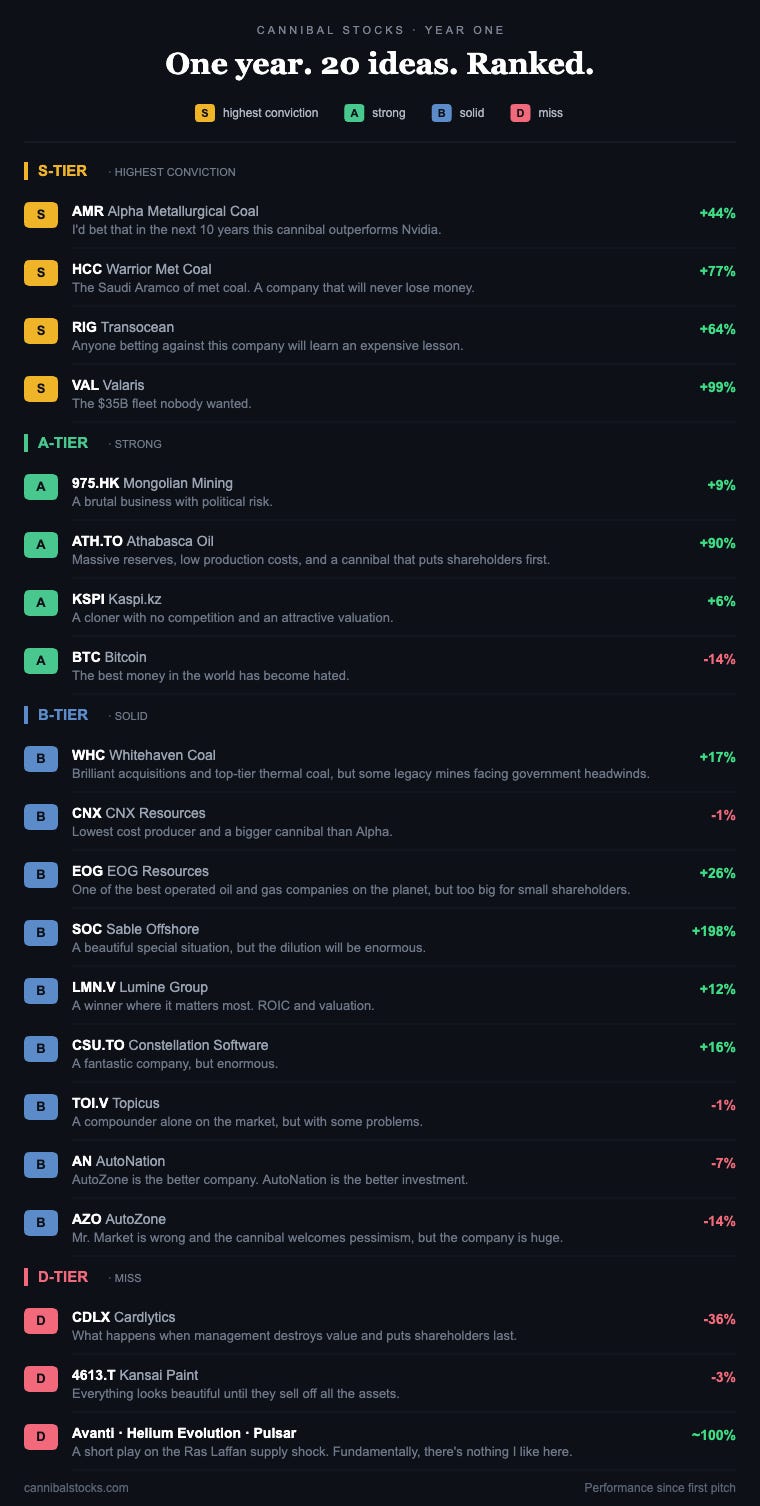

The First Year of Cannibal Stocks: 20 Ideas, Ranked From Best to Worst

S Tier to D Tier

Let's look back at the first year of Cannibal Stocks.

One year ago I published my first pitch. Twenty ideas later, this is the scoreboard.

Not a victory lap, and not a list of winners cherry-picked after the fact. A ranking. Every idea I put in front of you, sorted from my highest conviction to my biggest mistake — including the ones I actually own, and the ones I only traded and would never marry.

That distinction matters, so let me be clear about it up front. Some of these are companies I hold because I believe in them for the next decade. Some were special situations — Helium, Sable — that I rode hard and sold, brilliant trades built on businesses I have no interest in owning. A good return tells you nothing about which is which. The ranking does.

