm the market.

That’s why deepwater fields naturally strengthen maritime powers like the U.S., Brazil, and Norway control over the oceans is becoming just as important as control over land. It could reduce dependence on OPEC and the Middle East, and shift more influence toward countries with stable ocean access.

That said, macro is hard to predict — too many moving parts. There are plenty of tailwinds supporting offshore, but also headwinds like new taxes and regulations. That’s why I prefer to stay mostly focused on the micro side, on specific companies and their cash flows.