How to read this

The tier is my conviction, not the share price. S means highest conviction. A is strong. B is solid. D is a miss. A stock can be up 100% and still sit in D, and another can be down and still sit in A — because price is what happened, and conviction is what I think happens next. Performance is measured since the first pitch. The only companies I currently hold in my portfolio are the S-Tier names.

With that out of the way, from best to worst.

S-Tier — Highest Conviction

This is where I have the least doubt, and it’s no accident that it’s dominated by two industries the market still hates. Met coal and offshore drilling. The setup in both is the same. New supply is brutally hard to bring online, the survivors have cost positions that don’t lose money, and the industry’s ugly history — bankruptcies, dilution, destroyed capital — is precisely what keeps the opportunity alive. Everyone remembers the pain. Almost nobody noticed that the supply side was permanently damaged.

Alpha Metallurgical (AMR) is one half of my met coal core. If prices stay high, it’s probably the better bet than Warrior — cheaper valuation, more aggressive buybacks, better capital allocation. It’s going to return all of its free cash flow to shareholders, and the market still treats it as garbage. If you're a cannibal and Mr. Market treats you like garbage, that's about as good as it gets. The main negative is its dependence on railroads.

Warrior Met Coal (HCC) is the other half. Better margins, a fantastic management team, and a moat most investors underestimate. If everything goes wrong, Warrior is the one that still doesn’t lose money. I genuinely can’t tell you which I prefer between the two, so I own both. The anomaly is that both will return 100% of free cash flow to shareholders. The only knock on Warrior is its preference for dividends. At these prices, buybacks would create far more value over time.

Transocean (RIG) is the offshore thesis in one name. The industry is consolidating fast, and there’s a realistic path where one player controls roughly half the world’s ultra-deepwater fleet. Once the debt comes down, I expect management to start handing cash back — and that’s when the market re-rates the whole thing. The first-year return was already excellent. I think the bigger story is still ahead. On the negative side, the Valaris merger is being financed with shareholder dilution. If management creates more value per share than it gives away, and eventually adopts a met coal-style capital return strategy, returning virtually all free cash flow to shareholders, this could turn into a brutal investment.

Valaris (VAL) is the same trade — the $35 billion fleet nobody wanted — and the market is only now waking up to what it’s worth. I already view these two companies as one position. At this point, I have very little left to add.

A-Tier — Strong

A-tier is where conviction is high but something — size, politics, a single variable — keeps it just short of the top. These companies have a high probability of eventually earning an S-Tier ranking and making their way into my portfolio.

Mongolian Mining (975.HK) has incredibly low production costs, decades of Chinese demand, a railway due in 2028, and a company that has started buying back its own stock. Premium metallurgical coal with more than a billion tonnes of reserves and resources. An asset that I believe will become one of the most sought-after in the world over time. Even India is looking for ways to access this coal, but transportation is challenging because it would have to move overland, making logistics costs significantly higher. The reason it isn’t S-tier is one word: politics. When Mongolia’s Democratic Party was in power, it tried to nearly destroy this company.

Athabasca (ATH.TO) is a genuine cannibal that returns nearly every spare dollar through buybacks, and you can already see it in the share price. A major tailwind is developing right now. Canada wants a new pipeline to the Pacific Coast. If that happens, Alberta can export more oil directly to Asia instead of relying on U.S. buyers.That would narrow the massive discount Canadian oil trades at today. Athabasca wouldn’t need to produce a single extra barrel to benefit. A higher realized price means higher cash flow. Higher cash flow means more buybacks. And the best part is that every dollar goes back to shareholders through a cannibal that almost nobody is paying attention to.

Kaspi (KSPI) isn’t a cannibal, but management acts like one — entirely in shareholders’ interest. An enormous moat, a lot of growth, and the best cloner alive. They don’t reinvent anything, they find what works elsewhere and execute it better inside a platform that already runs millions of daily lives. At around 7x earnings, the valuation makes no sense to me. If management keeps doing what it’s done for a decade, this could end up the single best idea on the list. The only problem? My wife has banned me from investing in Kazakhstan.

Apparently companies that just emerged from bankruptcy are acceptable levels of insanity. 😅

Bitcoin (BTC). I don’t treat it as an investment. I treat it as money. Viewed purely as an asset, the fixed-supply argument honestly puts it alongside met coal and offshore. It’s still down, and it’s still hated. Both of those are features, not bugs. Because here’s the thing I’m certain of: every fiat currency eventually trends toward its intrinsic value, which is zero.

I lived through it. The hyperinflation that destroyed the Yugoslav dinar in the early 1990s wasn’t a chart to me — it was daily life. If you’ve never seen what happens when money dies, watch this. Eighteen minutes will teach you more about why Bitcoin matters than any white paper.

B-Tier — Solid

These are good-to-great businesses where I either expect more modest upside, have an open question, or simply prefer a wider margin of safety before getting excited.

Whitehaven (WHC) has brilliant capital allocation and top-tier thermal coal. My hesitation is that in the great years, a large slice of free cash flow leaks out through royalties and taxes. And some of the mines are not in the best condition.

CNX Resources (CNX) has unbelievably low costs and a massive buyback the market doesn’t appreciate yet. A bigger cannibal than Alpha, even — it just hasn’t shown up in the price. I also think patience makes sense here. Once the situation in the Middle East stabilizes, natural gas prices could come down, giving us a chance to pick up shares at a lower price.

EOG Resources (EOG) is one of the best-run operators on the planet. The only problem is that it’s already a giant, which caps the upside compared to the smaller, more hated names elsewhere on this list.

Sable Offshore (SOC) was the easiest trade of the year for anyone willing to buy when it was hated, and the return shows it. Sable Offshore has a tailwind from California because the state is reducing reliable energy supply while energy demand remains high, increasing the value of local oil production. But the next chapter needs enormous capital, much of it likely from issuing shares, and that dilution is exactly why I can’t fall in love with the long-term story.

Lumine (LMN.V), Constellation Software (CSU.TO), and Topicus (TOI.V) are all fantastic businesses, and I would not be surprised if they are much larger companies ten years from now. They probably belong closer to the A-tier than the B-tier. What cooled me off is that none of them are cannibals. We are unlikely to ever see buybacks. On top of that, after speaking with people close to Topicus, I learned that growth has become a bit more challenging than I originally thought, even in areas where I believed competition was almost nonexistent. That doesn’t break the thesis, but it does change it. These are still excellent businesses. The problem is that they are not extremely cheap, so for now they go into the "too hard" pile.

AutoNation (AN) and AutoZone (AZO). I think Mr. Market is making a clear mistake pricing both this cheaply. The fleet keeps aging, cars get more expensive to replace, and lower share prices just let both retire more stock per dollar of buyback. AutoZone is the better company; AutoNation is the better investment. They’re in B only because the explosive growth is mostly behind them. AutoZone has already delivered roughly a 450x return since its IPO. That's what happens when a cannibal retires 9 out of every 10 shares outstanding. Madness.

D-Tier — Miss

The honest part of the list.

Cardlytics (CDLX) was probably the biggest mistake of my investing life — and the most valuable. The real lesson wasn’t that I misunderstood the moat. It was dilution. Good management buys stock when it’s cheap. Bad management pays itself with stock while shareholders get diluted. Buffett called it “sell low, buy high.” Cardlytics followed that playbook perfectly. Roughly $49 million of new shares were issued in 2024 while the company continued losing money. The stock fell from $157 in February 2021 to about $0.65 today, a decline of roughly 99%. Management got richer. Shareholders got poorer. Munger had a line for companies like this.

A colony of rats in a grain warehouse.

Kansai Paint (4613.T) returned a lot of cash, which I liked — until I realized most of it came from selling assets, not recurring free cash flow. That makes the long-term economics genuinely hard to judge, so it lands here by default rather than conviction.

The Helium Basket (Avanti, Helium Evolution, Pulsar) was, alongside Sable, the best trade of the year. I bought early, when nobody was looking, and sold near the top after the crowd arrived. As a trade, it was close to perfect. As businesses, these have weak economics, uncertain paths to profitability, and depend almost entirely on expectations rather than performance. Could one of them work? Sure. But they don’t deserve any more of my time — which is exactly why a great trade still ends in the D-tier.

The Rats Ate the Grain in Those Other Companies

From today, only cannibals live in the portfolio. Everything else was a ride. For a year I showed you what I look for. Now I show you what I hold.

Most companies issue shares. Mine retire them.

The rats ate the grain in those other companies. Mine eat themselves.

Out there, plenty of companies dilute you while their prices keep climbing. Be careful what you own.

Year two begins.

Cheers, Sandro

Very cool to see your highest convictions all played out (buy the best companies with long term supply tailwinds in the most hated sectors). Love reading your stuff Sandro! I really like the depth of analysis on your highest conviction picks.